Executive Summary

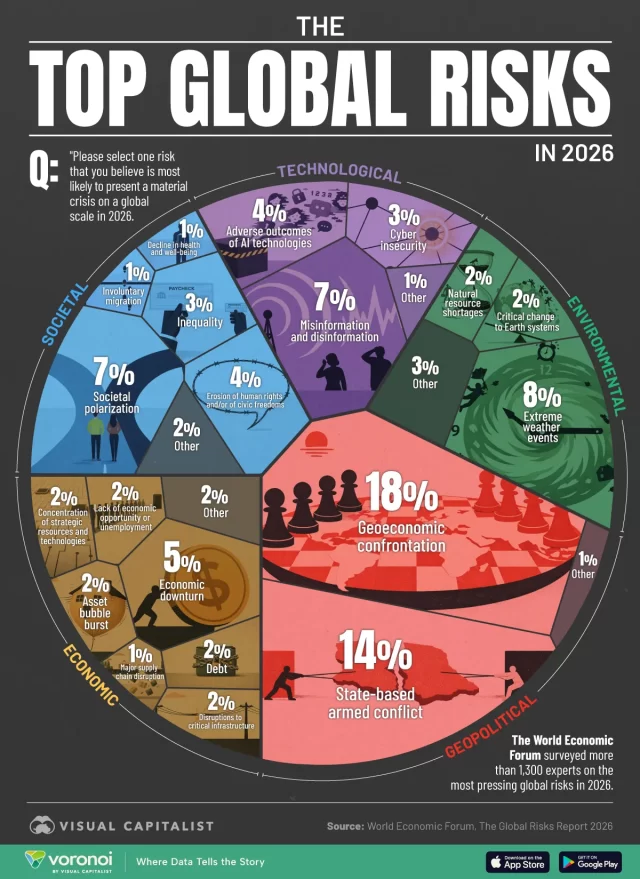

Extreme weather events rank among the most pressing global risks in 2026 and remain a dominant long-term threat in the World Economic Forum’s Global Risks Report 2026 analysis. For organisations across the Caribbean and beyond, “extreme weather” is no longer a compliance or sustainability topic—it is a profitability, liquidity, and continuity topic. Floods, hurricanes, droughts, heatwaves, wildfires, and storm surges can trigger multi-channel losses: damaged assets, operational downtime, supply chain breakdowns, employee disruption, data centre outages, commodity shocks, and insurance repricing.

This article provides a board-ready approach to extreme weather risk: (1) map exposures across the value chain, (2) quantify financial and operational impacts using scenarios, (3) integrate resilience into business continuity and crisis management, (4) harden critical infrastructure and data/IT dependencies, (5) strengthen supplier and logistics resilience, and (6) optimise insurance and risk financing. We also include composite (anonymised) case studies showing how mid-market companies can reduce downtime, stabilise cashflow, and improve recovery speed.

1) Why Extreme Weather Belongs on the Board Agenda in 2026

The global risk landscape has shifted into what the World Economic Forum describes as an “age of competition,” where near-term geopolitical and economic risks collide with longer-term structural pressures, including climate impacts. In this environment, extreme weather is not “background noise”—it is a catalyst that can amplify other risks:

-

Inflation and margin pressure: agricultural shocks, energy disruptions, and logistics constraints feed price volatility.

-

Credit and liquidity risk: downtime reduces cash inflow while recovery costs spike immediately.

-

Insurance availability and affordability: tighter terms, higher deductibles, exclusions, and sub-limits can leave firms underprotected.

-

Supply chain fragility: weather events can shut ports, disrupt roads, and cause upstream supplier failures.

-

Workforce disruption: displacement, commuting breakdowns, illness/heat stress, and school closures affect labour availability.

-

Regulatory and stakeholder scrutiny: lenders, boards, and clients increasingly expect evidence of resilience planning.

The implication is simple: resilience is becoming a competitive advantage. Companies that can maintain service levels through disruptions are better positioned to retain customers, protect reputations, and negotiate more favourable financing and insurance terms.

2) Extreme Weather Risk: It’s Not One Risk—It’s a Portfolio

“Extreme weather” is often treated as a single category, but operationally it behaves like a portfolio of hazards with different impact pathways:

Common hazard types

-

Wind and storm surge: hurricanes, cyclones, tropical storms

-

Flooding: flash floods, river floods, coastal inundation

-

Heat extremes: heatwaves, prolonged high humidity (affecting labour productivity and equipment)

-

Drought: water restrictions, agricultural impacts, hydro-related power constraints

-

Wildfires and smoke: direct damage, air quality impacts, power shutdowns

-

Non-weather natural disasters influenced by climate conditions: landslides following intense rainfall

The six business impact channels

-

Physical asset damage: facilities, fleet, stock, plant and equipment

-

Operational downtime: inability to operate, reduced output, service disruption

-

Supplier and logistics disruption: inbound materials delayed; outbound deliveries interrupted

-

Demand shocks: customers postpone purchases; emergency demand spikes (sometimes beneficial but hard to serve)

-

Financial shocks: working capital swings, higher costs, delayed receivables, FX/commodity impacts

-

People and safety: employee unavailability, health risks, duty-of-care liabilities

Treating extreme weather as a portfolio helps boards and executives avoid generic planning and instead invest in targeted controls that move the needle.

3) A Practical Framework: “Protect, Continue, Recover, Adapt”

Most organisations have fragments of resilience (a BCP, an incident response procedure, some insurance). The gap is often integration: the plan exists, but it is not tested against plausible, financially quantified scenarios.

A strong extreme weather programme can be structured into four linked capabilities:

A. Protect (reduce loss frequency/severity)

-

Site-level hardening: drainage, flood barriers, wind-rated retrofits, roof protection, equipment anchoring

-

Utility resilience: backup power, redundant connectivity, water storage where applicable

-

Asset and maintenance discipline: preventative maintenance schedules; lifecycle upgrades

B. Continue (keep critical operations running)

-

Business Impact Analysis (BIA) that is realistic: define critical services, recovery time objectives (RTOs), and dependencies

-

Alternate operating model: remote work capability; alternate locations; manual workarounds for key processes

-

“Minimum viable service” definition: what you must deliver to protect revenue and customer trust

C. Recover (restore quickly and control costs)

-

Pre-negotiated vendors: restoration contractors, generators, logistics providers, security

-

Spare parts and critical inventory strategy

-

Crisis communications plan: customers, regulators, staff, suppliers, lenders

D. Adapt (learn and reconfigure)

-

Post-incident reviews with metrics (downtime hours, recovery cost vs. insured recovery, customer churn)

-

Capital planning: invest where payback is clear (downtime reduction, claim reduction, insurance improvement)

-

Supplier redesign: dual sourcing, regional alternatives, contract clauses for resilience

4) Quantification: Make the Risk Decisionable

Boards struggle with climate risk when it’s framed as an abstract probability. The move that changes everything is quantification.

Step 1: Map “critical exposure points”

-

Single points of failure (one warehouse, one port, one supplier)

-

High-value assets and revenue-critical systems

-

Locations with known hazard profiles (coastal zones, flood plains, areas with power instability)

Step 2: Build 3–5 operational scenarios

Use scenarios that reflect how the business actually fails, not just the hazard:

-

Scenario 1: 3-day power loss + limited road access

-

Scenario 2: Facility flooding + stock contamination

-

Scenario 3: Port closure + inbound delay + customer penalties

-

Scenario 4: Heatwave + labour productivity reduction + equipment overheating

-

Scenario 5: Multi-site disruption + telecom outage

Step 3: Translate each scenario into financial drivers

-

Revenue loss (by product line and customer segment)

-

Gross margin impact (expedited freight, spoilage, overtime, substitute materials)

-

Working capital (inventory swings, receivables delays)

-

Cash requirements (repairs, relocation, security, temporary facilities)

-

Insurance recovery timing (claims processing lag)

This is where resilience planning becomes CFO-aligned: you can compare the cost of controls versus the reduction in expected downtime and loss.

5) Composite Case Study 1: Distribution Company Facing Repeated Flood Disruptions

Profile: Mid-market distributor with one primary warehouse near a low-lying area.

Symptoms: Repeated storm events caused 2–4 days of disruption each time, with stock loss and delayed deliveries.

What we found (diagnostic):

-

The warehouse had no clear “flood trigger” thresholds (when to move stock, shut operations, reroute deliveries).

-

Customer communications were reactive; service teams had inconsistent messages.

-

Insurance terms had increased deductibles and narrow coverage for certain types of loss.

-

The company had a BCP, but it focused on IT rather than physical distribution continuity.

Resilience actions implemented:

-

Trigger-based playbooks: rainfall thresholds + local flood warnings tied to step-by-step actions.

-

Stock zoning: high-value/high-velocity items moved to elevated racking; critical stock assigned “protected zones.”

-

Alternate delivery model: pre-negotiated local 3PL capacity for emergency cross-docking.

-

Claims readiness: photo documentation protocols and pre-assigned claim roles to speed recovery.

-

Tabletop exercises: quarterly tests aligned to storm season.

Results (within one season):

-

Downtime reduced from days to hours in moderate events.

-

Emergency freight costs dropped due to pre-arranged logistics.

-

Claims documentation improved, reducing disputes and delays.

The lesson: continuity isn’t a document—it’s a trained operating rhythm.

6) Composite Case Study 2: Professional Services Firm With Hidden “Infrastructure Risk”

Profile: Services firm with heavy reliance on digital systems and client-facing commitments.

Symptoms: After a major weather event, staff could not work due to connectivity issues and local power instability, despite “remote work policies.”

What we found:

-

Remote work assumed home internet and electricity were available.

-

The firm’s client deadlines had no contingency clauses.

-

There was no prioritisation of critical client deliverables under disruption.

Resilience actions implemented:

-

Resilient remote model: mobile hotspot pools, backup power for key teams, and priority seating agreements with co-working spaces.

-

Deliverables triage protocol: a client-impact matrix to prioritise deadlines.

-

Client communication templates: proactive scripts and escalation paths.

-

Data resilience review: secondary access routes and tested backups.

Results:

-

Client service continuity improved materially during outages.

-

Reduced reputational damage and reduced staff burnout.

The lesson: digital continuity is still physical continuity—power and connectivity are operational dependencies.

7) Insurance and Risk Financing: Stop Treating Coverage as the Strategy

Insurance is vital, but it is a risk financing tool, not the full resilience plan. The most common failure pattern is “insured but still in distress” because cashflow timing breaks the business.

Practical improvements

-

Policy review aligned to scenarios: confirm coverage triggers match how losses occur (flood definitions, business interruption waiting periods, sub-limits).

-

Claims preparedness: pre-loss documentation, asset registers, and supplier contracts ready for proof-of-loss.

-

Risk retention strategy: decide what you can absorb versus what must be transferred, based on liquidity analysis.

-

Layered recovery funding: working capital facilities, contingent credit lines, and pre-approved spend authorities.

8) Integrating Extreme Weather Into Enterprise Risk and Governance

Extreme weather resilience fails when it is “owned by everyone” and therefore owned by no one. Governance needs clarity:

-

Board oversight: set risk appetite for downtime, safety, and service disruption.

-

Executive sponsor: ensure investment decisions are made and tested.

-

Cross-functional resilience team: operations, finance, HR, IT, procurement, legal/compliance.

-

Metrics and reporting: downtime hours, near-miss incidents, recovery time, insurance claim cycle time, supplier performance during disruptions.

A useful “north star” metric is: time-to-restore critical service (measured, tested, improved).

9) A 30–60–90 Day Implementation Roadmap

If you want momentum without overwhelming the organisation:

First 30 days: Diagnose and prioritise

-

Rapid BIA refresh for critical services

-

Hazard and dependency map (sites, suppliers, utilities, IT)

-

Identify the top 3 single points of failure

Days 31–60: Build playbooks and quantify

-

Scenario set (3–5 scenarios) with financial translation

-

Trigger-based continuity playbooks

-

Vendor pre-negotiation and crisis communications templates

Days 61–90: Test and harden

-

Tabletop exercise + after-action improvement plan

-

Quick-win hardening (drainage, racking, backup power priorities)

-

Insurance alignment review and claims readiness kit

How Dawgen Global Risk Advisory Services Can Help

Dawgen Global supports clients with practical, execution-focused resilience programmes that align risk governance, operational continuity, and financial decision-making. Typical deliverables include:

-

Extreme Weather Risk Diagnostic (sites, utilities, suppliers, and critical services)

-

Board-ready scenario analysis and stress testing (downtime + cashflow)

-

Business Continuity Plan refresh with trigger-based playbooks

-

Crisis governance design (roles, decision rights, escalation, communications)

-

Tabletop exercises and operational testing

-

Insurance and risk financing alignment (claims readiness and coverage gap review)

Next Step!

If extreme weather is treated as “an annual inconvenience,” the organisation will keep paying the same disruption tax—often with compounding costs. The resilient organisations in 2026 will be those that can stay operational, protect cashflow, and recover faster than competitors.

Let’s build your extreme-weather readiness program—practical, tested, and financially grounded.

🔗 Contact us: https://www.dawgen.global/contact-us/

📧 [email protected]

📞 USA: 855-354-2447

💬 WhatsApp Global: +1 555 795 9071

About Dawgen Global

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

Email: [email protected]

Email: [email protected]  Visit: Dawgen Global Website

Visit: Dawgen Global Website

WhatsApp Global Number : +1 555-795-9071

WhatsApp Global Number : +1 555-795-9071

Caribbean Office: +1876-6655926 / 876-9293670/876-9265210  WhatsApp Global: +1 5557959071

WhatsApp Global: +1 5557959071

USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements