Executive Summary

Covenants are not “bank paperwork.” They are the operating rules that determine how much strategic room management has when performance deviates from plan. In volatile markets, the difference between a resilient capital structure and a fragile one is rarely the headline interest rate—it is covenant durability: the size and quality of headroom, the testing mechanics, the cure toolkit, and the definition of EBITDA and debt that sits underneath the ratios. This article (Part 9 of Dawgen Global’s C.A.P.I.T.A.L. Architecture™ series) explains how to design covenant packages that protect lenders while preserving management’s ability to invest, adapt, and refinance—without walking into an avoidable default.

1) What Covenants Really Do

At their best, covenants serve three functions:

-

Early warning system – signals stress before liquidity breaks.

-

Risk guardrails – limits leverage and ensures debt service capacity.

-

Governance mechanism – creates a framework for lender engagement when performance deteriorates.

At their worst, covenants act as tripwires—triggering technical default even when the business is fundamentally viable.

Dawgen lens: A covenant breach is often not a “business failure.” It is a contract design failure—mismatched to cashflow volatility, reporting cadence, or the operating cycle.

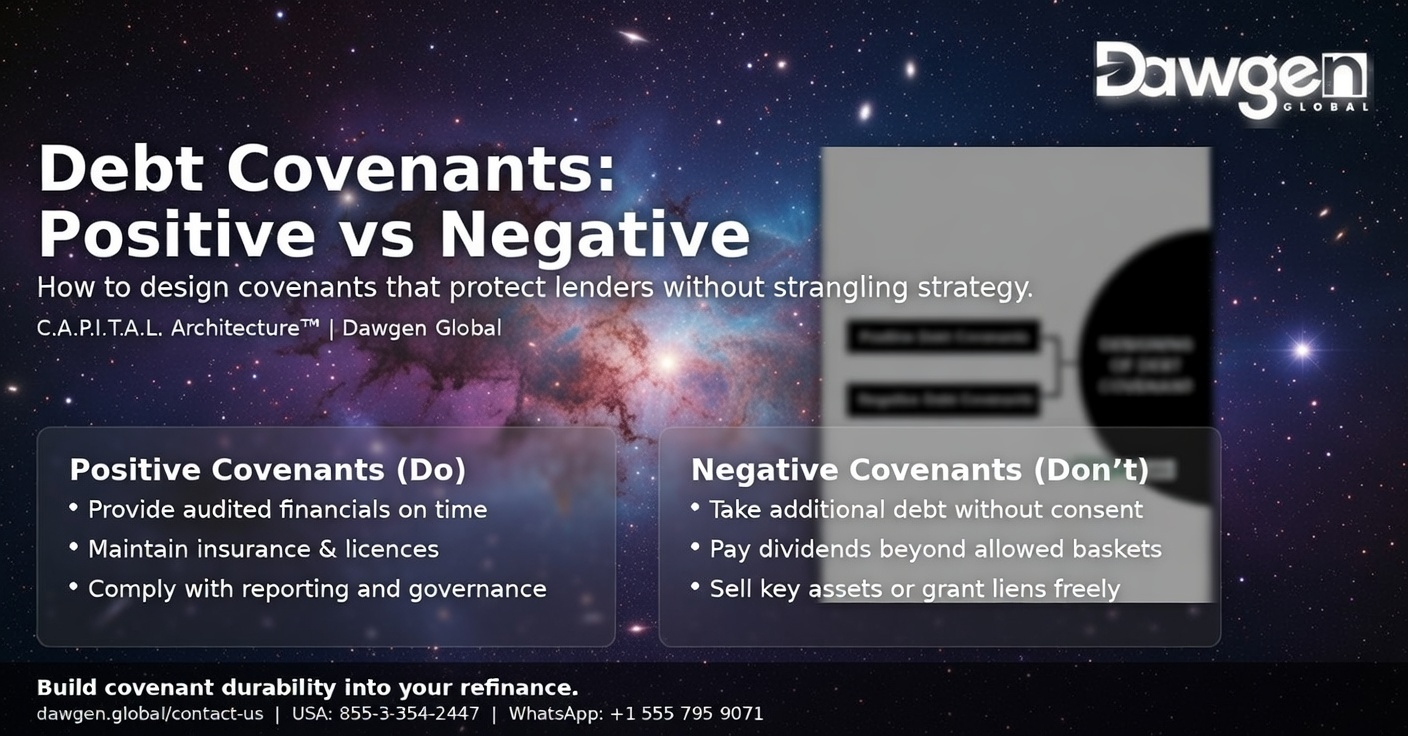

2) The Covenant Toolkit: What You’re Really Negotiating

Covenant packages are more than one ratio. They are a system:

A) Maintenance covenants (tested regularly)

Common examples:

-

Net Debt / EBITDA

-

EBITDA / Interest (Interest Cover)

-

Debt Service Coverage Ratio (DSCR)

-

Minimum liquidity (cash + undrawn committed lines)

These are powerful—and dangerous—because they are tested regardless of whether you take action.

B) Incurrence covenants (tested only if you do something)

Typical in bond/notes-style structures:

-

additional debt capacity

-

restricted payments (dividends)

-

asset sales and reinvestment

-

acquisitions and investments

Key difference: Maintenance covenants drive day-to-day flexibility; incurrence covenants govern strategic moves.

C) Reporting & information undertakings

Slow reporting can create default risk. Lenders price uncertainty—and enforce delays.

3) Headroom Isn’t a Percentage—It’s a Downside Story

Many boards ask: “How much headroom do we have—10%?”

That’s the wrong question.

The right question: “How much headroom do we have in the downside case?”

Because covenants fail in stress, not in base case.

Dawgen practice: Headroom must be tested against:

-

demand contraction

-

margin compression

-

working capital shock

-

FX depreciation (if debt is USD and revenues are local currency)

-

rate increases (floating exposure)

-

delayed receivables / customer concentration events

4) Four Common Reasons Covenant Headroom Collapses

1) EBITDA definition risk

The covenant “EBITDA” may not match management EBITDA. Problems include:

-

aggressive add-backs not accepted by lenders

-

one-off costs recurring every year

-

insufficient documentation for adjustments

-

IFRS / accounting policy changes affecting calculations

2) Working capital cycle ignored

Businesses with seasonal or lumpy cash flows often fail DSCR-style tests when covenants are not aligned to operating reality.

3) FX and interest rate volatility not embedded

If debt is USD but revenue is local currency, a depreciation can break leverage and coverage even with flat operations.

4) Step-downs set too early

Ratios that “tighten over time” can become unrealistic if growth or margin expansion does not materialize.

5) The Dawgen Covenant Engineering Framework

Dawgen designs covenant systems using five engineering principles:

Principle 1: Align covenants to cashflow volatility

-

stable cashflows: leverage + interest cover may be acceptable

-

volatile cashflows: minimum liquidity + springing leverage may be safer

-

project finance-like cashflow: DSCR can be appropriate

Principle 2: Make headroom meaningful and measurable

-

stress test to define the minimum headroom threshold

-

ensure the covenant fails after liquidity becomes the primary concern, not before

Principle 3: Use “liquidity-first” architecture where appropriate

A minimum liquidity covenant can be more economically rational than tight leverage covenants for cyclical businesses.

Principle 4: Design the cure toolkit before you need it

Key tools include:

-

equity cure rights (how many times, how applied)

-

EBITDA cures (limited, well-defined)

-

covenant holiday / reset triggers

-

permitted disposals and reinvestment flexibility

-

prepayment mechanics without punitive break costs

Principle 5: Engineer definitions and baskets like an operating manual

The real covenant negotiation is usually hidden inside:

-

“Net Debt” definition (cash netting, restricted cash, leases)

-

“EBITDA” definition (add-backs, pro-forma adjustments)

-

restricted payments baskets and builder baskets

-

permitted liens and negative pledge

-

acquisitions/investments baskets

-

change-of-control definitions and cross-default thresholds

6) Maintenance vs Springing Covenants: A Practical Choice

A springing covenant only becomes active when utilization crosses a threshold (e.g., RCF draw > 35%).

This can be a powerful compromise:

-

lenders get protection when liquidity is tight

-

management retains flexibility when liquidity is healthy

Dawgen view: For many mid-market borrowers, a springing covenant structure paired with a minimum liquidity covenant creates a more resilient system.

7) Negotiating Strategy: What to Ask For (Without Losing Credibility)

Covenant requests must be backed by analytics. Effective asks include:

-

Replace tight leverage covenant with minimum liquidity covenant

-

Add seasonality adjustments or test on rolling averages

-

Delay step-downs or tie them to achieved milestones (not dates)

-

Ensure add-backs are documentable and capped

-

Build realistic baskets for capex, acquisitions, and working capital needs

-

Include cure rights and clear waiver mechanics

The Dawgen rule: If you can’t explain the covenant package in plain language to the board, it is too risky to sign.

8) Case Study

A growing regional group refinanced into a tighter leverage covenant based on optimistic projections. A mild margin dip and FX move reduced EBITDA in reporting terms, triggering a technical breach despite adequate cash.

Dawgen redesign:

-

shift to minimum liquidity covenant + springing leverage

-

clarify EBITDA add-backs and cap them

-

embed FX stress logic in covenant planning

-

re-stage step-downs after verified performance

Outcome: Improved covenant durability and reduced default risk without meaningfully increasing lender risk.

Key Takeaways

-

Covenants determine strategic freedom in stress—not in calm markets.

-

Headroom must be designed around downside scenarios, not base-case budgets.

-

Definitions (EBITDA, Net Debt) are often more important than the ratio itself.

-

Liquidity-first structures and springing covenants can materially reduce fragility.

-

A cure toolkit is part of responsible governance, not a sign of weakness.

Next Step: Covenant Durability Is Capital Structure Strategy

Dawgen Global helps boards and CFOs engineer covenant systems that balance lender protection with real operating flexibility—through modelling, stress-testing, negotiation support, and capital architecture redesign.

🔗 Contact us: https://www.dawgen.global/contact-us/

📧 [email protected]

📞 USA: 855-354-2447

💬 WhatsApp Global: +1 555 795 9071

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

Email: [email protected]

Email: [email protected]  Visit: Dawgen Global Website

Visit: Dawgen Global Website

WhatsApp Global Number : +1 555-795-9071

WhatsApp Global Number : +1 555-795-9071

Caribbean Office: +1876-6655926 / 876-9293670/876-9265210  WhatsApp Global: +1 5557959071

WhatsApp Global: +1 5557959071

USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements