In almost every part of the world, one rule of aviation economics quietly holds true: the moment your journey crosses a border, the tax bill jumps.

Two flights may be similar in distance and aircraft type, but if one is domestic and the other is international, the passenger on the international leg will usually pay more in specific taxes on their ticket—even before airport fees, fuel surcharges, or VAT are added.

Using the insights from recent IATA analysis on specific taxes on the use of air transport, this article explores why crossing borders costs more, how big the gap between domestic and international taxation has become, and what it means for passengers, airlines, tourism-dependent economies, and policymakers.

1. Domestic vs International: The Numbers Behind the Story

Globally, governments collected around USD 60.4 billion in specific taxes on air passenger tickets in 2024. These are fixed per-passenger charges that apply simply because someone flies, and they exclude VAT, airport charges, fuel excise and corporate income taxes.

The key split is revealing:

-

International flights

-

Specific ticket tax revenue: roughly USD 38.0 billion

-

Average tax per passenger per flight: around USD 17.7

-

Average tax per round trip (outbound and inbound): about USD 43.9

-

-

Domestic flights

-

Specific ticket tax revenue: around USD 22.4 billion

-

Average tax per passenger per flight: about USD 8.5

-

Average tax per round trip: roughly USD 18.9

-

On a simple per-flight basis, international journeys are taxed at more than double the rate of domestic ones on average. That difference becomes even more dramatic once you consider:

-

Multiple flight segments in a single international journey,

-

Layered taxes from origin, destination and sometimes transit states,

-

Additional tourism or solidarity taxes that apply only to foreign arrivals or departures.

From the passenger’s perspective, the result is clear: going abroad costs more in taxes than staying within your own borders, even before you look at base fares.

2. Why Governments Target International Passengers

Governments rarely say, “We prefer to tax foreign visitors,” but the design of many tax systems shows that in practice they often do.

Several reasons explain why international travel is taxed more heavily:

1. Who Pays: Residents vs Non-Residents

International travellers are more likely to be:

-

Non-residents, particularly tourists and business visitors,

-

Higher-income individuals, especially on long-haul routes,

-

People who cannot avoid flying due to geography (e.g., island destinations).

Politically, it is easier to introduce or increase taxes that fall largely on non-voters or on groups perceived as having greater ability to pay. A departure tax on foreign tourists is often more acceptable than a higher domestic income tax or VAT rate.

2. Perception of “Luxury”

Historically, international air travel has been seen as a luxury good, even though in many markets it is now a mass-access mode of transport. This perception has encouraged:

-

Higher tax rates on international journeys,

-

Additional levies labelled as “travel” or “luxury” taxes,

-

Limited political resistance compared with everyday consumption taxes.

3. Border Controls and Security Costs

Governments incur extra costs at borders for:

-

Immigration and customs control,

-

Security screening,

-

Health and biosecurity measures.

Rather than funding these from general taxation, many states recover them via per-passenger international charges, structured as fixed taxes or quasi-fees. Over time, these often grow beyond strict cost recovery.

4. Tourism and Solidarity Funding

Some countries add tourism levies or solidarity taxes to international tickets to:

-

Fund tourism promotion and infrastructure,

-

Support social programmes (e.g., health initiatives in other countries),

-

Create a visible link between visitors and perceived impacts.

These measures are almost always limited to international air passengers, not domestic ones.

3. Layer Upon Layer: How International Taxes Stack Up

The higher burden on international travel is not just about one tax being larger than another. It is often about multiple taxes stacking up on the same journey.

A typical international itinerary can involve:

-

Origin country’s specific passenger tax

-

Destination country’s arrival or departure tax

-

Transit state charges, if applicable (some jurisdictions tax passengers even if they are only transiting)

-

Additional tourism, solidarity, or environmental levies targeted at international travellers

By contrast, a domestic journey generally involves:

-

A single jurisdiction,

-

Fewer layered charges,

-

Often lower or zero specific ticket taxes.

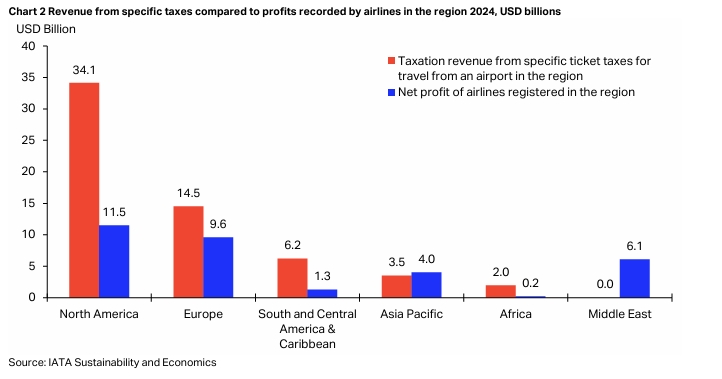

In regions like South and Central America & the Caribbean, this stacking effect is especially pronounced. Nearly all specific ticket tax revenue there is collected on international passengers, and the average specific tax per international flight in the region is close to USD 45. For many long-haul travellers connecting through a high-tax hub and into a regional destination, the total tax bill can easily reach USD 50–100 or more, just in fixed per-passenger charges.

4. The Impact on Passengers: Price and Behaviour

From a passenger’s perspective, higher international ticket taxes affect both what they pay and how they travel.

Higher All-In Prices

Even if base fares are competitive, specific international taxes:

-

Increase the minimum possible ticket price,

-

Represent a larger share of the total cost for price-sensitive travellers,

-

Can make it difficult for airlines to offer attractive “headline” fares.

A USD 40–60 increase on a long-haul return ticket may be manageable for some travellers, but it can be a deciding factor for:

-

Families,

-

Students,

-

Low-income diaspora travellers,

-

Tourists considering several competing destinations.

Travel Frequency and Destination Choice

When international travel taxes push up the cost of flying:

-

Some travellers simply fly less often, especially for discretionary trips,

-

Others switch destinations, favouring places where access is cheaper,

-

In regions with viable land or sea alternatives, some may switch modes for short or medium distances.

Over time, these behavioural shifts can subtly reshape global tourism and business travel patterns.

5. Airlines: International Taxes and Route Viability

For airlines, the domestic vs international tax gap directly influences route economics.

Thin Margins vs Thick Taxes

As noted in earlier analysis, in 2024 global airlines earned around USD 6.8 of net profit per passenger per flight, while average specific ticket taxes per flight were about USD 12.6, and closer to USD 17.7 for international flights.

When:

-

A single government can levy USD 30–100+ per international passenger in specific taxes, and

-

Airlines earn single-digit dollars of profit per passenger,

it becomes obvious that tax policy can make or break a route.

Route Selection and Capacity Deployment

Airlines decide where to fly based on after-tax profitability. Heavy international tax regimes can:

-

Discourage airlines from opening new routes,

-

Lead to lower frequencies or seasonal operation only,

-

Push carriers to route traffic through lower-tax hubs instead of higher-tax origin or destination airports.

For tourism-dependent or trade-oriented economies, reduced air service can mean fewer visitors, less investment, and weaker integration into global supply chains.

6. Tourism and Trade: When Borders Become Fiscal Barriers

International air travel is critical not just for leisure, but for trade, investment, education, and services exports. Heavier taxes on cross-border flights therefore have far-reaching economic consequences.

Tourism-Dependent Economies

In many small island and coastal states, tourism accounts for a large share of GDP and employment. For such economies, international air links are primary arteries for:

-

Visitor arrivals,

-

Foreign exchange inflows,

-

Jobs in hotels, restaurants, transport, and supporting sectors.

When specific ticket taxes on international arrivals and departures become too high:

-

Some price-sensitive tourists choose competing destinations with lower taxes and cheaper air access,

-

Tour operators and airlines shift capacity to markets where packages are easier to sell,

-

Local businesses reliant on steady visitor flows feel the strain first.

A modest-looking tax increase per passenger can therefore translate into a disproportionate economic impact once reduced visitor spending and employment are taken into account.

Trade and Global Business

International flights also facilitate:

-

Business travel for deal-making and client relationships,

-

Participation in trade fairs, conferences, and regional value chains,

-

Mobility of professionals, students, and skilled workers.

Higher border-crossing costs can:

-

Raise the cost of doing business internationally,

-

Discourage smaller firms from exploring export markets,

-

Reduce the frequency of in-person engagement that builds trust and networks.

For developing economies trying to diversify beyond commodities or low-value tourism, affordable international connectivity is a strategic asset—not just a convenience.

7. Equity and Inclusion: Who Pays the Price of Crossing Borders?

Although international air travel is sometimes still treated as a luxury, in many regions it is the only practical mode for:

-

Visiting family abroad,

-

Accessing specialised healthcare,

-

Pursuing education,

-

Migrant workers returning home.

In these contexts, heavy international ticket taxes have a direct social impact.

Diaspora and VFR (Visiting Friends and Relatives) Travel

In countries with large diasporas, people abroad often travel home regularly for:

-

Family events and funerals,

-

Cultural and religious festivals,

-

Property and small-business management.

Fixed international ticket taxes are regressive:

-

They take a larger share of income from lower- and middle-income migrants than from high earners,

-

For families with children, the per-person tax multiplies, making travel much more expensive.

The result is a de facto tax on family ties and cultural connection.

Residents of Remote and Island States

For populations in islands and remote regions, crossing borders for:

-

Education,

-

Work opportunities,

-

Medical treatment,

often requires air travel. High international taxes therefore function as a barrier to mobility, constraining access to opportunities that citizens in larger, better-connected countries may take for granted.

8. Climate Arguments and International Travel Taxes

Because long-haul flights are emissions-intensive, some governments have linked higher international ticket taxes to climate objectives. However, the design of these taxes does not always align well with environmental principles.

The Design Problem

Many international ticket taxes:

-

Are flat per passenger, not based on actual emissions or fuel burn,

-

Do not reward airlines or passengers for choosing more efficient aircraft or routes,

-

Are not reliably earmarked for climate or sustainability spending.

At the same time, aviation emissions on international routes are increasingly addressed through market-based mechanisms such as CORSIA or regional emissions trading schemes.

Risk of Double Charging

If a state imposes:

-

A generic international ticket tax labelled as “green”, and

-

Its airlines or routes are already covered by an emissions scheme,

there is a risk of double charging the same activity without delivering proportional environmental benefits.

For climate goals, well-designed carbon pricing and support for sustainable aviation fuels, efficiency improvements and technology are generally more effective than simply loading more flat tax onto international passengers.

9. Rethinking the Border Premium: Policy Options

Recognising that crossing borders currently attracts a heavy tax premium, what can policymakers do?

1. Map and Benchmark the Gap

Governments should start by:

-

Quantifying the difference between domestic and international ticket taxes,

-

Comparing their international tax levels with those of competing destinations and hubs,

-

Identifying where they are outliers in terms of burden.

This basic benchmarking can highlight cases where international travel is taxed more heavily than is justified by costs or policy goals.

2. Distinguish Cost Recovery from Pure Taxation

Where additional border-related costs exist (immigration, customs, security):

-

These can be set as transparent, cost-based charges,

-

Periodically reviewed to ensure they reflect genuine expenditure.

Beyond that, pure revenue-raising taxes on international travel should be assessed separately, with clear justification.

3. Consider the Full Economic Impact

Before raising or creating an international ticket tax, policymakers should consider:

-

Expected demand impact on inbound and outbound travel,

-

Effects on tourism receipts and jobs,

-

Consequences for trade, investment, and human mobility,

-

Long-run implications for the tax base as a whole.

In some cases, a lower international tax rate that sustains higher passenger volumes may generate greater net benefits than a high rate that suppresses demand.

4. Protect Essential Mobility

For certain categories, states may explore:

-

Reduced or zero rates for medical travel, students, or other vulnerable groups,

-

Special regimes for residents of remote areas where flying abroad is not luxury but necessity,

-

Regional agreements that reduce barriers to intra-regional movement.

Such measures must be carefully designed to prevent abuse, but they can improve social equity and opportunity.

5. Integrate with Climate and Tourism Strategies

Finally, international ticket taxes should be embedded within broader strategies:

-

If climate is a priority, taxes should be clearly linked to emissions and integrated with carbon markets or offset schemes, with credible earmarking of revenues.

-

If tourism is a growth engine, aviation tax policy must align with destination marketing, infrastructure investment, and product development, not undermine them.

10. Making Crossing Borders Affordable and Sustainable

Today, the data are clear: crossing borders by air attracts a significantly heavier tax burden than staying within them. International passengers pay more per flight, contribute the majority of specific ticket tax revenue, and often face multiple layers of origin, destination, and transit charges.

This pattern reflects understandable political and fiscal incentives. But it also carries costs:

-

It can dampen tourism, trade and investment,

-

It can limit mobility for lower-income travellers and diaspora communities,

-

It can weaken airline economics and discourage route development,

-

It can deliver relatively small fiscal gains at the expense of wider growth.

The goal is not to eliminate air travel taxes, but to rebalance and redesign them:

-

So that they are proportionate, transparent and fair;

-

So that they support, rather than undermine, sustainable connectivity;

-

So that climate ambitions are pursued with targeted, efficient tools rather than blunt border surcharges.

If governments can achieve that balance, crossing borders by air can remain both affordable and economically enabling, while still contributing its fair share to public finances and climate solutions.

About Dawgen Global

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

✉️ Email: [email protected] 🌐 Visit: Dawgen Global Website

📞 📱 WhatsApp Global Number : +1 555-795-9071

📞 Caribbean Office: +1876-6655926 / 876-9293670/876-9265210 📲 WhatsApp Global: +1 5557959071

📞 USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements