Mastering the E-Layer of the WC-PULSE Framework™

The Force Multiplier You Cannot Control

In January 2025, the central bank of a Caribbean nation announced a 100-basis-point increase in its benchmark lending rate. The decision was widely anticipated by economists and reported in the morning financial press. By lunchtime, most CFOs in the region had moved on to other matters. It was, after all, a macro-economic event – something for economists and central bankers to debate. Not a working-capital issue.

Except that it was. Within 60 days, that single rate decision rippled through the working-capital positions of every company carrying floating-rate debt. A manufacturer with US$25 million in variable-rate revolving credit saw its annual interest expense increase by US$250,000 – the equivalent of losing a mid-sized customer. A distribution company whose suppliers began demanding shorter payment terms in response to their own increased borrowing costs experienced a compression in DPO that tightened available liquidity by US$1.8 million. A professional-services firm whose largest client, a government entity, delayed project payments by an additional 30 days as the public sector absorbed the fiscal impact, saw its DSO spike from 55 to 87 days.

None of these companies were poorly managed. All had competent treasury teams and functioning cash-flow forecasts. But none of them had a systematic mechanism for translating a macro-economic signal – an interest-rate decision, a currency movement, a commodity-price shift – into a working-capital impact assessment with specific, actionable trigger responses. They experienced the macro shock and then reacted. The WC-PULSE Framework is designed to ensure they anticipate and pre-position.

This is the domain of the E-Layer: External and Macro Environment Sensitivity. It is the final diagnostic layer in the PULSE architecture, and in many ways it is the most challenging, because it monitors forces that the organisation cannot control but must prepare for.

You cannot control interest rates, exchange rates, or commodity prices. But you can control how prepared your working capital is to absorb them.

The Macro-Working-Capital Transmission Mechanism

The first step in mastering the E-Layer is understanding how macro-economic forces transmit into working-capital outcomes. Most finance professionals understand these connections intuitively but have never mapped them systematically. The E-Layer formalises these transmission pathways so that they can be monitored, quantified, and managed.

Channel 1: The Interest-Rate Channel

Interest rates affect working capital through three distinct pathways. The most direct is the cost-of-carry pathway: every dollar of working capital that is financed by debt becomes more expensive when rates rise. A company with US$40 million in working capital financed through a floating-rate revolving facility experiences a direct annual cost increase of US$400,000 for every 100-basis-point rate rise. This is pure margin destruction that flows directly to the income statement.

The second pathway is the customer-behaviour pathway. When rates rise, your customers’ cost of capital increases, which pressures their cash flow, which causes them to stretch payment terms. This effect is not immediate but it is predictable: research consistently shows that DSO across the corporate sector increases by 1.5 to 3 days in the 6 months following a 100-basis-point rate increase, as the cost of capital percolates through customer behaviour.

The third pathway is the investment-return pathway, which operates in the opposite direction. When rates rise, the return on surplus cash increases. Organisations in the Green Zone benefit from higher yields on their deployed surplus, partially offsetting the cost-of-carry impact on the financed portion of working capital. The E-Layer captures both sides of this equation to produce a net interest-rate sensitivity score.

Channel 2: The Foreign-Exchange Channel

For any organisation that operates across currency boundaries – and in the Caribbean, that means virtually every enterprise of meaningful scale – the FX channel is often the single most volatile input to working-capital health. The transmission pathways are multiple and compound.

The procurement pathway is the most direct: a company importing goods priced in US dollars and selling in Jamaican dollars, Trinidad and Tobago dollars, or Barbadian dollars experiences an immediate increase in its cost of goods sold when the local currency depreciates. If the company cannot pass this cost through to customers immediately – and in most markets, price adjustments take 30 to 90 days to implement – the margin compression is absorbed by working capital. The inventory that was purchased at the old exchange rate is worth more to replace but sells at the old price. The cash collected on the sale is insufficient to fund the next purchase at the new exchange rate. The gap is funded from working-capital reserves or incremental borrowing.

The translation pathway affects companies with operations or receivables denominated in foreign currencies. A subsidiary’s working capital, when translated back to the parent’s reporting currency, gains or loses value with exchange-rate movements. This is often dismissed as a non-cash accounting adjustment, but it affects covenant calculations, borrowing-base determinations, and the perceived health of the balance sheet in ways that have very real operational consequences.

The competitive pathway is the subtlest. When your currency depreciates, imported competitors become more expensive and your export pricing becomes more competitive. When it appreciates, the reverse occurs. These competitive shifts affect revenue volumes and pricing power, which in turn affect collections, inventory requirements, and the Cash Conversion Cycle. The E-Layer monitors these second-order effects because they often have a larger working-capital impact over time than the direct procurement pathway.

Channel 3: The Commodity Channel

Companies whose input costs are linked to commodity prices – energy, agricultural inputs, metals, chemicals, packaging materials – face a third macro transmission channel. Commodity-price spikes increase the cost of inventory, which increases DIO in dollar terms even if physical inventory volumes remain constant. They also increase supplier bargaining power, which can compress DPO as suppliers demand faster payment. And they create pricing uncertainty that can delay customer purchasing decisions, temporarily increasing DSO as the sales cycle elongates.

The Caribbean is particularly exposed on this channel. Import-dependent economies absorb global commodity-price movements with limited ability to hedge at scale, and the transmission to local working-capital positions is rapid and direct.

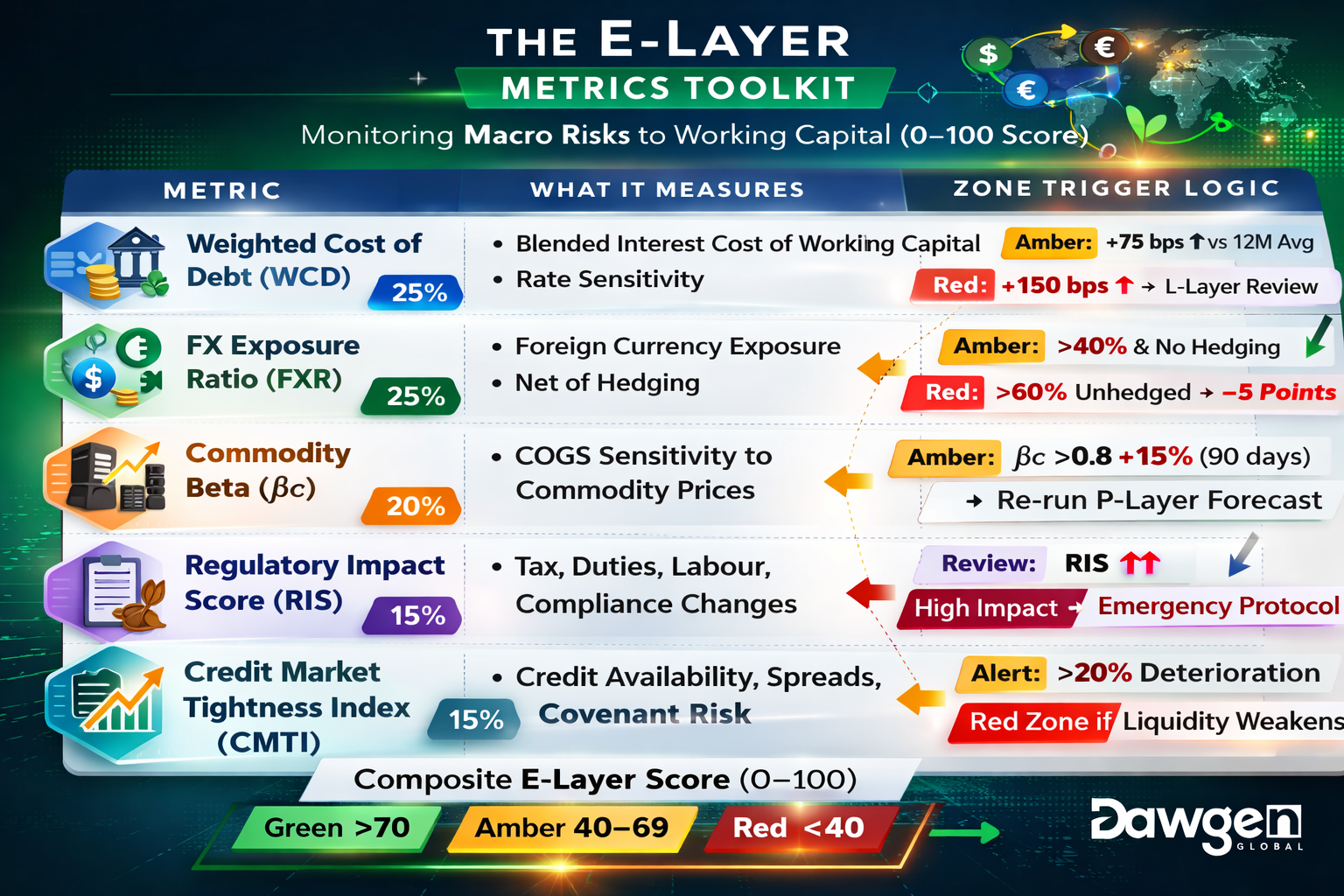

The E-Layer Metrics Toolkit

The E-Layer generates its 0–100 score using five metrics, each calibrated to the client’s specific exposure profile during the PULSE implementation phase.

| Metric | What It Measures | Zone Trigger Logic |

| Weighted Cost of Debt (WCD) | The blended cost of all interest-bearing working-capital facilities, weighted by utilisation. Captures the direct margin impact of rate changes on the financed portion of working capital. | WCD increase of more than 75bps versus the 12-month trailing average triggers an Amber Alert. Increase of more than 150bps triggers a Red Zone evaluation of the L-Layer’s adequacy. |

| FX Exposure Ratio (FXR) | The proportion of total working capital (assets and liabilities) exposed to foreign-currency movements, net of hedging. A higher ratio indicates greater vulnerability to exchange-rate shocks. | FXR above 40% with no hedging programme triggers a standing Amber Alert. An unhedged FXR above 60% imposes a penalty on the composite PULSE Score equivalent to a 5-point deduction. |

| Commodity Beta (βc) | The sensitivity of the organisation’s cost of goods sold to movements in its primary commodity index. A βc of 1.0 means a 10% commodity price increase translates to a 10% COGS increase. | A βc above 0.8 combined with a commodity index increase of more than 15% in the trailing 90 days triggers an Amber Alert and an immediate P-Layer forecast re-run incorporating the new cost structure. |

| Regulatory Impact Score (RIS) | A qualitative-quantitative score capturing pending or recently enacted regulatory changes that will affect working-capital requirements: tax-payment timing, import duties, labour costs, environmental compliance costs. | Any RIS change exceeding a calibrated threshold triggers a Council review to assess budget and forecast implications. High-impact regulatory events (e.g., new tax regime) trigger an Emergency Protocol evaluation. |

| Credit Market Tightness Index (CMTI) | A composite indicator of the availability and cost of external credit in the organisation’s primary borrowing markets. Monitors bank lending appetite, credit spreads, covenant tightness, and facility renewal conditions. | A CMTI deterioration exceeding the 12-month average by more than 20% triggers an L-Layer cross-check. If liquidity depth is also weakening, the combined signal escalates to a Red Zone evaluation. |

The five E-Layer metrics are designed to capture not just the current state of the macro environment but the direction and velocity of change. A stable interest rate is a very different signal from a rate that has increased by 200 basis points over six months and is expected to rise further. The E-Layer’s trend and momentum algorithms distinguish between these states and adjust the layer score accordingly.

Macro Scenario Overlays: Stress-Testing the External Environment

Beyond continuous monitoring, the E-Layer prescribes periodic macro scenario overlays that are injected into the P-Layer’s 13-week forecast to quantify the working-capital impact of plausible macro events. These overlays answer the question that the standard forecast cannot: What happens to our cash if the world changes?

Dawgen Global recommends three standard macro scenarios, run quarterly and refreshed whenever a significant macro event occurs:

- Rate-Shock Scenario: Models the working-capital impact of a 150-basis-point increase in the benchmark lending rate sustained for 26 weeks. The overlay adjusts the cost-of-carry on all floating-rate facilities, models the expected customer-behaviour deterioration based on the interest-rate-to-DSO elasticity calibrated for the client’s customer base, and calculates the net impact on the projected PULSE Score. For a typical Caribbean manufacturer, this scenario typically reduces the composite PULSE Score by 8 to 15 points and can trigger a zone transition from Green to Amber or from Amber to Red.

- FX-Depreciation Scenario: Models the working-capital impact of a 15 per cent depreciation of the local currency against the US dollar sustained for 13 weeks. The overlay reprices all USD-denominated inventory and payables, models the pricing-lag effect on margins, calculates the increased cost of replacing inventory at the new exchange rate, and quantifies the incremental borrowing requirement to fund the gap. For import-dependent Caribbean enterprises, this is often the highest-impact scenario, with potential PULSE Score reductions of 12 to 20 points.

- Commodity-Spike Scenario: Models the working-capital impact of a 25 per cent increase in the client’s primary commodity index sustained for 13 weeks. The overlay adjusts COGS, recalculates DIO in dollar terms, models the supplier-negotiation dynamic that typically accompanies commodity spikes, and assesses the customer-pricing-lag effect. Organisations with high Commodity Beta (βc above 0.8) can see PULSE Score reductions of 10 to 18 points under this scenario.

The scenarios are not predictions. They are stress tests – designed to reveal how much macro-economic headroom the organisation has before it transitions into a less favourable zone. A company whose PULSE Score drops from 72 to 54 under the rate-shock scenario knows that it has approximately 18 points of buffer before the Amber Zone boundary and can calibrate its hedging, pricing, and liquidity strategies accordingly. A company whose score drops from 45 to 28 under the same scenario knows that it is one rate hike away from the Red Zone and must act now to pre-position buffers.

The macro environment does not send calendar invitations. The organisations that survive its shocks are the ones that have already rehearsed their response.

Hedging Strategy Calibrated to the Trigger Zone

One of the most practical applications of the E-Layer is the calibration of hedging strategy to the organisation’s current zone status. Traditional hedging programmes operate on a fixed policy – hedge 50 per cent of FX exposure for the next 12 months, regardless of conditions. The WC-PULSE Framework introduces a dynamic hedging approach that adjusts hedge ratios based on the composite PULSE Score and the specific E-Layer signals.

| Zone | FX Hedge Ratio | Interest-Rate Hedge | Commodity Hedge |

| RED | 75–100% of net exposure hedged for 6–12 months. Prioritise certainty over cost optimisation. Use forwards and options to lock in rates. | Fix 80–100% of floating-rate debt using interest-rate swaps. Eliminate variable-rate exposure that could exacerbate the liquidity crisis. | Hedge 60–80% of primary commodity exposure for 6 months. Use collars to cap downside while allowing some upside participation. |

| AMBER | 50–75% of net exposure hedged for 3–6 months. Balance cost and protection. Review monthly and adjust based on E-Layer score trends. | Fix 50–80% of floating-rate debt. Maintain some variable exposure to benefit from potential rate declines while limiting upside risk. | Hedge 40–60% of primary exposure for 3–6 months. Use a mix of forwards and options for flexibility. |

| GREEN | 25–50% of net exposure hedged for 3 months. Surplus liquidity provides a natural buffer against FX shocks; reduce hedge ratios to lower premium costs. | Fix 25–50% of floating-rate debt. Allow more variable exposure to capture the benefit of potential rate declines. Surplus cash reduces rate sensitivity. | Hedge 20–40% of primary exposure for 3 months. Strong cash position allows greater tolerance for commodity volatility. |

The zone-calibrated hedging approach generates measurable savings. Organisations that reduce hedge ratios in the Green Zone and increase them in the Red Zone typically reduce their annualised hedging costs by 15 to 25 per cent compared to a static hedge policy, while maintaining equivalent or superior risk coverage across the full economic cycle. The savings come from not over-hedging in benign conditions and not under-hedging in stressed ones – a calibration that is only possible when the hedging strategy is connected to a real-time, multi-dimensional risk-assessment engine like the PULSE Framework.

Building Macro Intelligence into the Finance Function

The E-Layer requires the finance function to develop a capability that many mid-market organisations lack: systematic macro-intelligence gathering and translation. This does not mean hiring an economist or subscribing to expensive macro-research services. It means building a structured, lightweight process for monitoring, interpreting, and acting on the macro signals that matter to your specific working-capital position.

The PULSE Framework prescribes a Macro Intelligence Cadence with three components:

- Weekly Signal Scan (15 minutes): The Treasurer or designated analyst reviews a curated set of macro indicators relevant to the E-Layer metrics: the central bank policy rate, the benchmark exchange rates, the primary commodity indices, and a credit-market health indicator. This is not macro-economic research. It is a checklist review of five to eight data points that takes less than fifteen minutes per week and produces a binary assessment: has anything changed materially since last week? If no, proceed with the current PULSE cycle. If yes, trigger a recalculation of the E-Layer score.

- Monthly Macro-Working-Capital Briefing (30 minutes): A structured briefing for the Working Capital Council that translates the month’s macro developments into specific working-capital implications. This briefing is not a macro-economic review. It is an impact-translation exercise that answers three questions: What changed in the macro environment this month? How does it affect each E-Layer metric? And what, if anything, should we do differently in the next four weeks? The discipline of asking these questions monthly ensures that macro awareness is maintained without consuming disproportionate management attention.

- Quarterly Scenario Refresh (Half-day): A facilitated session where the finance team refreshes the three standard macro scenario overlays (rate shock, FX depreciation, commodity spike) using the latest market data and forward curves. This session recalibrates the stress-test parameters, re-runs the overlays through the P-Layer forecast, and updates the Ecosystem Buffer Requirement if the results indicate a material change in macro-driven risk exposure. Dawgen Global facilitates these sessions for clients during the first year of PULSE implementation and transfers the capability to internal teams thereafter.

The total time investment for this macro-intelligence cadence is approximately two hours per month plus one half-day per quarter. The return on that investment is measured in the avoidance of the working-capital surprises that macro events routinely deliver to unprepared organisations.

The Caribbean Context: Why the E-Layer Matters Most Here

The E-Layer has particular significance for enterprises operating in the Caribbean region. The structural characteristics of Caribbean economies – small size, openness, import dependency, limited domestic capital markets, currency pegs or managed floats, and exposure to commodity and tourism cycles – create an operating environment where macro-economic forces have an outsized impact on corporate working capital.

A Jamaican manufacturer that imports 70 per cent of its raw materials in US dollars, sells domestically in JMD, and finances operations through a floating-rate facility denominated in local currency is simultaneously exposed to all three macro channels. A 10 per cent JMD depreciation increases procurement costs immediately but pricing adjustments take 60 to 90 days. A 100-basis-point rate increase raises borrowing costs on the entire working-capital base. And a rise in global commodity prices compounds the FX-driven input-cost increase.

For this manufacturer, the E-Layer is not an optional enhancement to working-capital management. It is an existential capability. Without it, every macro movement is a surprise. With it, each movement is a quantified, pre-modelled scenario with a pre-approved response protocol. The difference is the difference between crisis management and strategic management.

MACRO SHOCKS DON’T WAIT FOR YOUR QUARTERLY REVIEW.

Get Ahead with a PULSE Macro Sensitivity Briefing

Dawgen Global is a full-spectrum advisory firm delivering transformation across Strategy, Finance, Operations, Technology, and Governance. Our Working Capital Advisory practice is powered by the proprietary WC-PULSE Framework™, designed to convert working-capital management from a reactive function into a strategic capability that drives shareholder value. We serve mid-market and large enterprises across the Caribbean, North America, and international markets.

A focused 45-minute session mapping your working-capital exposure to the current rate, FX, and commodity environment. You’ll walk away with a quantified E-Layer Sensitivity Profile, a customised scenario overlay for your 13-week forecast, and a recommended hedging calibration aligned to your current PULSE zone.

| Book Your Briefing Today : info@dawgen.global

The WC-PULSE Thought Leadership Series

Articles 1–6: CCC Blind Spots → Buffer vs. Reprice → 13-Week Crystal Ball → Supplier Ecosystem → Governance Model → Reprice Playbook

Article 7: “Interest Rates, FX Shocks, and Your Balance Sheet: Mastering the E-Layer” (You are here)

Coming Next – Article 8: “The 90-Day Working Capital Transformation: A PULSE Implementation Case Study” – A detailed, step-by-step walkthrough of a real (disguised) client engagement showing how the WC-PULSE Framework delivered US$12 million in released working capital and a 14-day CCC improvement in just 90 days.

About Dawgen Global

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

Email: [email protected]

Email: [email protected]  Visit: Dawgen Global Website

Visit: Dawgen Global Website

WhatsApp Global Number : +1 555-795-9071

WhatsApp Global Number : +1 555-795-9071

Caribbean Office: +1876-6655926 / 876-9293670/876-9265210  WhatsApp Global: +1 5557959071

WhatsApp Global: +1 5557959071

USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements