Building Value-Chain Cost Advantage for Caribbean Organisations in a High-Pressure Economy

Executive Summary

Cost reduction has become a strategic necessity—not because organisations want to “cut back,” but because the economic environment is forcing a new level of discipline. Across the Caribbean and beyond, businesses are confronting persistent input cost inflation, logistics volatility, energy pressures, FX impacts, and higher financing costs. In response, many firms default to blunt measures: hiring freezes, delayed maintenance, training cuts, and across-the-board budget reductions. These actions may deliver short-term relief, but they often weaken capability, erode service, and create hidden costs that resurface later.

A more durable approach is value-chain cost reduction: reducing cost across the end-to-end chain—Source → Operate → Deliver → Sell/Service → Support—while protecting the value customers experience and strengthening operational resilience. In other words: value-protected cost advantage, not “budget cuts.”

This article explains:

-

Why cost pressure in the Caribbean has unique structural features (import dependence, energy costs, logistics constraints, FX volatility, skills scarcity)

-

How a value-chain lens reveals savings opportunities that budgets cannot

-

What “value-protected” cost reduction means in practice

-

The difference between quick wins and structural reshape—and why you need both

-

How organisations can launch a high-confidence opportunity scan using the Dawgen V.A.L.U.E.-Chain Cost Advantage Framework™

If cost advantage determines tomorrow’s winners, then leaders must move beyond budgets and start redesigning the cost drivers embedded in how the business operates.

Why “Budget Cuts” Don’t Create Cost Advantage

Budget cuts are familiar, fast, and deceptively simple. Finance teams reduce budgets, leaders ask functions to “find savings,” and spending is constrained. The problem is that budgets are not the same as cost drivers.

Budget cuts typically create one or more of these outcomes:

-

Service degradation (slower delivery, less support, poorer responsiveness)

-

Operational fragility (deferred maintenance, increased downtime, quality issues)

-

Risk exposure (cyber controls weakened, compliance gaps, control failures)

-

Savings evaporation (spend returns through different accounts, off-contract purchasing, or overtime creep)

-

Low morale and talent loss (skills drain, lower productivity, more turnover)

In contrast, cost advantage comes from changing the system:

-

simplifying complexity that creates inefficiency

-

improving planning and control so “urgent spend” decreases

-

redesigning processes and service models to match what customers truly value

-

reducing leakage through governance and controls

-

rethinking the operating model to remove duplication and slow decision-making

That’s why the modern cost conversation must move beyond budgets into the value chain.

The Caribbean Reality: Why Cost Pressure Is Structurally Different

Cost pressure exists globally, but the Caribbean faces certain structural features that intensify the problem—and shape the solution.

1) Import dependence and supply chain concentration

Many Caribbean businesses are heavily dependent on imported inputs—materials, parts, finished goods, equipment, packaging, and even certain labour categories. This creates exposure to:

-

supplier pricing in foreign currencies

-

shipping variability and container availability

-

port congestion and inland logistics friction

-

longer lead times and higher safety stock requirements

2) Foreign exchange and funding constraints

FX volatility can convert “stable” unit costs into moving targets. Additionally, higher interest rates and tighter credit conditions can make:

-

inventory more expensive to hold

-

receivables more painful to finance

-

capex decisions more constrained

-

unprofitable customers more dangerous

3) Energy and utility costs

In many sectors, energy is not a minor overhead—it is a material driver of cost competitiveness. Without disciplined energy management, organisations can pay for inefficiency every hour.

4) Scale disadvantages and complexity overload

Smaller markets often mean:

-

smaller purchasing volumes (less supplier leverage)

-

fewer distribution efficiencies

-

higher per-unit overhead

-

pressure to serve many customer segments with limited scale

This often leads to “complexity creep”:

-

too many SKUs

-

too many service exceptions

-

too many suppliers

-

too many manual processes

-

too many approvals and workaround steps

5) Skills scarcity and productivity constraints

Talent shortages increase labour costs and make productivity improvement harder—especially where processes are informal and measurement is weak.

Bottom line: Caribbean organisations need cost programmes that are realistic, data-informed, and value-protected—not generic “cost cutting.”

Why the Value Chain Lens Changes Everything

Budgets show who spends money. The value chain shows why money is spent—and where it multiplies.

A value-chain approach looks across five connected zones:

1) Source (Procurement and Inbound)

This is where cost often begins:

-

supplier pricing and terms

-

specifications and quality standards

-

import freight, duties, and Incoterms choices

-

supplier performance and reliability

-

demand aggregation and purchasing discipline

A common insight: what you buy is as important as what you pay.

Specification choices and fragmented buying often create more cost than price.

2) Operate (Operations / Service Delivery)

Here cost is created through:

-

labour productivity

-

asset utilisation

-

downtime and maintenance performance

-

yield and scrap

-

rework and quality failures

-

energy consumption and process efficiency

Operational leakage is often invisible in budgets because it is embedded in “normal activity.”

3) Deliver (Logistics and Inventory)

This includes:

-

warehouse layout and picking efficiency

-

routing and delivery frequency

-

fleet utilisation and fuel management

-

inventory policies (safety stock rules, reorder logic)

-

emergency freight and stockout costs

Logistics cost is often a function of service model design, not just transport rates.

4) Sell/Service (Commercial Economics)

Cost is shaped by:

-

discounting and trade spend

-

returns and credit notes

-

customer service expectations and exception handling

-

order patterns and minimum economic order sizes

-

channel complexity and service-level design

Many firms discover they have “high revenue customers” that are loss-making when cost-to-serve is included.

5) Support (SG&A and Technology)

SG&A becomes a cost advantage lever when approached as:

-

spans and layers redesign

-

shared services and standardisation

-

process automation and controls

-

technology rationalisation (tool sprawl reduction)

-

governance simplification and faster decision-making

When these zones are assessed together, the cost programme becomes an integrated transformation—not isolated cuts.

What “Value-Protected Cost Reduction” Means

Value-protected cost reduction means:

-

savings do not come from weakening service reliability

-

savings do not come from removing controls and increasing risk

-

savings are designed to reduce waste, complexity, and leakage while maintaining the customer promise

It also means explicitly balancing three priorities:

-

Cost (margin improvement and cash release)

-

Value (customer experience and proposition)

-

Resilience (risk controls and operational continuity)

This is exactly what the Dawgen V.A.L.U.E.-Chain Cost Advantage Framework™ is built to do.

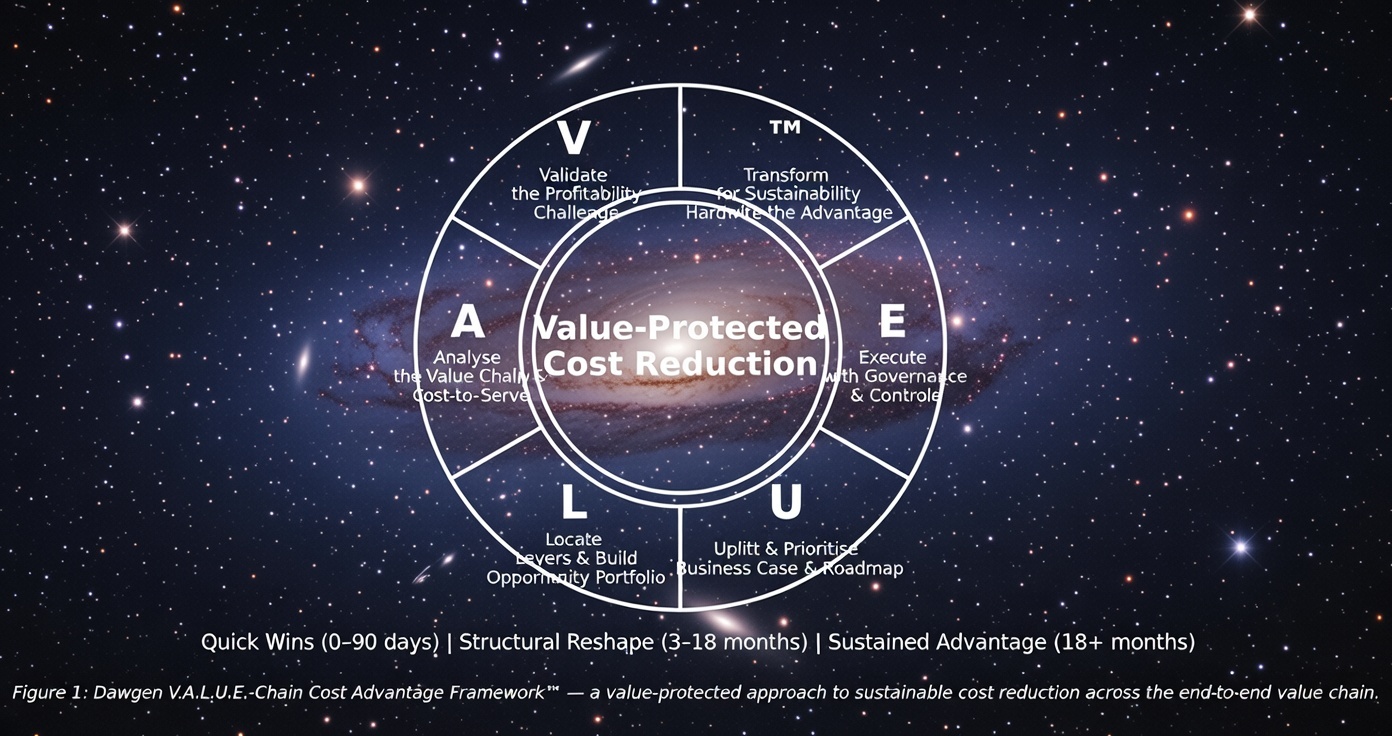

How V.A.L.U.E.™ Applies to Value-Chain Cost Reduction

The framework provides a structured path from diagnosis to results:

V — Validate the Profitability Challenge

-

build a margin bridge

-

identify the major cost pools and drivers

-

isolate leakage and complexity signals

-

establish a shared fact base and ambition

A — Analyse the Value Chain and Cost-to-Serve

-

map cost across Source, Operate, Deliver, Sell/Service, Support

-

perform cost-to-serve views where data allows

-

identify hotspots, constraints, and root causes

L — Locate Levers and Build the Opportunity Portfolio

-

generate levers in each zone

-

quantify ranges (low/base/high) and dependencies

-

assign owners and feasibility ratings

U — Uplift and Prioritise (Business Case + Roadmap)

-

prioritise using impact, speed, risk, value impact, and capability needs

-

separate quick wins from structural reshape

-

build a sequenced roadmap

E — Execute with Governance and Controls

-

run workstreams with cadence

-

track savings (gross → net → run-rate)

-

enforce compliance and decision rights

-

prevent savings evaporation

™ — Transform for Sustainability

-

embed controls, KPIs, and accountability

-

implement supplier performance management

-

create continuous improvement pipeline

-

prevent complexity creep

A Practical Value-Chain Opportunity Scan (What to Review First)

If you want a practical starting point, here is the highest-yield scan order for many organisations:

Source (Procurement) – 10 questions

-

Are we buying on contract, and what is the compliance rate?

-

Do specifications match what customers truly value—or are we over-engineering?

-

Are supplier terms optimised (payment terms, rebates, Incoterms)?

-

Are we consolidating volume or fragmenting purchasing?

-

Are we paying “urgency premiums” because of poor planning?

Operate (Operations) – 10 questions

-

What is our downtime cost, and what causes it?

-

What is our yield loss and rework cost?

-

Where is labour underutilised or mis-scheduled?

-

Are we measuring energy consumption by process and shift?

-

Are quality failures generating hidden logistics and service costs?

Deliver (Logistics) – 8 questions

-

Is delivery frequency aligned with profitability?

-

Are routes optimised or built around habit?

-

Are warehouse processes measured and improved?

-

Is inventory policy tuned to demand variability and lead times?

-

How much cost comes from stockouts, emergency freight, and overstock?

Sell/Service (Commercial) – 8 questions

-

Which customers/products/channels are unprofitable after cost-to-serve?

-

Are returns and credit notes controlled and analysed?

-

Do service-level agreements match pricing?

-

Are discounts funding inefficiency rather than strategy?

Support (SG&A/Tech) – 8 questions

-

Where is work duplicated across functions?

-

Are approvals excessive and creating delays?

-

Which processes are manual that should be automated?

-

Is technology sprawl increasing cost and reducing discipline?

-

Are control weaknesses creating leakage (e.g., purchasing, inventory, payroll)?

This scan is often enough to build a credible opportunity heatmap within weeks.

Case Snapshot: What Value-Chain Cost Advantage Can Look Like

A regional organisation launched a value-chain programme after margin pressure increased and financing costs rose.

Quick wins (0–90 days):

-

contract compliance enforcement, reduction in maverick spend

-

overtime and scheduling discipline

-

claims/returns controls to reduce leakage

-

inventory rationalisation and improved replenishment rules

Structural reshape (3–18 months):

-

strategic sourcing and specification rationalisation

-

energy optimisation and downtime reduction

-

delivery frequency redesign by customer segment

-

SG&A redesign supported by automation and simplified workflows

Sustainment (18+ months):

-

Value Capture Office governance cadence

-

supplier scorecards and performance management

-

periodic complexity reviews to prevent re-expansion

The result was not only lower cost but improved service consistency and stronger cash generation—creating space to invest in technology and customer experience.

Cost Advantage Is Built Across the Chain

Cost reduction programmes that focus on budgets tend to produce temporary relief and long-term fragility. In contrast, cost advantage is built when leaders:

-

diagnose cost drivers across the value chain

-

protect customer value and resilience

-

execute a two-speed programme (quick wins + structural reshape)

-

lock in benefits with governance, controls, and continuous discipline

That is why Dawgen Global’s approach is value-chain based and value-protected.

Next Step!

Ready to uncover value-protected cost reduction across your value chain?

Email [email protected] with the subject line “V.A.L.U.E. – Cost Opportunity Scan” to request an initial discussion and our data intake checklist.

WhatsApp Global: +1 555 795 9071 | Contact form: https://www.dawgen.global/contact-us/

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

Email: [email protected]

Email: [email protected]  Visit: Dawgen Global Website

Visit: Dawgen Global Website

WhatsApp Global Number : +1 555-795-9071

WhatsApp Global Number : +1 555-795-9071

Caribbean Office: +1876-6655926 / 876-9293670/876-9265210  WhatsApp Global: +1 5557959071

WhatsApp Global: +1 5557959071

USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements