A Dawgen RISE-360™ guide for Jamaica and the Caribbean

After a hurricane, getting money flowing quickly and fully depends on the strength of your claims and relief dossier—not just the damage itself. Payments stall when evidence is thin, numbers aren’t reconciled, or policy terms aren’t mapped to losses. This article delivers a step-by-step, field-ready method to build auditor-grade claims packs that insurers, adjusters, and regulators can approve with minimal friction. It aligns to the Dawgen RISE-360™ phases: capture evidence in Impact, frame quantum in Stabilization, and turn approvals into Elevation funding.

You’ll get: a policy-mapping workflow, evidence protocols, loss quantification models for Property, Business Interruption (BI), and Extra Expense, a ready-made dossier structure, adjuster briefing materials, regulator/relief linkages, and KPI-driven governance. Use this to move from “we’re assessing” to “approved and paid.”

1) Claims Strategy in the RISE-360™ Model

-

R — Readiness: Know your coverages (property, BI/EE, cargo, cyber, parametric). Maintain asset registers; validate backup/restore; pre-appoint evidence officers.

-

I — Impact & Insurance (0–72h): Triage safety first, then announce early: notify carriers, open claim numbers, request inspection windows, begin chain-of-custody evidence capture.

-

S — Stabilization (Days 3–30): Convert raw evidence into structured schedules, validate quantum, reconcile to policies, and push for advances tied to documented milestones.

-

E — Elevation (31–90+): Finalize settlements; memorialize lessons; update endorsements; tune the operating model and hardening CAPEX with proceeds.

Principle: A good claim is project managed like any restoration workstream: roles, timelines, trackers, and status cadences.

2) Policy Mapping: Know What You’re Claiming, and Why

2.1 Coverage Inventory (make this table before storm season)

| Policy Type | Insurer | Policy # | Period | Limits/Sub-limits | Deductibles/Waiting Periods | Key Endorsements | Exclusions |

|---|---|---|---|---|---|---|---|

| Property/All Risks | Flood/Storm Surge, Debris Removal | Wear/tear, Gradual damage | |||||

| Business Interruption (BI/EE) | Waiting: X hrs/days | Denial of Access, Utilities Interruption | No gross profit? | ||||

| Cargo/Inland Transit | |||||||

| Cyber (incl. outage costs) | |||||||

| Parametric (wind/rain index) | Trigger: [spec] | Payout grid | Use of proceeds |

Actions:

-

Pull policies & endorsements (PDFs) into 01_Policies_and_Endorsements/.

-

Abstract coverage into the table above; highlight deductibles, sub-limits, waiting periods, and evidence requirements.

-

Pre-build a coverage-to-evidence map (e.g., “Debris Removal → photos + vendor invoices + scope + GPS pins”).

2.2 Trigger & Waiting-Period Diagnostics

-

Record exact event date/time per site; document access restrictions (police orders, road closures).

-

For BI, set the waiting period clock (e.g., 72 hours) with a transparent timeline binder (authority notices, utility outages, photos).

2.3 Force Majeure & Contracts

-

Log landlord, supplier, and customer contract clauses. Some sub-limits may cover denial of access or utility service interruption; ensure you can prove the trigger with official notices.

3) Evidence Protocols: Capture Once, Use Many Times

3.1 The Five Golden Rules

-

Timestamp + geotag every file.

-

Photograph wide + medium + close and serial numbers.

-

Chain of custody: who captured, on what device, when, and where stored.

-

Separate Property vs BI/Extra Expense.

-

Index evidence to coverage items.

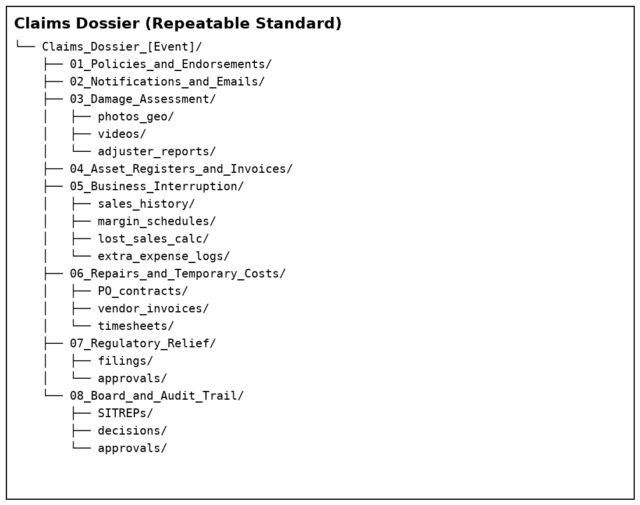

3.2 Folder Structure (repeatable standard)

3.3 Photo Naming Convention

[Site]_[Asset/Area]_[YYYYMMDD-HHMM]_[Initials]_[WIDE/CLOSE/SERIAL].jpg

3.4 Evidence Ownership

-

Evidence Officer: runs the index, trains capturers, validates metadata.

-

Site Leads: ensure completeness by area/asset list.

-

Tech Lead: ensures offsite/backed-up repository; controls access and versioning.

4) Property Damage (PD) Quantification

4.1 Assess & Categorize

-

Structural: roofs, walls, glazing, drainage.

-

Mechanical/Electrical: generators, switchgear, HVAC, pumps.

-

IT/Comms: servers, networking, end-user devices.

-

Stock: raw materials, WIP, finished goods (with SKU-level counts).

4.2 The Schedule of Loss (PD)

Columns to maintain:

-

Asset ID / Description

-

Serial # / Make/Model

-

Location (GPS / Site)

-

Pre-loss condition / last service date

-

Damage description (with photo refs)

-

Repair vs Replace decision basis

-

Vendor quotes (attach PDFs)

-

Lead time/ETA, SLA

-

Cost (parts + labour)

-

Linked evidence files (path/filename)

Tip: If stock is water-damaged, photograph count-and-disposal. Keep disposal permits/receipts.

4.3 Debris Removal & Mitigation

-

Separate line items; tie to mitigation steps (tarps, pumping, temporary bracing).

-

Document before/after photos and work logs (timesheets) to justify Extra Expense.

5) Business Interruption (BI) & Extra Expense (EE)

5.1 Define BI Basis

-

If BI is on Gross Profit (contribution) basis, align to policy definition.

-

Lost gross profit = (Baseline Sales − Actual Sales) × Baseline Gross Margin %

-

Indemnity Period and Waiting Period (e.g., first 72h non-indemnified).

5.2 Sales Baseline Construction

-

Use comparable periods (same weeks last year) adjusted for growth/seasonality.

-

Exclude unrelated anomalies; include documented customer cancellations.

-

Store in 05_Business_Interruption/sales_history/.

5.3 Margin Schedules

-

Build contribution margin by SKU/segment, pre-event.

-

Store cost evidence (BOMs, historical COGS). Put in margin_schedules/.

5.4 Extra Expense (EE)

-

Definition: reasonable costs to reduce BI (e.g., generators, temp premises, expedited freight).

-

Rule: EE is indemnified to the extent it reduces BI (or up to a sub-limit).

-

Keep P.O., invoice, proof of payment, and narrative linking the expense to reduced downtime.

5.5 BI Calculation Workbook (tabs)

-

Inputs: policy parameters (waiting period, limits).

-

Baseline Sales: weekly expected by channel/SKU.

-

Actual Sales: weekly actual (attach ledgers).

-

Gross Margin %: by SKU/segment.

-

Lost Gross Profit: automated calc.

-

Extra Expense: itemized, with link to evidence.

-

Offsets: credits, grants (if policy requires).

-

Result vs Limits/Sub-limits.

6) Notifications, Adjusters & Inspection Windows

6.1 Notification Pack (send within 24 hours where possible)

-

Policy numbers, sites affected, short impact narrative, contact tree, preferred inspection dates, evidence repository link (read-only).

-

Ask for advance payment criteria and documentation checklist.

Email subject: Claim Notice — [Company] — [Event] — [Policy #s]

6.2 Adjuster Brief (1–2 pages + annex)

-

Executive summary (people/sites/systems), photos overview, initial PD schedule, BI status, mitigation actions, site access requirements, H&S rules (PPE).

-

Provide site maps with damage hotspots and QR codes to evidence folders.

6.3 Field Logistics

-

Reserve time with site leads and vendors; ensure power/lighting or mobile generators for inspections.

-

Prepare sample restore tests (e.g., switchgear, servers) to demonstrate mitigation.

7) Advances & Settlement Strategy

7.1 Advance Triggers

-

Clean PD schedule for high-certainty items (e.g., roof panels, generators).

-

EE already incurred (with invoices/receipts).

-

BI advance based on early-week run-rate and credible baseline.

7.2 Negotiation Basics

-

Propose milestone-based advances: (i) acceptance of PD schedule; (ii) completion of critical repairs; (iii) BI period confirmation.

-

Offer transparency: weekly SITREPs, work photos, vendor SLAs.

7.3 Settlement Hygiene

-

Keep a reconciliation workbook: advances received vs. components (PD/BI/EE).

-

Track sub-limit utilization and deductible application.

8) Regulatory & Relief Linkages (Documentation Mindset)

Even where specific programs vary, the documentation standard is similar: traceable evidence, clear need, and proper approvals. Maintain a Relief Tracker with:

-

Program name, eligibility, requirements

-

Filing dates, forms, supporting evidence

-

Approvals, amounts, conditions

-

Conflicts/offsets with insurance (if any)

Attach official government/utility notices to show denial-of-access or outage durations.

9) Legal Considerations & Dispute Prevention

-

Notice windows & cooperation clauses: meet deadlines; provide reasonable access.

-

Mitigation duty: document all efforts to reduce loss; this protects BI/EE.

-

Preservation of damaged property: don’t discard without photographic inventory and, where required, adjuster consent.

-

Expert opinions: bring engineers or quantity surveyors where causation/costs could be debated.

-

Without-prejudice labeling for settlement discussions (jurisdiction dependent).

10) Governance, KPIs & Cadence

10.1 Roles

-

Legal/Claims Lead (owner)

-

Evidence Officer

-

Finance Lead (BI/EE quant)

-

Operations Lead (PD & repairs)

-

Comms Lead (stakeholders)

10.2 Weekly KPIs (first 8 weeks)

-

% Assets documented (PD schedule completeness)

-

# Insurer refs received (claim #s, adjuster assigned)

-

Advance $ requested vs received

-

BI model status (baseline built, actuals loaded)

-

Evidence integrity (files with timestamp/geo, % cross-referenced)

-

Open items with insurer (count, age)

10.3 Cadence

-

Daily (first 10 days): evidence & inspection status huddle (15 min).

-

Weekly: insurer/adjuster call with action tracker.

-

Board pack: short dashboard + top risks/asks.

11) Sector Mini-Playbooks (Claims & Relief Nuances)

Retail:

-

Refrigeration loss (stock write-offs) needs temperature logs if available.

-

BI: footfall collapse; offset with click-and-collect recovery evidence.

Manufacturing:

-

Machinery repair vs replace analysis; OEE evidence; WIP spoilage photos and counts.

-

BI: constraint on critical line → show capacity/throughput loss.

Hospitality:

-

Room inventory status, reservation cancellations, RevPAR baseline vs actual.

-

EE: temp power/water for habitability; staff housing.

Financial Services:

-

Denial-of-access for branches; ATM/network outage logs; remote KYC protocols.

-

BI: fee income shortfalls; digital substitution evidence.

12) Common Pitfalls (and How to Avoid Them)

-

Late notice: diary renewal and notice requirements in your calendar.

-

Unverifiable photos: no timestamps/serials → add metadata and retake key items.

-

Mixing PD and BI: keep ledgers and evidence separate; link via references.

-

Optimistic BI: validate baseline; document why certain weeks are representative.

-

Discarding damaged stock too soon: photograph, count, document disposal.

-

Silence with insurers: send structured updates weekly; always propose next steps.

13) Templates (Copy-Ready)

13.1 Claim Notification Email

Subject: Claim Notice — [Company] — [Event] — [Policy #s]

Dear [Insurer/Adjuster],

We notify a claim under the above policy(ies) due to [event] on [date/time] impacting [sites].

-

Contact: [name, phone, email]

-

Inspection windows: [options]

-

Evidence repository (read-only): [link]

-

Initial SITREP attached; PD and BI schedules in progress.

Please confirm claim numbers, adjuster assignment, and any specific documentation you require for an advance.

Regards, [name]

13.2 Adjuster Brief (Outline)

-

Company & event summary

-

People/Sites/Systems status

-

Safety controls for visit (PPE, escorts)

-

Top 10 PD items with photo refs

-

BI: baseline approach, current run-rate

-

Mitigation actions and EE to date

-

Site map + QR links to evidence folders

13.3 PD Schedule (CSV Columns)

13.4 BI Workbook (Tab Headers)

-

Parameters (limits, deductibles, waiting period)

-

Baseline_Sales (by week, channel/SKU)

-

Actual_Sales

-

Gross_Margin%

-

Lost_GP

-

Extra_Expense

-

Offsets

-

Summary_vs_Limits

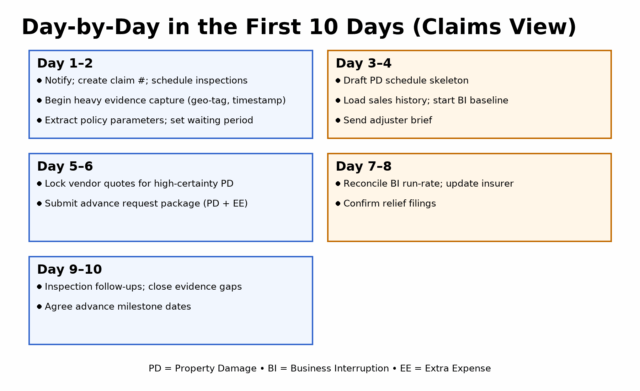

14) Day-by-Day in the First 10 Days (Claims View)

Day 1–2: Notify; create claim #; schedule inspections; begin heavy evidence capture; extract policy parameters; set waiting period.

Day 3–4: Draft PD schedule skeleton; load sales history; start BI baseline; send adjuster brief.

Day 5–6: Lock vendor quotes for high-certainty PD; submit advance request package (PD + EE).

Day 7–8: Reconcile BI run-rate; update insurer; confirm relief filings.

Day 9–10: Inspection follow-ups; close evidence gaps; agree advance milestone dates.

15) Closeout & Learning (Elevation)

-

Settlement reconciliation workbook completed; advances netted; sub-limits exhausted documented.

-

Endorsement updates: adjust sums insured, add parametric cover or utilities/denial-of-access.

-

Train & drill: repeat evidence and BI modeling exercises; update SOPs and role cards.

Next Step!

A fast, full claim is not luck—it’s discipline. When your dossier is clean, quantified, and linked to policy triggers, adjusters can recommend payment and relief agencies can approve support with confidence. Align your insurance and relief workflow to Dawgen RISE-360™, and your restoration budget will arrive when it matters most.

Let’s restore—and rise—together.

Dawgen Global’s RISE-360™ team builds bulletproof claim and relief dossiers, manages adjuster interactions, and accelerates advances so you can stabilize operations.

Request a proposal: [email protected]

USA: 855-354-2447

Web: https://dawgen.global

At Dawgen Global, we help you make Smarter and More Effective Decisions.

About Dawgen Global

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

✉️ Email: [email protected] 🌐 Visit: Dawgen Global Website

📞 📱 WhatsApp Global Number : +1 555-795-9071

📞 Caribbean Office: +1876-6655926 / 876-9293670/876-9265210 📲 WhatsApp Global: +1 5557959071

📞 USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements