| Executive Summary

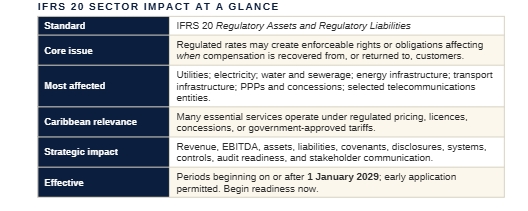

IFRS 20, Regulatory Assets and Regulatory Liabilities, will have its greatest impact on companies operating under rate-regulated frameworks — entities whose prices, tariffs, fees, or charges are determined, approved, or influenced by a regulator through enforceable regulatory agreements. The sectors most likely to be affected include utilities, electricity providers, water and sewerage entities, energy and power infrastructure companies, gas transmission operators, transport infrastructure operators, airports, seaports, toll roads, rail systems, public-private partnership (PPP) entities, concession operators, and selected telecommunications companies. For Caribbean economies the implications are particularly important, because many essential services operate under some form of regulated pricing, licence arrangement, concession framework, or government-approved tariff. IFRS 20 may therefore affect not only accounting and financial reporting, but also board reporting, tariff discussions, debt financing, investor communication, audit readiness, and regulatory engagement. The standard is effective for annual reporting periods beginning on or after 1 January 2029, with earlier application permitted — but affected entities should begin readiness assessments now. This article examines the sectors most exposed, why they are exposed, the specific issues to assess, and how Dawgen Global can support regulated entities across the Caribbean and beyond. |

1 Why Sector Exposure Matters

IFRS 20 is not expected to affect every company. Its impact is concentrated in industries where companies operate under regulatory agreements that determine how much they can charge customers and when they can recover approved compensation.

That makes sector analysis essential. A retailer, manufacturer, hotel, or professional-services firm that freely negotiates prices is unlikely to be affected. An electricity utility, water company, airport operator, seaport concessionaire, toll-road operator, or regulated energy-infrastructure business may face significant financial reporting implications.

The key question is not simply whether a company is regulated in a general legal sense. The more precise question is whether the company is party to a regulatory agreement that creates enforceable rights or obligations affecting regulated rates, and that creates differences in timing between when regulatory goods or services are supplied and when compensation is charged to, or deducted from, customers through those rates.

Where that difference in timing exists, IFRS 20 may require recognition of regulatory assets, regulatory liabilities, regulatory income, and regulatory expense. Identifying sector exposure is the first step in IFRS 20 readiness.

2 The Core Trigger: Rate Regulation and Differences in Timing

IFRS 20 applies where a regulatory agreement gives rise to regulatory assets and regulatory liabilities, because the framework determines how a company is compensated for regulated goods or services. The central concept is the difference in timing.

A regulatory asset may arise when a company supplies regulated goods or services in the current period but is entitled to recover part of the compensation through regulated rates in a future period. A regulatory liability may arise when a company charges customers in the current period for amounts relating to another period, or must reduce future rates because it has already recovered more than it is entitled to retain. IFRS 20 is therefore especially relevant where tariffs are set using cost-recovery, permitted-return, performance-incentive, penalty, pass-through, or true-up mechanisms.

COMMON MECHANISMS THAT MAY CREATE IFRS 20 EXPOSURE

| • Fuel cost recovery mechanisms

• Storm or disaster recovery surcharges • Infrastructure and approved capital expenditure recovery • Pension cost recovery • Performance incentives and penalties |

• Over-recovery and under-recovery adjustments

• Tariff stabilisation arrangements • Price-control mechanisms • Regulatory depreciation and return on regulatory capital base • Future rate reductions linked to current over-collections |

Companies in regulated sectors should assess not only whether they are regulated, but how their regulatory framework determines compensation over time.

3 Utilities: The Sector Most Clearly Exposed

Utilities are likely to be among the most affected sectors. Electricity, water, sewerage, and waste-management entities often operate under frameworks that determine how and when they recover approved costs from customers.

Electricity Utilities

Electricity utilities may face IFRS 20 implications across generation, transmission, distribution, and supply. Frameworks may allow recovery of costs related to fuel, grid maintenance, network expansion, renewable integration, storm restoration, asset replacement, and reliability improvement. A distributor that incurs heavy restoration costs after a hurricane may need to assess whether a regulatory asset exists if recovery is permitted through future tariffs; conversely, over-recovery of fuel costs when prices fall below tariff assumptions may create a regulatory liability through future tariff reductions.

ELECTRICITY UTILITIES SHOULD ASSESS

| • Fuel pass-through mechanisms

• Purchased-power adjustment clauses • Storm recovery mechanisms • Grid modernisation costs • Renewable integration costs |

• Regulatory depreciation

• Approved return on capital base • Tariff true-up arrangements • Customer rebate obligations • Performance incentives and penalties |

Water and Sewerage Utilities

Water and sewerage entities are capital-intensive and often rely on regulated tariffs to recover infrastructure costs over long periods. IFRS 20 may be relevant where frameworks permit recovery of costs related to water-treatment infrastructure, pipe-network replacement, non-revenue-water reduction, desalination, wastewater treatment, sewerage upgrades, drought-response and climate-resilience investments, pension obligations, and approved operating-cost variances.

Waste Management and Environmental Utilities

In some jurisdictions, waste-management, recycling, landfill, or environmental-service providers also operate under regulated pricing. Where charges are set or approved by regulators and timing differences arise, IFRS 20 may require further analysis.

4 Energy and Power Infrastructure

Energy-infrastructure entities — power-transmission companies, grid operators, renewable-energy infrastructure entities, gas pipelines, storage facilities, and other regulated energy networks — are another high-impact group, typically involving large upfront capital, long recovery periods, and regulated returns.

Renewable Energy and Grid Transition

The transition to renewable energy creates major investment needs: grid upgrades, battery storage, renewable integration, transmission expansion, and resilience projects may be financed through regulated rates. Where agreements allow recovery over future periods, IFRS 20 may affect the timing of reported income and the recognition of regulatory assets or liabilities — particularly relevant in the Caribbean, where renewable energy, energy security, and climate resilience are strategic priorities.

Fuel and Energy Cost Volatility

Energy companies often operate under mechanisms that adjust tariffs for changes in fuel or purchased-energy costs. Where actual costs differ from tariff assumptions, the difference may be recovered from or returned to customers in future periods — a classic IFRS 20 issue.

COMPANIES SHOULD CAREFULLY ASSESS

| • Fuel adjustment clauses

• Purchased-power cost pass-through • Energy cost true-ups • Grid reliability incentives |

• Regulatory capital base calculations

• Return on assets not yet in use • Regulatory interest on deferred balances |

5 Transportation Infrastructure

Transportation infrastructure may be materially affected, especially where operators charge regulated fees, tolls, tariffs, or user charges.

Airports

Airport operators may be subject to frameworks governing passenger charges, landing fees, security charges, terminal fees, or infrastructure-recovery charges. IFRS 20 may be relevant where operators recover approved costs or investments through future charges — runway expansions, terminal upgrades, safety and security investments, climate-resilience works, or pandemic-related revenue shortfalls. Areas to review include passenger-fee regulation, landing and parking charges, regulated security fees, infrastructure-recovery mechanisms, concession arrangements, government-approved tariff frameworks, and under-/over-recovery mechanisms.

Seaports

Ports are critical Caribbean infrastructure. Many authorities or private operators work under tariff frameworks, concession agreements, or government-approved fee structures. IFRS 20 may be relevant where charges are regulated and the operator has enforceable rights to recover approved costs through future tariffs, or obligations to reduce future charges. Potentially relevant charges include cargo-handling tariffs, berthing fees, wharfage, container-handling fees, passenger-facility charges, security charges, and infrastructure-recovery fees.

Toll Roads and Rail Systems

Toll-road and rail operators may be affected where fees are regulated or subject to concession-based approval. Where operators recover construction, maintenance, or availability costs through regulated user charges, and are entitled to future increases or required to reduce future charges for current over-recovery, IFRS 20 may apply.

6 Public-Private Partnerships and Concession Arrangements

PPPs and concession arrangements require careful analysis because they often combine infrastructure service obligations, regulated pricing, government oversight, and long-term cost recovery. Not every arrangement falls within IFRS 20, however: some rights and obligations may be accounted for under other IFRS Standards. The entity must first assess the requirements applicable to service concessions, leases, financial instruments, and revenue; IFRS 20 may then apply to remaining rights and obligations that meet the definitions of regulatory assets or liabilities.

PPPs AND CONCESSION ENTITIES SHOULD REVIEW

| • Concession agreements

• Licence terms • Tariff-setting mechanisms • Government guarantee clauses • Minimum revenue support |

• Regulated user fees

• Availability payment mechanisms • Cost recovery provisions • Capital expenditure approval processes • Future price adjustment clauses |

The interaction between IFRS 20 and concession accounting can be complex. This is an area where professional judgement, technical accounting analysis, and early auditor engagement will be essential.

7 Telecommunications and Digital Infrastructure

Telecommunications is not automatically within scope. Many telecom companies operate in competitive markets even when subject to sector regulation. IFRS 20 becomes relevant only where an entity is subject to enforceable rate-setting mechanisms that create regulatory assets or liabilities — for example: regulated interconnection charges, universal-service obligations, tariff-approval mechanisms, wholesale-access pricing, regulated broadband-infrastructure charges, spectrum-related pricing, and cost-recovery arrangements for mandated services.

Telecom companies should distinguish between general sector regulation and rate regulation that creates enforceable rights or obligations affecting future rates. Digital-infrastructure companies — fibre-network operators or regulated broadband providers — may also need to assess IFRS 20 where pricing is regulated and cost recovery occurs over future periods.

8 Public-Sector Commercial Entities

Public-sector commercial entities may also be affected, particularly where they prepare IFRS financial statements and operate under government-approved pricing or tariff frameworks — public utilities, port and airport authorities, water commissions, electricity providers, transport and road authorities, state-owned infrastructure companies, and public-sector PPP vehicles.

For these entities, IFRS 20 may affect financial statements used for bond financing, development-bank lending, government reporting, public accountability, tariff applications, investor presentations, privatisation or concession planning, and credit-rating assessments. Because tariffs are often politically and socially sensitive, clear communication of IFRS 20 effects will be especially important.

9 Caribbean-Specific Sector Implications

The Caribbean has a high concentration of essential-service entities operating under regulated or quasi-regulated pricing. IFRS 20 should therefore be on the radar of boards, CFOs, audit committees, regulators, and policymakers across the region.

Climate and Disaster Recovery

Caribbean utilities and infrastructure operators face recurring exposure to hurricanes, flooding, and other climate shocks. Where regulators permit disaster-recovery costs to be recovered through future tariffs — hurricane restoration, flood-damage repairs, grid rebuilding, emergency water infrastructure, airport and port recovery, and climate-resilience capital projects — IFRS 20 may affect the recognition of regulatory assets.

Energy Transition

Many Caribbean jurisdictions are pursuing renewable energy and reduced dependence on imported fuel. The transition requires capital investment in solar, wind, storage, grid upgrades, and resilience. Where recovered through regulated rates, IFRS 20 may become relevant.

Infrastructure Financing

Caribbean infrastructure projects often rely on long-term financing from banks, bond markets, multilateral institutions, development-finance institutions, or PPP investors. IFRS 20 may affect reported performance, leverage, EBITDA, working capital, and debt covenants. Lenders and investors will need to understand how IFRS 20 changes reported numbers without necessarily changing the underlying cash economics.

Tariff Affordability and Public Communication

In small island economies, tariffs for electricity, water, transport, and infrastructure are politically and socially sensitive. IFRS 20 may require companies to explain how current rates relate to past or future compensation, and how regulatory assets and liabilities affect future tariffs — both a reporting challenge and a communication opportunity.

10 How to Determine Whether an Entity Is in Scope

A company should not assume it is within or outside IFRS 20 based on its industry alone. The assessment must rest on the specific regulatory agreement. A practical scoping assessment should ask:

- Does the company supply goods or services subject to regulated rates?

- Is there a regulator that determines, approves, or influences those rates?

- Are the relevant rights and obligations enforceable?

- Does the regulatory agreement determine the company’s compensation for regulated goods or services?

- Are there differences in timing between when goods or services are supplied and when compensation is included in customer rates?

- Does the company have rights to increase future rates because of current or past activities?

- Does the company have obligations to reduce future rates because of current or past recoveries?

- Are there performance incentives, penalties, cost pass-throughs, or true-up mechanisms?

- Are regulatory balances already tracked in regulatory filings but not recognised in the IFRS financial statements?

- Are systems capable of producing auditable information for IFRS 20 reporting?

The answers will help determine the likely impact and complexity of IFRS 20 implementation.

11 Key Risks for Affected Sectors

Six recurring risks tend to surface across regulated sectors. The earlier each is identified, the lower the cost of managing it.

| Risk | What it looks like in practice |

| Late identification | Discovering too late that IFRS 20 applies, creating pressure around transition data, audit evidence, disclosures, and stakeholder communication. |

| Data | Regulatory data exists but not in a form suitable for IFRS reporting; bridges are needed between regulatory filings, accounting systems, and reporting processes. |

| Judgement | Significant judgement over enforceability, identification of timing differences, measurement of future cash flows, and recovery or fulfilment patterns. |

| Systems | Existing systems may not capture regulatory asset and liability movements, regulatory interest, maturity analysis, and disclosures. |

| Covenant | Changes in reported revenue, EBITDA, assets, liabilities, and equity may affect debt covenants and financing discussions. |

| Communication | Users may misinterpret changes in reported performance if management does not clearly explain IFRS 20 effects. |

12 Sector Readiness Checklist

Use the following checklist to gauge readiness across six dimensions.

GOVERNANCE

- Has the board been briefed on IFRS 20, and has the audit committee received a technical overview?

- Has management assigned implementation responsibility and convened a cross-functional project team?

SCOPING

- Have all regulatory agreements, licences, concession agreements, tariff frameworks, and rate orders been identified and reviewed?

- Have enforceable rights and obligations been assessed, and in-scope activities documented?

ACCOUNTING

- Have potential regulatory assets and liabilities been identified, and recognition and measurement requirements assessed?

- Have regulatory income and expense impacts been estimated, and an accounting policy paper prepared?

SYSTEMS AND CONTROLS

- Can systems track timing differences and prepare reconciliations and maturity analyses?

- Are controls in place over estimates and judgements, and is regulatory data reconciled to financial reporting data?

FINANCIAL IMPACT

- Has the effect on revenue, EBITDA, assets, liabilities, and equity been estimated, and covenants and metrics reviewed?

- Have budgets and forecasts been updated, and investor and lender communication considered?

AUDIT READINESS

- Have auditors been engaged early, and are technical position papers and supporting evidence being prepared?

- Are disclosures being developed in advance?

13 How Dawgen Global Can Help

Dawgen Global supports regulated entities, boards, CFOs, audit committees, regulators, lenders, and investors in preparing for IFRS 20. Our services include:

- Sector-specific IFRS 20 scoping assessments.

- Review of regulatory agreements, licences, tariffs, and concession arrangements.

- Identification of regulatory assets and liabilities, and regulatory income and expense analysis.

- IFRS 20 financial statement impact assessments.

- Utilities, energy, transport, infrastructure, and PPP sector diagnostics.

- Systems and data readiness reviews, and accounting policy development.

- Covenant and KPI impact analysis.

- Board and audit-committee training.

- Audit preparedness documentation and IFRS disclosure design and review.

- Investor, lender, and regulator communication support.

We help clients understand not only whether IFRS 20 applies, but what it means for financial reporting, governance, systems, financing, and stakeholder confidence.

14 Conclusion: Affected Sectors Should Start Now

IFRS 20 will be most significant for companies whose business models depend on regulated pricing and long-term cost recovery. Utilities, energy infrastructure, transportation, PPPs, concession entities, public-sector commercial entities, and selected telecommunications businesses should begin assessing their exposure now.

The most important first step is not to calculate the final accounting numbers. It is to determine whether the company’s regulatory agreements create enforceable rights or obligations that give rise to regulatory assets or regulatory liabilities. For many affected entities, IFRS 20 will require new data, new controls, new disclosures, new board oversight, and new stakeholder communication. Those that start early will be better positioned to manage transition risk, educate users of financial statements, and communicate with clarity.

Dawgen Global is ready to assist regulated entities across the Caribbean and beyond with the full IFRS 20 readiness and implementation journey.

| Is your organisation in a sector affected by IFRS 20?

Dawgen Global can help you assess whether IFRS 20 applies, understand the financial reporting implications, prepare your systems, train your teams, and communicate the impact with confidence. Let’s have a conversation. Website: www.dawgen.global/contact-us Email: [email protected]

|

About Dawgen Global

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

Email: [email protected]

Email: [email protected]  Visit: Dawgen Global Website

Visit: Dawgen Global Website

WhatsApp Global Number : +1 555-795-9071

WhatsApp Global Number : +1 555-795-9071

Caribbean Office: +1876-6655926 / 876-9293670/876-9265210  WhatsApp Global: +1 5557959071

WhatsApp Global: +1 5557959071

USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements