Executive Summary

Economic downturn risk is rising again in 2026, and for many organisations the real danger isn’t a single headline event—it’s a stack of pressures: softer demand, tighter credit, elevated operating costs, FX volatility, supply chain interruptions, and greater customer sensitivity to price. In the global risk landscape you shared, economic downturn is identified as a material near-term risk, and it often compounds with other risks (misinformation, geopolitical tension, and weather-related disruptions).

This article provides a practical, CFO-and-board-ready playbook for managing downturn conditions without “panic cuts” that damage long-term capability. We focus on six high-impact disciplines:

-

Liquidity defence, 2) cost agility, 3) revenue resilience, 4) working capital excellence, 5) balance-sheet risk controls, and 6) scenario-based decisioning.

We also include composite case studies to show how mid-market Caribbean organisations can protect cash, preserve strategic capacity, and position for recovery—while maintaining governance, transparency, and stakeholder confidence.

1) Why “Economic Downturn” Is Different in 2026

Downturns are not uniform. A 2026 slowdown can be uneven across sectors, markets, and customer segments, and it can emerge from a variety of triggers: persistent geopolitical friction, tighter financial conditions, supply chain shocks, or climate-driven price effects. The challenge for executives is that downturn impacts are often lagged:

-

Demand softens gradually, then contracts suddenly.

-

Customer payment behavior deteriorates before revenue visibly drops.

-

Inventory becomes “sticky” just as cash becomes expensive.

-

Financing availability shifts quickly, especially for SMEs and mid-market firms.

The organisations that perform best don’t try to predict every macro outcome. They build financial and operational resilience so they can adapt faster than competitors.

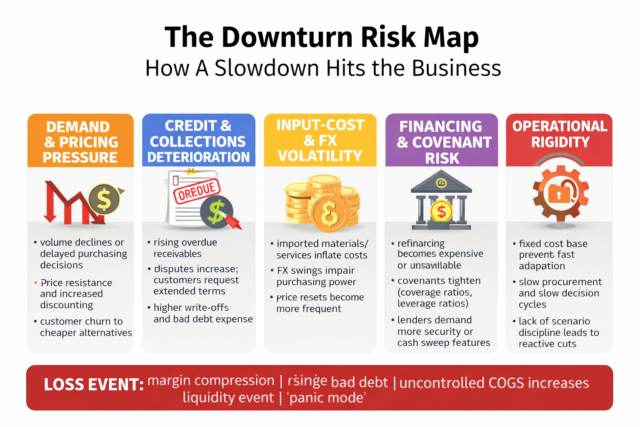

2) The Downturn Risk Map: How a Slowdown Hits the Business

A useful way to manage an economic downturn is to map it to a small set of measurable business exposures:

A) Demand and pricing pressure

-

volume declines or delayed purchasing decisions

-

price resistance and increased discounting

-

customer churn to cheaper alternatives

Loss event: margin compression + volume drop = rapid earnings degradation.

B) Credit and collections deterioration

-

rising overdue receivables

-

disputes increase; customers request extended terms

-

higher write-offs and bad debt expense

Loss event: revenue may be “booked” but cash doesn’t arrive.

C) Input-cost and FX volatility

-

imported materials/services inflate costs

-

FX swings impair purchasing power

-

price resets become more frequent

Loss event: uncontrolled COGS increases and pricing lag.

D) Financing and covenant risk

-

refinancing becomes expensive or unavailable

-

covenants tighten (coverage ratios, leverage ratios)

-

lenders demand more security or cash sweep features

Loss event: liquidity event triggered by financing constraints.

E) Operational rigidity

-

fixed cost base prevents fast adaptation

-

slow procurement and slow decision cycles

-

lack of scenario discipline leads to reactive cuts

Loss event: “panic mode” erodes core capabilities.

3) The Resilience Objective: Survive, Stabilise, and Position for Recovery

The point of downturn planning is not merely to “cut costs.” It is to achieve three outcomes:

-

Survive: protect liquidity, avoid covenant breaches, maintain essential operations.

-

Stabilise: restore cash conversion, align cost base to revenue reality, keep service quality acceptable.

-

Position: preserve strategic capability (talent, core systems, customer relationships) so the business can accelerate when conditions improve.

In downturn conditions, the winning strategy is often disciplined agility: cut what is non-strategic, protect what drives future earnings.

4) Liquidity Defence: Build the “Cash Shock Absorber”

Liquidity is the first line of defence. Organisations fail in downturns primarily due to cash—not profit.

Practical liquidity actions (immediately implementable)

-

13-week rolling cashflow (weekly refresh) as the control centre.

-

Establish a minimum liquidity threshold (e.g., X weeks of operating spend).

-

Create a cash governance routine (Treasury + CFO + Ops) with clear actions triggered by thresholds.

-

Build a liquidity waterfall: operating cash → working capital → discretionary spend → capex → financing options.

Liquidity stress tests to run now

-

10% revenue decline with flat costs for 90 days

-

60-day collections slowdown (DSO increases materially)

-

FX shock on critical imports

-

loss of a top customer (or delayed contract renewal)

Board question to answer: If revenue drops 10–15% and collections slow, how long can we operate without external funding?

5) Cost Agility: Reduce Spend Without Breaking the Business

Cost management in a downturn is often done badly: indiscriminate cuts reduce capability and create downstream failures. The right approach is to classify costs by purpose and flexibility.

Cost segmentation framework

-

Run costs (essential): compliance, core operations, critical systems

-

Grow costs (strategic): sales capacity, product development, customer experience

-

Change costs (transformation): automation, reengineering, restructuring

Then apply controls:

-

Freeze: hiring pauses, non-essential travel, discretionary marketing, low-ROI projects

-

Renegotiate: supplier terms, leases, outsourced services, insurance and logistics

-

Redesign: shift to variable cost models; restructure workflows; consolidate vendors

-

Protect: customer support capability, core systems, key talent, regulatory readiness

Rule: Protect what keeps customers paying and operations stable.

6) Revenue Resilience: Defend What You Have, Then Reprice and Repackage

Revenue resilience is about stabilising demand and improving retention when customers become cautious.

High-impact moves

-

Identify your profit pools: which customers/products generate cash and margin.

-

Build retention plays for your top 20% customers (by margin, not only revenue).

-

Repackage offerings: “good-better-best” tiers, subscription or managed service options, bundles.

-

Strengthen pricing discipline:

-

tighten discount authority

-

move from “price cuts” to “value redefinition”

-

introduce small, frequent adjustments where feasible

-

Watch the early warning signs

-

sales cycle lengthening

-

rising quote-to-close drop-off

-

increased requests for extended terms

-

contract downsizing at renewal

Risk insight: retention is cheaper than acquisition—especially when acquisition costs rise.

7) Working Capital Excellence: Release Cash Locked in the Business

Working capital is often the quickest source of liquidity.

Accounts receivable (AR)

-

segment customers by risk: stable / watch / high risk

-

tighten credit controls for high-risk segments

-

deploy proactive collections cadence

-

introduce payment incentives for early settlement where appropriate

-

use structured dispute resolution to reduce “excuse-driven” non-payment

Inventory

-

improve demand forecasting

-

reduce slow-moving SKUs

-

align procurement to cashflow constraints

-

renegotiate MOQs and delivery schedules

Accounts payable (AP)

-

negotiate extended terms strategically (without damaging critical supply)

-

consolidate suppliers for better bargaining power

-

improve invoice accuracy to avoid late payment penalties

Board question: How much cash can we release from working capital in 30–60 days without compromising supply and service?

8) Balance Sheet Risk: Debt, FX, and Counterparty Controls

Downturns expose hidden balance sheet risks:

-

Debt maturities and covenant headroom (coverage and leverage ratios)

-

FX exposures (imports, foreign-currency debt, USD-linked contracts)

-

Counterparty risk (supplier failures, customer defaults, insurer or lender retrenchment)

Practical controls

-

map all FX exposures and define a clear policy: hedge, natural hedge, or pass-through pricing

-

review debt maturities and refinance early where possible

-

maintain covenant “buffer targets” and escalation triggers

-

evaluate supplier concentration and build alternate sourcing options

9) Scenario-Based Decisioning: Make Better Choices Under Uncertainty

The organisations that struggle in downturns often suffer from “single forecast thinking.” Instead, use three scenarios:

-

Base: mild slowdown, manageable inflation, stable credit

-

Downside: demand shock + collections deterioration + FX pressure

-

Severe: major customer loss + credit tightening + disruption event

For each scenario define:

-

trigger indicators (what tells us we’ve entered this scenario)

-

predefined actions (what we will do within 2 weeks)

-

governance (who approves; what can be delegated)

This becomes your decision engine instead of reactive debates.

10) Composite Case Study: How a Mid-Market Organisation Avoided Panic Cuts

Profile: Mid-sized service firm with recurring contracts and some project-based revenue.

Trigger: customer budgets tighten; collections slow; FX increases the cost of key imported software tools.

Risks:

-

cash squeeze from delayed payments

-

margin compression from higher costs

-

leadership pressure to cut staff quickly

Actions implemented:

-

deployed 13-week cashflow and weekly liquidity controls

-

segmented customers, tightened credit, accelerated collections

-

renegotiated supplier terms and shifted some contracts to usage-based pricing

-

redesigned packages into tiers to retain price-sensitive clients

-

protected client service and key relationship roles

Result:

-

stabilized cash conversion, reduced write-offs, avoided destructive layoffs, and gained market share as competitors cut too deeply.

Lesson: disciplined liquidity + targeted cost agility outperforms panic reductions.

How Dawgen Global Risk Advisory Services Can Help

Dawgen Global supports organisations in converting “downturn fear” into structured resilience—linking finance, operations, and governance.

We can help you:

-

build a 13-week cashflow and liquidity governance model

-

design downturn scenarios with trigger-based action plans

-

implement working capital improvement programs

-

redesign cost base for agility while protecting strategic capability

-

assess balance sheet risks (debt/FX/counterparty)

-

run board-level stress tests and tabletop exercises

Next Step!

A downturn doesn’t have to be a crisis. It can be a strategic advantage—if you manage liquidity, cost agility, and decision speed better than competitors.

Let Dawgen Global help you build a practical downturn resilience program tailored to your business.

🔗 Contact us: https://www.dawgen.global/contact-us/

📧 [email protected]

📞 USA: 855-354-2447

💬 WhatsApp Global: +1 555 795 9071

About Dawgen Global

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

Email: [email protected]

Email: [email protected]  Visit: Dawgen Global Website

Visit: Dawgen Global Website

WhatsApp Global Number : +1 555-795-9071

WhatsApp Global Number : +1 555-795-9071

Caribbean Office: +1876-6655926 / 876-9293670/876-9265210  WhatsApp Global: +1 5557959071

WhatsApp Global: +1 5557959071

USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements