Resilience is adoption’s silent engine

In islands where storms redraw shorelines and power flickers like a heartbeat, payments that only work when the sun shines and the fiber holds won’t win people’s trust. The Caribbean doesn’t need “cashless.” It needs cash-resilient digitization: rails that hum during normal days, degrade gracefully during outages, and snap back fast. When we design for the worst five days of the year—not the average afternoon—consumers and merchants will bet on digital without fear of being stranded when they need money most.

1) The reality of downtime: where, how, and why systems fail

Single points of failure are everywhere in fragile geographies:

-

Power dependencies: POS terminals, routers, cell towers, and bank branches all rely on electricity; fuel shortages for generators cascade into longer outages.

-

Connectivity bottlenecks: Backhaul fiber cuts, tower misalignment after high winds, and congested cells on cruise-ship days throttle throughput.

-

Operational choke points: Settlement windows, batch jobs, and reconciliation processes scheduled at night collide with curfews and rotating blackouts.

-

Human factors: Merchants lack clear playbooks; front-line staff don’t know rules for “offline acceptance” or daily caps; consumers panic-withdraw.

Translation: Any “digital by default” plan must assume intermittent power and patchy connectivity—and still work.

2) Design goal: graceful degradation, not abrupt failure

A resilient payment system answers three questions under stress:

-

Can I still accept a payment now? (Even if the network is down.)

-

What are the limits and who holds the risk? (Clear caps and liability rules.)

-

How will the system reconcile later—automatically and transparently? (No guesswork.)

The better those answers, the more cash-like (read: reliable) digital feels on bad days.

3) Offline-capable toolset: what to deploy (and when)

Think in layers, ordered from lowest to highest dependency on infrastructure. Each layer has caps to manage risk.

A) Visual QR with deferred authorization (store-and-forward)

-

How it works: Consumer scans merchant QR; app generates a cryptographically signed token (amount + time + merchant ID). The token queues locally and auto-posts when either party reconnects.

-

Risk control: Per-payment and daily caps (e.g., US$20 per txn; US$60/day). Token expiry window (e.g., 24h). Duplicate-prevention via nonce.

-

Best for: Markets, food stalls, taxis, pop-ups, festivals.

B) NFC “tap when dark”

-

How it works: Phones exchange signed payloads over NFC without internet. Merchant phone accumulates transactions; reconciliation occurs when either side comes online.

-

Risk control: Same caps as above; device attestation to limit rooted or tampered devices.

-

Best for: Transport, delivery, service professionals.

C) USSD / SMS fallbacks (feature-phone friendly)

-

How it works: Short codes trigger menu flows on 2G/3G; confirmations via SMS.

-

Risk control: Lower caps, step-up PINs for higher values, timeouts to prevent ghost debits.

-

Best for: Rural areas, older devices, low bandwidth.

D) Paper or plastic “disaster vouchers” (pre-provisioned)

-

How it works: Regulator or utility prints secure, serialised vouchers redeemable at merchants; later reimbursed over rails.

-

Risk control: Fixed denominations, issuer signatures, limited validity windows.

-

Best for: Immediate post-hurricane relief when digital/ATM infrastructure is impaired.

Key principle: Communicate caps and liability in one sentence at the point of use:

“Offline limit: $20 per payment, $60/day; you’re protected for eligible offline transactions.”

4) Settlement during disruption: making T+0 feel real when networks aren’t

Instant settlement is adoption’s engine, but outages complicate the guarantee. A pragmatic approach:

-

Tiered guarantees:

-

Online transactions: true T+0.

-

Offline transactions: provisional T+0 up to a daily ceiling per merchant; convert to final when tokens sync.

-

-

Liquidity buffers: Scheme providers maintain float pools to fund provisional settlements during long outages.

-

Auto-netting on recovery: The system nets provisional credits against reconciled posts; publish the math to merchants.

This retains the cashflow advantage merchants care about while capping ecosystem risk.

5) Disaster playbooks: who does what, and when

A plan no one can find is not a plan. Publish short, printable playbooks for merchants, PSPs/banks, and regulators.

Merchant playbook (one page, laminated)

-

Stay open kit: Printed static QR; battery bank; backup charger; paper receipt pad.

-

Offline acceptance rules: Caps, steps to verify payer, what to do if a token fails to sync.

-

Cash handling: Temporary float guidance; counterfeit checks; deposit procedure after curfew.

-

Hotline + WhatsApp: Real humans for outages; canned scripts for staff.

PSP/Bank playbook

-

Service levels under outage: Status page + SMS updates; target recovery windows.

-

Fee policy: Temporary fee caps or waivers for essential categories (food, fuel, water).

-

Settlement: Provisional T+0 policy; reconciliation timeline; dispute handling.

Regulator playbook

-

Emergency directives template: Fee caps, data-zero-rating for wallet apps, curfew exceptions for cash logistics.

-

Inter-agency comms: Telco, central bank, utilities, disaster agency signal plan—one voice.

-

Cash replenishment: Pre-positioned ATM and branch cash; armed transport protocols.

6) Testing, drills, and observability: resilience you can measure

Don’t trust, test. Run quarterly tabletop exercises and at least one live failover drill per year.

-

Tabletop: Simulate tower outages, islanded micro-grids, batch reconciliation delays, and cyber incidents.

-

Live drill: 60–90 minute “air gap” for a defined region; measure offline acceptance rates, queue depth, sync time, dispute incidence.

-

Telemetry to watch:

-

Offline transactions as % of total during event

-

Average sync time post-restoration

-

Merchant churn and complaint volume

-

Dispute rate/amount for offline transactions

-

Liquidity buffer utilization vs. thresholds

-

Publish a post-mortem summary (scrubbed) to build public trust.

7) Security architecture: keep it tight when the lights are out

-

Device attestation: Block rooted/jailbroken devices from offline acceptance or enforce stricter caps.

-

Token design: Signed, time-boxed, unique nonces; replay prevention; clock-skew tolerance.

-

Step-up auth: PIN/biometric for amounts over micro caps even in offline modes.

-

Tamper-evident logs: Local append-only journal for offline events to support disputes.

-

Compromised-merchant response: Remote kill-switch for QR/tap credentials; rapid re-issue procedures.

8) Infrastructure partners: telcos and utilities are co-architects

Resilience is shared. Formalize MOUs with telcos and utilities:

-

Zero-rated data for wallet apps and status pages during declared emergencies.

-

Power prioritization for data centers, switching nodes, and key retail corridors (fuel, food, water).

-

Temporary cell on wheels (COWs) and satellite links for critical hubs (ports, hospitals, shelters).

-

Messaging lanes: Reserve capacity for payment status SMS/USSD to reduce rumor-driven cash runs.

9) Government as anchor user: pay, procure, and protect on the same rails

-

G2P (government-to-person): Emergency stipends via wallet rails with offline redemption at certified merchants.

-

G2B (government-to-business): Emergency procurement and vendor payments on instant rails; reduces cash logistics during curfews.

-

Consumer charter: A plain-language rights card (refund windows, dispute SLAs, fee caps) that doubles as public education.

Government use normalizes the rail, and the rail strengthens government’s response capacity.

10) Tourism stress test: designing for cruise days and festival spikes

Island economies swing with visitor surges. Design for peak-hour load, not averages:

-

Pre-event merchant kits: QR signage, offline instructions, laminated pricing in local currency with optional FX display.

-

Queue-friendly UX: Dynamic QR totals; one-tap repeat amounts; offline caps visible at checkout.

-

Rapid dispute lanes: Festival-specific hotline; 48-hour fast-track resolution for sub-$25 disputes.

If digital is slower than cash when the market is busiest, merchants will revert. Make the busiest hour the proudest hour.

11) CBDCs, stablecoins, and the resilience question

Central bank digital currencies (CBDCs) promise sovereign settlement and potential offline features; stablecoins offer cross-border speed. The resilience test is the same:

-

Offline CBDC must support signed device-to-device transfers with strict caps and robust double-spend prevention.

-

Stablecoin acceptance must abstract FX risk for merchants and keep finality and fee guarantees crystal clear.

-

Interoperability first: Whether CBDC or stablecoin, it must plug into the same QR/tap rails and dispute playbooks—no parallel universes.

12) The Caribbean Spotlight: staying open when skies close

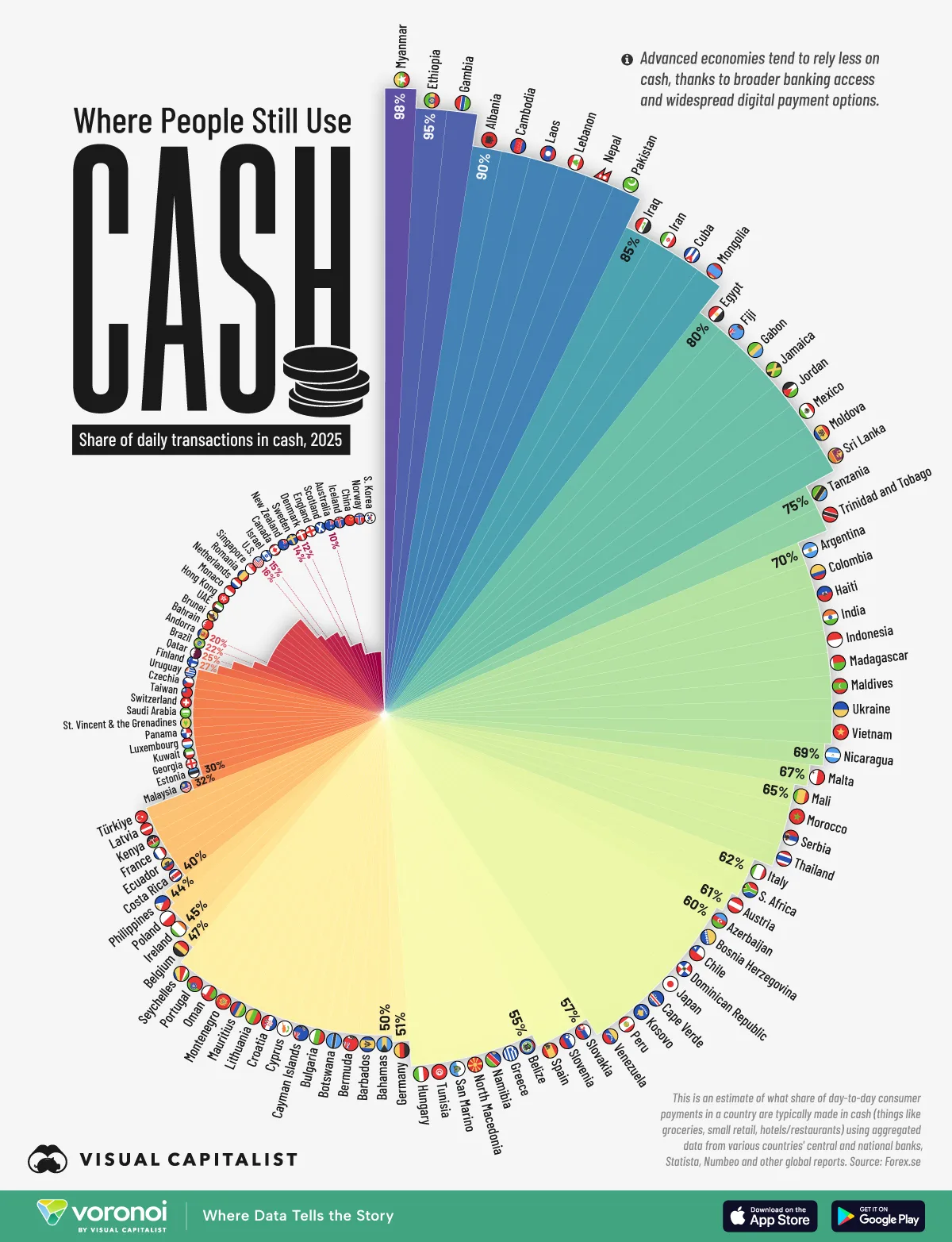

From the visualization’s Caribbean arc, day-to-day transactions still skew cash-heavy (e.g., Jamaica ~80%, Trinidad & Tobago ~75%, Haiti ~70%, Dominican Republic ~60%, Bahamas ~51%, Barbados ~50%, with several OECS markets similarly elevated). That’s rational in disaster-prone geographies: cash is offline by design. To bend the curve safely, pair every digital adoption push with resilience guarantees.

Five actions to launch this season

-

Publish a national offline-payments policy with simple caps (e.g., $20/txn, $60/day) and plain-English liability rules.

-

Distribute “Stay-Open” merchant kits (printed QR, signage, battery bank guidance, hotline card).

-

Stand up liquidity buffers so provisional T+0 continues through multi-day outages.

-

Zero-rate wallet traffic during declared emergencies; coordinate SMS updates with telcos.

-

Drill twice before hurricane season: a tabletop with banks/telcos/utilities/regulators; a 60-minute live failover in a defined district.

Quick wins by sector

-

Transport (route taxis, minibuses): Tap-to-phone + USSD fallback; laminated fare tables with QR.

-

Fresh markets & street food: Static QR + offline tokenization; token caps printed next to codes.

-

Fuel & pharmacies: Priority power and connectivity; dynamic QR and POS-lite features for reconciliation.

-

Shelters & relief sites: Redeemable disaster vouchers; queued digital payouts; agent cash-out windows.

13) Metrics that prove resilience (and earn adoption)

-

Offline completion rate during outages (% of attempted offline txns that later reconcile).

-

Median sync time to settlement after restoration.

-

Dispute incidence and resolution time for offline txns.

-

Merchant uptime (% of merchants processing payments despite grid/network failure).

-

Public trust index (quarterly consumer/merchant pulse on “Will digital work on a bad day?”).

Publish these as a Resilience Scorecard; reputations rise with transparency.

14) Policy levers for confidence at scale

-

Interoperable QR standard (national) with certified offline extensions.

-

Mandatory T+0 for micros (provisional allowed during outages) with daily caps.

-

Micro-fee bands (free under US$2; ≤0.5% for ≤US$10) to keep small-ticket digital competitive with cash.

-

Tiered e-KYC so vulnerable households onboard quickly; limits expand with usage.

-

Disaster directives ready to issue: fee caps, data zero-rating, cash logistics exemptions, and consumer protection reminders.

15) Field notes: how resilient design changes behavior

-

Market vendor: After receiving a kit (printed QR + instructions), she continues trading through a 9-hour outage; 70% of sales reconcile within 15 minutes of network return; provisional T+0 pays suppliers next morning.

-

Taxi driver: Uses tap-to-phone with offline tokens during a storm-related data dip; caps prevent over-exposure; next day, the app reconciles and sends a WhatsApp summary he can share with his base.

-

Corner shop: When a power cut hits, the owner switches to USSD acceptance; fuel and candle sales continue; later, dynamic QR resumes for speed.

Common thread: With clear caps, instant (or provisional) settlement, and simple rules, merchants stay open, customers keep buying, and the economy keeps moving—even while the grid heals.

16) Closing: resilience first, adoption follows

Digital payments don’t earn trust by being perfect; they earn trust by being predictably useful on imperfect days. For the Caribbean, that means offline-capable acceptance, transparent limits, provisional T+0, liquidity buffers, and practiced playbooks with telcos and utilities. Build those foundations and everyday life—markets, transport, tourism, remittances—will shift from notes to nodes without sacrificing the safety net cash has always provided.

Work with Dawgen Global

Design your cash-resilient digitization roadmap with us: drills, playbooks, fee/settlement policy, and merchant kits tailored to your island’s realities.

-

Book a 30-minute payments strategy consult.

-

Request our Payments Resilience Checklist and Offline Acceptance Policy Template.

Contact: 🔗 https://dawgen.global/ | 📧 [email protected] | 📞 USA: 855-354-2447

About Dawgen Global

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

✉️ Email: [email protected] 🌐 Visit: Dawgen Global Website

📞 📱 WhatsApp Global Number : +1 555-795-9071

📞 Caribbean Office: +1876-6655926 / 876-9293670/876-9265210 📲 WhatsApp Global: +1 5557959071

📞 USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements