Where does each Caribbean jurisdiction stand — and what comes next?

The Gap in the Schedule

When Caribbean businesses reviewed the Meta DST location fee notification of March 2026, they noticed something that many found reassuring at first glance: no Caribbean jurisdiction appeared in the fee schedule. Austria, France, Italy, Spain, Türkiye, and the United Kingdom were listed. Jamaica was not. Trinidad and Tobago was not. Barbados, Guyana, the Cayman Islands — none of them appeared.

This absence is real, but its reassurance is limited and temporary. Caribbean jurisdictions are not in the Meta fee schedule because they have not yet enacted the specific legislative framework that triggers platform-level DST collection obligations. They are not exempt from the global trajectory of digital services taxation. They are simply earlier in that journey.

This article is the definitive Caribbean reference on digital services taxation. We examine where each major Caribbean jurisdiction currently stands — what legislation exists, what is in development, and what the regulatory trajectory looks like. We then assess what businesses should be monitoring and how to read the early warning signals that DST legislation is approaching in a given market.

| How to Read This Article

Each country section uses a status indicator: [Partial Framework] — some digital economy tax measures exist but no standalone DST; [In Development] — DST or equivalent legislation is actively being explored or drafted; [Monitoring] — no current framework but trajectory indicates eventual adoption; [Early Stage] — limited digital economy legislation, longer timeline expected. |

Part 1: The Global Context That Shapes Caribbean Policy

To understand where the Caribbean stands, it is necessary to understand the forces shaping policy trajectories across all small island developing states and developing economy members of the OECD Inclusive Framework.

The OECD Inclusive Framework and Caribbean Membership

The majority of Caribbean jurisdictions are members of the OECD/G20 Inclusive Framework on Base Erosion and Profit Shifting (BEPS). This membership creates a formal commitment to implementing internationally agreed minimum tax standards. As the Two-Pillar Solution — particularly the global minimum tax under Pillar Two — moves toward implementation, Caribbean jurisdictions face direct pressure to enact the required domestic legislation.

Pillar One, which directly addresses the reallocation of taxing rights from platform headquarter jurisdictions to market jurisdictions, is the element most directly analogous to a DST. Its delayed implementation has been one reason Caribbean governments have not felt urgency to enact standalone DSTs — the expectation has been that a multilateral solution would eventually resolve the issue. That expectation is now being tested, and some jurisdictions are reassessing whether to proceed with unilateral measures.

CARTAC and Technical Capacity

The Caribbean Technical Assistance Centre (CARTAC), operated by the International Monetary Fund, plays a crucial role in building fiscal and revenue administration capacity across the region. CARTAC has been actively supporting Caribbean revenue authorities in assessing their readiness for digital economy taxation — conducting diagnostics, training staff, and developing policy frameworks. The pace of CARTAC-assisted preparation is a useful leading indicator of which jurisdictions are moving most quickly toward digital economy tax implementation.

The Fiscal Pressure Factor

Small island economies in the Caribbean face persistent fiscal pressures — narrow tax bases, high debt-to-GDP ratios, vulnerability to external shocks, and the ongoing costs of climate adaptation. The digital economy represents a significant and growing source of economic activity that is substantially undertaxed under current frameworks. For finance ministers across the region, digital services taxation offers a politically palatable route to broadening the tax base — it targets foreign technology corporations rather than local businesses or citizens, making it easier to justify publicly.

This fiscal pressure factor means that DST legislation in the Caribbean is not a question of whether, but when. And in several jurisdictions, the answer to ‘when’ is becoming ‘soon.’

Part 2: Country-by-Country Analysis

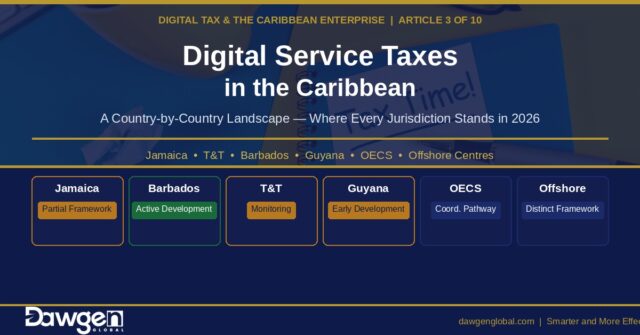

JAMAICA

| Jamaica [Partial Framework — Active Development]

Jamaica has the most developed digital economy tax framework in the English-speaking Caribbean, but has not yet enacted a standalone Digital Service Tax. The existing GCT on digital services is significant but structurally different from the DST model applied by Meta’s location fees. |

Jamaica’s primary mechanism for taxing the digital economy is its General Consumption Tax (GCT) framework, which was extended to cover digital services supplied by non-resident businesses to Jamaican consumers. Under this framework, digital platforms providing services to Jamaican-based customers — including streaming services, software subscriptions, and certain platform services — are required to register for GCT purposes and remit the applicable tax to the Jamaica Revenue Authority (JRA).

This GCT on digital services operates as a consumption tax on the end consumer, collected and remitted by the platform. It is structurally distinct from a Digital Service Tax on the revenues of the platform itself. The GCT captures value at the point of consumption; a DST would capture it at the level of platform revenue derived from advertising or intermediation activity within Jamaica.

The distinction matters for Caribbean businesses. The existing GCT framework primarily affects Jamaican consumers paying for digital subscriptions and services. A DST would affect the economics of digital advertising on platforms that generate advertising revenue from Jamaican audiences — which is the mechanism that creates the Meta-style location fee.

What Is Being Developed

Jamaica’s Ministry of Finance and the Public Service has engaged in active consultation on digital economy taxation as part of its broader tax reform programme. The 2025-26 budget cycle included provisions for further review of the digital economy tax framework, and the JRA has been strengthening its capacity to administer digital economy taxes. Parliamentary discussions have referenced the need to align Jamaica’s framework with the OECD Two-Pillar Solution as it matures.

| Key Watch Signal for Jamaica

Monitor the annual budget speech and the Finance and Public Service Committee for references to digital economy tax reform. The JRA’s publication of consultation documents on digital services taxation will be the clearest advance signal of impending DST legislation. |

TRINIDAD AND TOBAGO

| Trinidad and Tobago [Partial Framework — Monitoring]

Trinidad and Tobago has existing VAT obligations that apply to some digital services but does not have a comprehensive digital economy tax framework. The country’s fiscal situation — shaped by its energy sector revenues — has historically reduced urgency around broadening the non-energy tax base, but that calculus is shifting. |

Trinidad and Tobago’s tax framework includes a Value Added Tax (VAT) that theoretically applies to digital services supplied to T&T consumers, but enforcement against non-resident digital platforms has been limited. The Board of Inland Revenue (BIR) has not yet established a simplified registration and remittance regime for non-resident digital service providers equivalent to those implemented in Jamaica and several other jurisdictions.

The country’s energy sector revenues have historically provided fiscal buffers that reduced pressure to expand digital economy taxation. However, the volatility of energy prices and the long-term trajectory of the global energy transition are creating new fiscal pressures that are shifting the political calculus. Finance ministers have increasingly referenced the need to develop non-energy revenue streams, and digital economy taxation features in several policy documents.

The T&T Business Exposure

Trinidad and Tobago hosts some of the largest and most digitally active businesses in the Caribbean — financial services groups, telecommunications companies, media organisations, and retail conglomerates. Many of these run significant digital advertising campaigns targeting regional and international audiences. Their exposure to Meta’s existing DST location fees — particularly for UK-targeted campaigns — is among the highest in the Caribbean private sector. When T&T eventually enacts its own digital economy tax framework, these businesses will face the most material compliance and cost adjustments.

| Key Watch Signal for T&T

Monitor the Ministry of Finance’s annual revenue review reports and the BIR’s strategic plan publications. Any reference to a ‘digital economy taxation project’ or ‘VAT modernisation for digital services’ is an early indicator of approaching legislation. |

BARBADOS

| Barbados [Active Development — Regional Leader]

Barbados is the Caribbean jurisdiction most actively engaged with digital economy tax policy at both the domestic and international levels. It has signalled clear intent to implement a framework consistent with the OECD Two-Pillar Solution and has made concrete legislative preparations. |

Barbados has been at the forefront of Caribbean engagement with the OECD Inclusive Framework, playing an active role in negotiations on the Two-Pillar Solution. Domestically, the Barbados Revenue Authority (BRA) has implemented VAT obligations for non-resident digital service providers — requiring platforms supplying digital services to Barbadian consumers to register and remit VAT — and has demonstrated effective enforcement of these obligations.

The country’s corporate tax reform programme, undertaken to align with emerging global minimum tax standards, has positioned Barbados as the regional jurisdiction closest to full compliance with the OECD framework. This alignment work has direct implications for digital economy taxation: as Barbados implements the Pillar Two global minimum tax rules, it is also building the institutional and legislative infrastructure that would support a standalone DST or equivalent mechanism.

The Barbados Diaspora and Digital Economy Connection

Barbados has a significant and commercially active diaspora community, particularly in the United Kingdom and North America. Digital advertising targeting the Barbadian diaspora — for tourism, financial services, real estate, and cultural events — is a significant segment of Barbadian business advertising spend. These campaigns are already subject to the UK’s 2% DST location fee through the Meta framework. When Barbados enacts its own digital economy tax measures, it will be doing so as a market that is already integrated into the global DST ecosystem from the advertiser side.

| Key Watch Signal for Barbados

Barbados is the most likely Caribbean jurisdiction to enact DST or equivalent legislation first. Watch for Budget Estimates presentations and the Barbados Revenue Authority’s annual performance reports, which frequently reference the digital economy tax agenda. Legislative action within the 2026-2027 fiscal cycle is plausible. |

GUYANA

| Guyana [Early Development — Rapidly Evolving]

Guyana’s fiscal landscape has been transformed by its oil revenues, creating both the resources and the impetus for comprehensive tax modernisation. Digital economy taxation is on the reform agenda but competes with many other priorities in one of the world’s fastest-growing economies. |

Guyana’s Guyana Revenue Authority (GRA) has been undergoing significant institutional strengthening, supported by the IMF and other development partners, as the country manages the transition to an oil-based fiscal model. This modernisation programme includes capacity building in digital economy tax administration — a foundation that will be necessary before any DST or equivalent framework can be effectively implemented.

The current tax framework in Guyana does not include specific provisions for digital services taxation beyond general income tax and VAT principles that may theoretically apply to some digital transactions. The GRA’s capacity to enforce these provisions against large non-resident digital platforms is currently limited.

The Oil Wealth and Tax Policy Question

Guyana’s extraordinary oil revenues create a different fiscal environment from other Caribbean jurisdictions. The government has access to significant revenues without needing to broaden the tax base in the near term. This reduces the immediate fiscal urgency of digital services taxation. However, economic diversification and tax equity considerations — ensuring that the digital economy contributes to public revenues alongside the resource sector — are increasingly part of the policy conversation. The long-term probability of Guyana enacting digital economy tax legislation remains high.

| Key Watch Signal for Guyana

Monitor the GRA’s capacity building announcements and the Natural Resource Fund Act governance publications. References to ‘digital economy taxation’ in the annual budget speech will signal that the issue has moved from technical preparation to political priority. |

THE EASTERN CARIBBEAN — OECS MEMBER STATES

| OECS (St. Lucia, Antigua & Barbuda, St. Kitts & Nevis, Dominica, Grenada, St. Vincent & the Grenadines, Montserrat) [Early Stage — Coordination Pathway]

The Organisation of Eastern Caribbean States (OECS) member states share a common currency (the Eastern Caribbean dollar) and several harmonised regulatory frameworks. Digital economy taxation is likely to follow a coordinated rather than individual-jurisdiction approach across the OECS. |

The OECS member states are small economies with limited individual capacity to design and administer novel tax frameworks. The most efficient pathway to digital economy taxation for these jurisdictions is likely through coordinated OECS-level policy development, potentially followed by harmonised domestic legislation across member states simultaneously.

The Eastern Caribbean Central Bank (ECCB) and the OECS Commission have both referenced the digital economy in their strategic plans. The OECS Commission’s work on digital transformation creates a natural platform for digital economy tax policy development, though the timeline for legislative action remains uncertain.

Individual OECS member states do have VAT frameworks that could theoretically be extended to cover digital services, and some have begun informal assessments of their digital economy tax exposure. However, formal legislation is unlikely to precede regional coordination.

THE CAYMAN ISLANDS AND OFFSHORE CENTRES

| Cayman Islands / BVI / Other Offshore Centres [Distinct Framework — No Income Tax Base]

The Caribbean’s offshore financial centres occupy a unique position in the digital tax landscape. With no income or corporate taxes, they do not have the tax infrastructure to implement DST-style levies. Their exposure is primarily as advertiser jurisdictions — businesses based there face Meta’s location fees when targeting DST-jurisdiction audiences. |

The Cayman Islands, British Virgin Islands, Bermuda, and similar jurisdictions have no corporate income tax and no VAT. Their tax frameworks are fundamentally different from those of the onshore Caribbean jurisdictions. Digital Service Tax legislation — which in most jurisdictions is built on top of, or alongside, existing corporate or VAT frameworks — does not map cleanly onto these zero-tax environments.

However, the global minimum tax under OECD Pillar Two creates direct pressure on these jurisdictions. Several have already enacted domestic minimum top-up taxes to retain the tax revenue that would otherwise flow to other jurisdictions under the Pillar Two rules. This represents the most significant tax policy development in the offshore Caribbean in decades, and it is part of the same global tax reform process that is driving DST adoption elsewhere.

Businesses domiciled in Caribbean offshore centres but operating commercially and advertising to global audiences are fully subject to Meta’s DST location fees on their advertising spend into the six current jurisdictions. Their exposure is not reduced by their home jurisdiction’s tax status.

Part 3: CARICOM and the Regional Harmonisation Pathway

CARICOM’s Position on Digital Economy Taxation

The Caribbean Community (CARICOM) has addressed digital economy taxation at the level of the Conference of Heads of Government and through its Council for Finance and Planning (COFAP). CARICOM’s general position is supportive of the OECD Two-Pillar framework as the primary vehicle for addressing digital economy taxation, with unilateral DST measures viewed as a transitional instrument that carries trade retaliation risks.

CARICOM’s concern about unilateral DSTs is not merely theoretical. The United States has historically threatened trade measures — including tariffs — against countries that implement digital services taxes targeting US technology companies. This geopolitical dimension has made CARICOM member states cautious about moving ahead of a multilateral consensus, particularly given the significant US-Caribbean trade and tourism relationship.

The Tension Between Multilateralism and Fiscal Urgency

The tension within CARICOM is between the multilateralist instinct — wait for the OECD process to produce a framework that all jurisdictions can implement simultaneously — and the fiscal urgency argument — regional governments are leaving significant revenues on the table while waiting for a global consensus that continues to be delayed.

This tension is likely to resolve in favour of selective unilateral action in the jurisdictions with the strongest fiscal pressures and the most developed administrative capacity. Barbados and Jamaica are the most likely first movers, potentially followed by Trinidad and Tobago. The OECS member states are likely to wait for a coordinated regional framework.

CARTAC’s Role as Preparation Catalyst

CARTAC’s technical assistance programme has become a de facto preparation pipeline for Caribbean digital economy tax legislation. When CARTAC announces a digital economy tax assessment or workshop in a given jurisdiction, it is a reliable early indicator that formal policy development is likely within 12 to 24 months. Regional finance officials and business leaders should track CARTAC’s published programme of work as a leading indicator of the regional DST timeline.

| Dawgen Global Monitoring Service

Dawgen Global tracks digital economy tax legislative developments across all Caribbean jurisdictions and provides quarterly briefings to advisory clients on the regional DST landscape. Contact your Dawgen Global advisor or visit dawgenglobal.com to subscribe to our Digital Tax Monitor. |

Part 4: The Early Warning Framework — What to Watch For

Caribbean businesses planning for the eventual arrival of domestic DST legislation need a systematic way to monitor the policy environment. The following framework identifies the key signals to watch in each jurisdiction, organised by the stage of legislative development they represent.

Stage 1 Signals — Policy Formation (12–36 months before legislation)

- CARTAC announces a digital economy tax capacity assessment or workshop in the jurisdiction

- Finance ministry publishes a ‘digital economy’ or ‘tax modernisation’ consultation document

- Revenue authority strategic plan references digital economy compliance as a priority

- Parliamentary or senate committee holds hearings on digital economy regulation

- Government signs or ratifies OECD Pillar Two implementing legislation in related areas

Stage 2 Signals — Legislative Preparation (6–18 months before legislation)

- Draft legislation or exposure draft is published for public consultation

- Finance minister references specific DST revenue projections in budget speech

- Revenue authority publishes digital services provider registration guidance

- Bilateral tax treaty with a major platform jurisdiction is amended or renegotiated

- Government announces intended effective date for new digital economy tax measures

Stage 3 Signals — Imminent Implementation (0–6 months before legislation)

- DST or digital economy tax bill is tabled in parliament

- Revenue authority publishes platform registration requirements and rate schedule

- Finance minister confirms implementation date in budget address

- Tax authority issues guidance on compliance obligations for advertisers and businesses

- Platform providers (Meta, Google, etc.) issue notifications to advertisers in the jurisdiction

| Strategic Implication

Caribbean businesses should not wait for Stage 3 signals to begin preparing. The compliance infrastructure — accounting systems, documentation protocols, budget frameworks, and advisor relationships — should be established at Stage 1. By Stage 3, businesses with preparation in place will experience implementation as an administrative update. Those without preparation will face simultaneous system changes, budget overruns, and compliance risk. |

Part 5: The Competitive Positioning Question

There is a final dimension to the Caribbean DST landscape that is often overlooked in purely compliance-focused analyses: the competitive positioning implications for businesses that take early advisory action versus those that wait.

When DST legislation arrives in Caribbean jurisdictions, it will create immediate compliance requirements for businesses that use digital advertising platforms. Businesses with established accounting frameworks, documented processes, and advisor relationships will be able to adapt quickly. Their competitors without these foundations will face higher compliance costs, greater risk of errors, and potential penalties.

More significantly, the businesses that understand DST mechanics in advance will be better positioned to optimise their advertising strategies in response to the new cost environment. They will know which platform spend is DST-exposed, which audience targeting choices carry higher effective costs, and how to recalibrate ROI metrics appropriately. This strategic awareness translates directly into more efficient marketing investment — a competitive advantage that compounds over time.

Not If, But When — and Whether You Are Ready

The Caribbean’s current absence from Meta’s DST fee schedule is a snapshot of the regulatory present, not a prediction of the regulatory future. Every significant Caribbean jurisdiction is moving — at different speeds, through different institutional pathways, and under different fiscal pressures — toward some form of digital economy taxation.

The businesses and advisors that treat this moment as preparation time rather than reprieve time will be better positioned when the regulatory present changes. The country-by-country analysis in this article provides a framework for that preparation — identifying where the signals are strongest, where the timelines are longest, and what to watch for as the Caribbean DST landscape evolves.

In the next article — Article 4 — we turn from the policy landscape to the financial fundamentals: how DST costs affect advertising budgets and ROI, and what a Caribbean business needs to do to recalibrate its digital marketing economics for the DST era.

Dawgen Global is the Caribbean’s leading professional services firm, headquartered in New Kingston, Jamaica. Our tax and advisory teams monitor digital economy tax developments across all Caribbean jurisdictions and help businesses and professional advisors build the frameworks they need to stay ahead of a rapidly evolving regulatory landscape. Visit dawgen,global or contact Dawgen Global office at : [email protected]

About Dawgen Global

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

Email: [email protected]

Email: [email protected]  Visit: Dawgen Global Website

Visit: Dawgen Global Website

WhatsApp Global Number : +1 555-795-9071

WhatsApp Global Number : +1 555-795-9071

Caribbean Office: +1876-6655926 / 876-9293670/876-9265210  WhatsApp Global: +1 5557959071

WhatsApp Global: +1 5557959071

USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements