Editor’s Note

This is the first article in a twelve-part Dawgen Global series introducing DAGAF™ — the Digital Asset Governance & Assurance Framework — the Caribbean’s first integrated framework for the governance, assurance, tax, and risk management of tokenized real-world assets. Each article in the series will engage one dimension of the tokenization question facing Caribbean enterprises and regulators in 2026 and beyond. The full DAGAF™ White Paper, on which this series is based, is available on request from Dawgen Global.

The Question No Caribbean Board Can Avoid Much Longer

There is a moment, increasingly common in Caribbean board meetings, when someone raises tokenization. It might be a younger executive who has been reading what BlackRock and JPMorgan are doing. It might be a strategy consultant making a presentation. It might be the chair, who has just returned from a regional fintech conference and wants to know what the firm’s position is.

The figures get cited: over US$340 billion in tokenized real-world assets globally in early 2026; Standard Chartered’s forecast of US$2 trillion by 2028; the EY research finding that 91 percent of high-net-worth investors and 83 percent of institutional investors plan to allocate to tokenized bonds by year-end; the BlackRock tokenized US Treasury fund; JPMorgan’s deposit token on a public blockchain; Citi Token Services’ 24/7 USD clearing for cross-border payments. The figures arrive together and they arrive with momentum.

Then there is a pause. Because the next questions — from the audit committee chair, from the senior independent director, from the general counsel, from the CFO — are the questions that have no comfortable answers in our region today. Under what regulatory framework? With what custody architecture? What is the tax position? What audit evidence will the external auditor accept? What does fiduciary duty actually require of us if we proceed? What does it require of us if we abstain? What happens if we make a decision and the regulatory framework subsequently moves against us?

The pause is honest. The pause is also, increasingly, indefensible. It is honest because the regulatory architecture in our region genuinely has not caught up with the global market. It is indefensible because the global market is no longer waiting for anyone to catch up. The capital is moving. The infrastructure is being rebuilt. The decisions are being made elsewhere. And Caribbean boards that continue to defer engagement are, whether they recognise it or not, taking a position — the position of strategic spectatorship — with consequences that compound over time.

This article is the first in a twelve-part series that argues, through evidence and structured analysis, that the Caribbean cannot sit this out. It introduces a framework — DAGAF™ — specifically built to give Caribbean boards, executives, audit committees, regulators, and policy makers a defensible methodology for engaging with tokenization on their own terms. And it sets up the argument that runs through the rest of the series: the question is no longer whether the Caribbean engages with tokenization, but how, when, and on what governance and assurance architecture.

| “The pause is honest. The pause is also, increasingly, indefensible.” | ||

| PART I

The Inflection Point: Why Tokenization Crossed the Line in 2026 |

||

The most important thing to understand about tokenization in 2026 is that the conversation has shifted. For most of the previous decade, tokenization was discussed alongside cryptocurrency — a speculative asset class with extreme volatility, regulatory ambiguity, and reputational risk. The institutional concern was largely about exclusion: how to keep crypto exposure off the balance sheet, off the audit, and off the front page. Most Caribbean boards quite reasonably concluded that the prudent posture was to wait.

That posture is no longer available. In April 2026, the International Monetary Fund published a note titled Tokenized Finance. Its central argument was that tokenization is not a marginal efficiency improvement to existing financial infrastructure. It is a structural reconfiguration of how trust, settlement, and risk are organised across the global financial system. The IMF’s framing matters because it tells regulators, central banks, asset managers, and corporate boards that this is not a question of whether to engage but of how, when, and on what terms. When the IMF reframes a market category from speculative to structural, supervisory dialogue follows.

The numerical evidence behind that reframing is dense. As of early 2026, on-chain real-world assets exceed US$340 billion in value. Tokenized US Treasury products form the largest single category. Private credit tokenization has grown faster in percentage terms. Institutional alternative funds, tokenized commodities, and corporate bonds round out the major categories. The number of asset holders crossed 700,000 in early 2026 — a figure that reflects institutional adoption rather than retail enthusiasm, given the minimum investment thresholds that govern most regulated tokenized products.

| US$340B+

On-chain real-world assets globally, early 2026 |

US$2T

Forecast tokenized assets by 2028 (Standard Chartered) |

91% / 83%

HNW / institutional investors planning tokenized bond allocations by year-end (EY) |

Standard Chartered, hardly a promotional source, forecasts US$2 trillion in tokenized assets by 2028. Standard Chartered’s CEO Bill Winters has said publicly that “pretty much all transactions will be tokenized” in the medium term. Morgan Stanley launched a dedicated tokenized fund in April 2026 targeting a US$500 billion valuation. EY research finds that 91 percent of high-net-worth investors and 83 percent of institutional investors plan to allocate to tokenized bonds by year-end 2026, with institutional portfolios expected to hold seven to nine percent in tokenized assets by 2027. These are not promotional projections. They are decisions already being made by asset managers, banks, and financial market infrastructures.

The infrastructure side of the market reinforces the point. DTCC has launched a tokenized real-time collateral management platform. Clearstream has launched its proprietary asset tokenization platform under European Union Central Securities Depositories Regulation (CSDR). Nasdaq has confirmed tokenized settlement of investor assets. JPMorgan has issued its USD deposit token on a public blockchain. Citi has integrated Citi Token Services with 24/7 USD clearing for cross-border payments. The financial market infrastructure is being rebuilt around tokenization, not around it.

Regulatory clarity has followed the institutional momentum. The United States passed the GENIUS Act in July 2025, establishing a federal stablecoin framework with 1:1 reserve requirements and monthly disclosures. The CLARITY Act — the Digital Asset Market Clarity Act — advanced through the House in 2025 and is targeted for Senate Banking Committee markup in 2026, drawing the line between digital commodities under the Commodity Futures Trading Commission and securities under the Securities and Exchange Commission. On 17 March 2026, the SEC and CFTC issued a joint interpretation naming sixteen crypto assets as digital commodities. In March 2026, the Federal Reserve, the Office of the Comptroller of the Currency, and the Federal Deposit Insurance Corporation jointly clarified that an eligible tokenized security receives the same regulatory capital treatment as its non-tokenized form. The European Union’s Markets in Crypto-Assets Regulation (MiCA) has been in full application since December 2024. The United Kingdom, Singapore, Hong Kong, the United Arab Emirates, Switzerland, and Japan have each established competitive licensing regimes.

These are the conditions of an inflection point. The market has scale. The market has institutional participation. The market has supervisory clarity in the major jurisdictions. The market has rebuilt infrastructure. And the market is no longer making the case for itself — it is being made for it, by the firms and the regulators that are already in motion.

| PART II

The Caribbean Position: What Sitting It Out Actually Looks Like |

The regional position is materially different from the global picture. Jamaica has no dedicated tokenization or virtual asset framework. Tokens are analysed case-by-case under the Securities Act, the Banking Services Act, and the Payment Clearing and Settlement Act. There is no published regulatory roadmap with a defined timeline for primary tokenization legislation. The Bank of Jamaica’s digital currency, JAM-DEX, three years on from its launch, faces persistently low merchant and consumer adoption — a cautionary tale about the gap between technical readiness and behavioural change. The Jamaica Stock Exchange flagged interest in cryptocurrency listings as far back as 2018 but has not built tokenized securities infrastructure in the seven years since.

The Eastern Caribbean Central Bank has been more deliberate. The ECCB has called for expedited issuance of Virtual Asset Business Regulations across the eight ECCU member territories. It has identified four specific priorities: the regulations themselves; the promotion of regional capital market alternatives to crypto products, including a relaunched DCash 2.0; the establishment of systems to identify virtual asset service providers operating in the region; and the constitution of an Eastern Caribbean Financial Standards Board. The ECCB’s posture has been deliberately cautious — informed by the lessons of FTX and other crypto failures — while recognising the structural opportunity. The framework is being built. The timetable, however, has not been published with precision.

Other CARICOM jurisdictions present distinct postures. Bermuda has a relatively mature Digital Asset Business Act framework administered by the Bermuda Monetary Authority. The Cayman Islands has its Virtual Asset (Service Providers) Act. The Bahamas, despite the reputational damage from the FTX collapse, retains its Digital Assets and Registered Exchanges Act. Barbados, Trinidad and Tobago, Belize, and Guyana operate primarily through existing securities, banking, and payments legislation, with varying levels of supervisory focus on virtual assets. The Caribbean does not present a unified regulatory front to global counterparties — it presents a patchwork of fifteen-plus territorial regimes at varying levels of development.

The Inter-American Development Bank has explicitly framed Latin America and the Caribbean as a tokenization “testing ground” driven by remittance corridors, cross-border payment needs, and financial inclusion imperatives. The IDB’s Tokenization and Development framework provides intellectual scaffolding for regional policy makers prepared to engage. Brazil, Mexico, and Colombia have advanced fintech frameworks. The Caribbean is not at the centre of this regional conversation — nor can it afford to be at the periphery.

This is what sitting it out looks like in practice. It does not look like a dramatic exit from the global financial system. It looks like a slow, quiet erosion of optionality. It looks like Caribbean asset managers losing institutional mandates because their custody architecture cannot support tokenized fund vehicles. It looks like Caribbean real estate developers watching diaspora capital go to fractionalised resort offerings in Dubai or Portugal because there is no defensible Jamaican equivalent. It looks like Caribbean credit unions watching member liquidity expectations evolve and finding that traditional share-redemption mechanics no longer match what younger members expect. It looks like Caribbean sovereign debt managers watching their non-resident investor base age and contract because the access mechanisms they offer are inferior to what other emerging markets now offer.

None of these are dramatic events. All of them are happening already, at the margins, in the conversations that do not make the front page. They compound. The compound rate determines whether the Caribbean enters the tokenized financial era as an active participant or as a price-taker.

| PART III

The Use Cases the Region Already Has |

The case for Caribbean engagement is not abstract. It rests on a specific set of asset classes that are textbook candidates for tokenization — not because tokenization is fashionable but because the structural characteristics of these assets and the structural characteristics of tokenization match unusually well. Five categories warrant explicit identification.

Real estate

Caribbean real estate — resort properties, commercial developments, residential complexes — has high asset values, fragmented ownership patterns, and significant non-resident investor interest. The classical problems of Caribbean real estate investment have been minimum ticket sizes, illiquid secondary markets, and the friction of cross-border legal structures. Tokenization addresses each of these directly. Fractionalisation of a US$60 million resort property into investor units of US$10,000 to US$50,000 broadens the addressable investor base by an order of magnitude. A regulated secondary market mechanism gives the property a liquidity profile no traditional Caribbean real estate vehicle has ever had. A documented legal structure, executed on a smart contract platform with appropriate custody, manages the cross-border friction that has historically deterred institutional capital. None of this is theoretical. The DAGAF™ White Paper sets out a complete illustrative scenario for a tokenized resort real estate offering.

Tourism receivables and advance-revenue instruments

The Caribbean’s tourism economies generate significant advance-revenue exposure: hotel bookings made and paid for months ahead of stay; airline-linked instruments; tour operator advance receipts; cruise-line port-call commitments. These cash flows are typically illiquid — the hotel cannot use the booking revenue until the guest arrives. Tokenization of receivables, properly structured, can convert tomorrow’s revenue into today’s working capital while maintaining a transparent, programmatic claim on the underlying obligation. This is not a Caribbean innovation — receivables tokenization is established in trade finance globally — but the Caribbean tourism economy is unusually well suited to it.

Sovereign debt and infrastructure financing

Caribbean sovereigns and statutory bodies issue debt at scale. The investor base for that debt is concentrated, the access mechanisms are conventional, and the secondary market liquidity is limited. Tokenized sovereign debt — particularly when linked to diaspora investment programmes, climate finance instruments, and blue-economy themes — can broaden investor access, programme distributions and disclosures, and create a secondary market accessible to a population the traditional bond market has never reached. The IDB has published work specifically on tokenization of development finance instruments. The international precedents — the World Bank’s bond-i, the European Investment Bank’s blockchain bond programme — are growing.

Credit union member shares and co-operative bonds

The Caribbean credit union movement holds a substantial share of regional savings, member capital, and small-business lending. The classical credit union member share has limitations the movement has long acknowledged: secondary transfer is restricted, member liquidity at withdrawal is constrained by capital adequacy requirements, and inter-credit-union capital flow is administratively heavy. Tokenization of member share records — with appropriate preservation of co-operative legal status, the Jamaican corporate income tax exemption on co-operative surplus under the Co-operative Societies Act, and member protections — offers the movement a path to operational modernisation and member-experience improvement that does not require abandoning the co-operative form. The DAGAF™ White Paper sets out a credit union illustrative scenario explicitly addressing these structural sensitivities.

Carbon credits and blue-economy assets

The Caribbean is at the front line of climate finance. Carbon credit issuance, mangrove and marine protection finance, blue-economy infrastructure — these are emerging asset classes for which the global market is hungry and for which the verification, attribution, and tracking requirements are unusually severe. Tokenization is one of the few infrastructure layers capable of delivering the transparency these instruments require at the scale international capital expects. The Caribbean opportunity here is not merely commercial; it is also reputational and developmental.

| “These are not Caribbean tokenization opportunities because tokenization is fashionable. They are tokenization opportunities because the structural characteristics of the assets and the structural characteristics of the technology match.” |

Each of these categories warrants its own dedicated analysis. Article 8 of this series will treat tokenized resort real estate in detail. Article 9 will treat credit unions. Article 11 will treat sovereign debt and infrastructure. Each will examine the structural opportunity, the regulatory considerations, the tax position, the audit and assurance architecture, the operational risk profile, and the strategic decision criteria. None of them is straightforward. All of them are real.

| PART IV

The Strategic Choice Now Before Caribbean Boards and Regulators |

Given the inflection-point evidence, the regional position, and the use case relevance, what should Caribbean boards and Caribbean regulators actually do? The answer divides into three distinct strategic options, and it is worth being explicit about all three because each carries its own logic and its own consequences.

Option 1: Strategic abstention

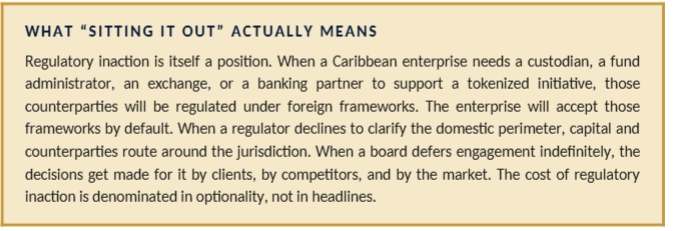

The first option is to continue deferring engagement. Wait until the regulatory framework is mature. Wait until the global market has stabilised. Wait until peer Caribbean institutions have moved first. The argument for strategic abstention is that the field is genuinely uncertain, the supervisory environment is incomplete, and prudence in the face of uncertainty is a defensible posture for fiduciaries. The argument against strategic abstention is that the cost of inaction is denominated in optionality, in market position, and in capability — and these are losses that compound silently. By the time the framework is mature, the institutions that built capability through staged engagement will have a strategic advantage that abstention cannot recover.

Option 2: Strategic engagement under structure

The second option is to engage — carefully, conservatively, under structure. Conduct a maturity assessment. Identify the use cases of greatest strategic relevance to the institution. Develop the governance, assurance, tax, and operational architecture necessary to support a controlled pilot. Engage with regulators proactively rather than reactively. Build internal capability and external advisory relationships. Move from awareness to defined practice over a period of one to two years. This is the path the DAGAF™ framework was built to support. The argument for strategic engagement under structure is that it captures optionality, builds capability, and positions the institution to participate at scale when conditions allow. The argument against it is cost — the diagnostic, the policy work, the legal and tax positioning, the assurance arrangements all require investment without immediate revenue return.

Option 3: Aggressive first-mover positioning

The third option is to go first — to commit substantial resources to becoming a regional reference point in tokenization, to engage publicly with regulators, to issue tokenized instruments at scale, and to capture the brand and capability advantages of leadership. Aggressive first-mover positioning has produced strategic advantages in other Caribbean industries; it has also produced spectacular reputational damage in those that have moved without governance and assurance discipline. The argument for it is the size of the strategic prize. The argument against it is the size of the regulatory, reputational, and operational risk if execution is imperfect.

| DAWGEN GLOBAL’S POSITION

Dawgen Global’s position is that strategic engagement under structure is the right path for most Caribbean institutions in 2026. Strategic abstention surrenders optionality without commensurate benefit. Aggressive first-mover positioning carries asymmetric risk that is rarely justified by the marginal advantage available. Engagement under structure captures the optionality, builds the capability, and protects the institution against the principal failure modes — governance breach, regulatory enforcement, audit qualification, custody loss, and reputational damage. The DAGAF™ framework operationalises this position. |

The choice is not symmetric across institutional categories. Boards of regulated financial institutions, credit unions, listed entities, and large family offices are operating under fiduciary obligations that meaningfully constrain the abstention option. Public-sector institutions — central banks, finance ministries, debt management offices, statutory bodies — face different considerations again, with public-interest obligations that elevate the cost of regulatory drift. Mid-market private companies have more latitude, but the latitude narrows as the industry consolidates around tokenized infrastructure standards.

Introducing DAGAF™ — The Lens for the Series Ahead

DAGAF™ — the Digital Asset Governance & Assurance Framework — is Dawgen Global’s contribution to the work of strategic engagement under structure. The framework is anchored in international standards: International Standards on Auditing, IFRS, the COSO Internal Control framework, ISO/IEC 27001, the Financial Action Task Force standards, the Basel Committee’s positions on crypto-asset exposures, and the published positions of the Bank for International Settlements. It is calibrated for Caribbean institutional scale and CARICOM regulatory plurality. It is conservative by design — it presumes that tokenization decisions clear governance and assurance gates before technology selection, not after.

The framework is built around seven interlocking pillars: Governance and Board Oversight; Regulatory and Legal Compliance; Tax Treatment and Reporting; Audit and Assurance; Cyber, Custody and Operational Risk; Investor and Market Conduct; and Strategic Use Case Selection. A five-level maturity model — Unaware, Aware, Defined, Managed, Optimised — applies uniformly across the seven pillars, producing thirty-five assessment dimensions in total. The full instrument is set out in Appendix A of the DAGAF™ White Paper and is intended for direct use by boards, audit committees, regulators, and engagement teams.

The eleven articles that follow this one will work through the framework in detail. Article 2 will examine the principal foreign frameworks — MiCA, GENIUS, CLARITY — and what they mean for Caribbean entities and counterparties. Article 3 will treat the DAGAF™ architecture itself in depth. Articles 4 through 7 will examine the governance, regulatory, tax, and audit pillars in turn. Articles 8 through 10 will work through the principal Caribbean use cases — resort real estate, credit unions, family offices. Article 11 will examine sovereign debt and infrastructure tokenization. Article 12 will close the series with a 24-month roadmap from pilot through programme.

Each article in this series is intended to be substantive on its own terms. Together they form the editorial expression of a framework Dawgen Global has built specifically for the work of engaging with tokenization in the Caribbean. The framework will evolve. The market will evolve. The regulatory environment will evolve. What does not evolve — what should not evolve — is the discipline that fiduciary obligations impose on the decisions our boards and our regulators are now making.

| “The question is no longer whether the Caribbean engages with tokenization, but how, when, and on what governance and assurance architecture.” |

Caribbean enterprises and Caribbean regulators have a window in which to shape the regional framework rather than to inherit one. The window is open. It will not remain open indefinitely. The decade ahead will reward the institutions that treated tokenization as a serious institutional question deserving serious institutional treatment. DAGAF™ is Dawgen Global’s framework for that work.

ABOUT THE AUTHOR

Dr. Dawkins Brown is the Executive Chairman of Dawgen Global, an independent integrated multidisciplinary professional services firm headquartered in Kingston, Jamaica, operating across the Caribbean. The firm advises Caribbean enterprises, regulators, and public-sector institutions on audit and assurance, tax, risk management, cybersecurity, IT and digital transformation, corporate recovery, M&A, business advisory and strategy, accounting outsourcing, and human capital. Dr. Brown is the architect of DAGAF™ and is the Founding Editor of Caribbean Boardroom Perspectives.

ABOUT THIS SERIES

The Caribbean Tokenization Imperative is a 12-article series introducing the DAGAF™ framework. Article 1 (this article) opens the series. Article 2 — Reading the Global Map: MiCA, GENIUS, CLARITY — will be published in the next edition. Subsequent articles will treat each DAGAF™ pillar in turn, examine principal Caribbean use cases, and conclude with a 24-month implementation roadmap. The full DAGAF™ White Paper is available on request.

© 2026 Dawgen Global. All rights reserved. DAGAF™ is a proprietary framework of Dawgen Global.

About Dawgen Global

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

Email: [email protected]

Email: [email protected]  Visit: Dawgen Global Website

Visit: Dawgen Global Website

WhatsApp Global Number : +1 555-795-9071

WhatsApp Global Number : +1 555-795-9071

Caribbean Office: +1876-6655926 / 876-9293670/876-9265210  WhatsApp Global: +1 5557959071

WhatsApp Global: +1 5557959071

USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements