Notes to Nodes: The Great Payment Transition

Why the till decides the future

Consumers may love convenience, but merchants decide which payment options survive. If accepting a payment is slower, costlier, or riskier than taking cash, the answer is simple: cash wins. The turning point toward digital arrives when a typical day’s takings are cheaper to accept, faster to settle, and safer to hold than notes in the drawer. This article unpacks the merchant math—fees, hardware, settlement, fraud, and reconciliation—and shows how a pragmatic bundle (QR + tap-to-phone + instant settlement + clear dispute rules) can flip the decision for Caribbean micro and small businesses.

1) The real cost of accepting a payment

Think about acceptance cost as a stack:

-

Merchant Discount Rate (MDR) / fees

-

Percentage fee (e.g., 0.5–3%) or a flat micro-fee on each transaction.

-

Additional cross-border or currency conversion fees in tourism corridors.

-

-

Hardware & software

-

Traditional terminals: upfront cost or monthly rental; paper rolls; maintenance.

-

Tap-to-phone: uses an existing smartphone; near-zero incremental cost.

-

Printed QR: effectively free; upgrade path to dynamic QR codes if needed.

-

-

Settlement timing

-

T+0 (instant) vs. T+1/T+2 (next day or later).

-

Longer settlement ties up working capital and increases bank-run time.

-

-

Chargebacks & fraud exposure

-

Dispute windows and liability allocation.

-

Card-not-present vs. in-person QR/tap.

-

Social-engineering attacks that create time-drain and revenue leakage.

-

-

Operational friction

-

End-of-day reconciliation, paper slips, error rates.

-

Staff training, device charging, connectivity.

-

Cash has costs too—but they’re often hidden: time to count and deposit, risk of theft/counterfeit, reconciliation errors, and security measures (safes, transport). For small tickets, those frictions add up.

2) A day in the till: three side-by-side scenarios

Assume a beach vendor or corner grocer processes 40 sales of US$5 each (US$200/day).

A) All cash

-

Direct fees: $0

-

Hidden costs: 20–30 minutes of counting; bank deposit trip; risk of loss/shrinkage (1–2% typical in cash-heavy micro retail).

-

Liquidity: Immediate, but manual.

-

Net at day’s end (after 1% shrinkage): $198

B) Card terminal, MDR 2.5%, T+1 settlement

-

Fees: 2.5% × $200 = $5.00

-

Hardware: $20/month amortized to ≈$1/day (assume 20 business days)

-

Settlement: Next day; cashflow timing risk

-

Shrinkage: Near-zero

-

Net: $200 − $5 − $1 = $194

C) QR + tap-to-phone, micro-MDR 0.5%, T+0 settlement

-

Fees: 0.5% × $200 = $1.00 (or a capped micro-fee equivalent)

-

Hardware: $0 (uses phone/printed QR)

-

Settlement: Instant; restock tonight

-

Shrinkage: Near-zero

-

Net: $199

In low-ticket environments, instant settlement + compressed micro-MDR is the game-changer. It narrows the gap with cash while removing shrinkage and deposit runs. The merchant gets back time, safety, and working capital.

3) The settlement dividend: why T+0 matters more than it seems

Merchants don’t just compare fees; they compare cashflow certainty. T+0 creates three compounding benefits:

-

Inventory turns: Same-day funds restock shelves or ingredients—especially critical in island supply chains.

-

Credit avoidance: Less need for costly short-term borrowing to bridge settlement gaps.

-

Trust: When money lands immediately, the system “feels” as reliable as cash.

A practical target for small merchants is: instant settlement up to a daily cap (e.g., US$500–1,000), then T+1 beyond that. It hedges risk for providers without punishing micros.

4) Fraud, disputes, and the psychology of risk

For a merchant, one painful dispute can erase a month of savings. Adoption rises when rules are clear and fair:

-

Transparent SLAs: e.g., “consumer has 7 days to dispute; merchant response within 3; resolution within 10.”

-

Risk-based liability: In-person QR/tap with verified device + matching name/amount = merchant-protected for low tickets.

-

In-app receipts and name confirmation: Reduce friendly fraud (“I don’t recognize this charge”).

-

Education nudges: Short videos and scripts for staff on how to verify, how to refuse suspicious payments, and how to escalate.

Fraud controls must be visible to feel real. A banner that says “You are protected under Rule X for purchases under $25” changes behavior.

5) Hardware-free acceptance: QR and tap-to-phone

QR (static and dynamic)

-

Static QR: Print once; customer enters amount. Lowest cost, slightly higher input error risk.

-

Dynamic QR: App generates amount and order ID; no manual input; clean reconciliation.

Tap-to-phone (NFC)

-

Turns a standard smartphone into a contactless acceptance device—no dongle, no terminal.

-

Ideal for delivery, pop-up markets, taxis, and curbside.

Best practice: start printed static QR for universality + tap-to-phone where phones are NFC-enabled; migrate higher-volume merchants to dynamic QR for speed and clean books.

6) The tourism lens: multi-currency reality without terminal complexity

Caribbean merchants serve locals and visitors. That means:

-

FX awareness: Clear pricing in local currency; optional FX display for tourists; beware hidden conversion fees.

-

Receipts & refunds: Digital receipts reduce chargeback risk and help with tax compliance.

-

Offline modes: Cruise days and festival crowds strain networks. QR with queued authorization and risk-capped offline limits keeps lines moving.

If the digital alternative is slower than cash on a cruise day, the merchant will switch back to cash by noon. Design for the peak-load day, not the average day.

7) The remittance angle: turning inbound flows into everyday spend

Remittances are a major inflow. If those funds land directly into wallets or accounts and can be spent at merchants—not just cashed out—habit changes quickly. Key enablers:

-

Fee-light P2M: Encourage spending at local MSMEs rather than immediate cash-out.

-

Bill-pay hooks: Utilities and schools as anchor use cases.

-

Cash-out nearby: Keep agent liquidity for those who still need physical cash; don’t make digital a trap.

8) Caribbean Spotlight: what merchants tell us

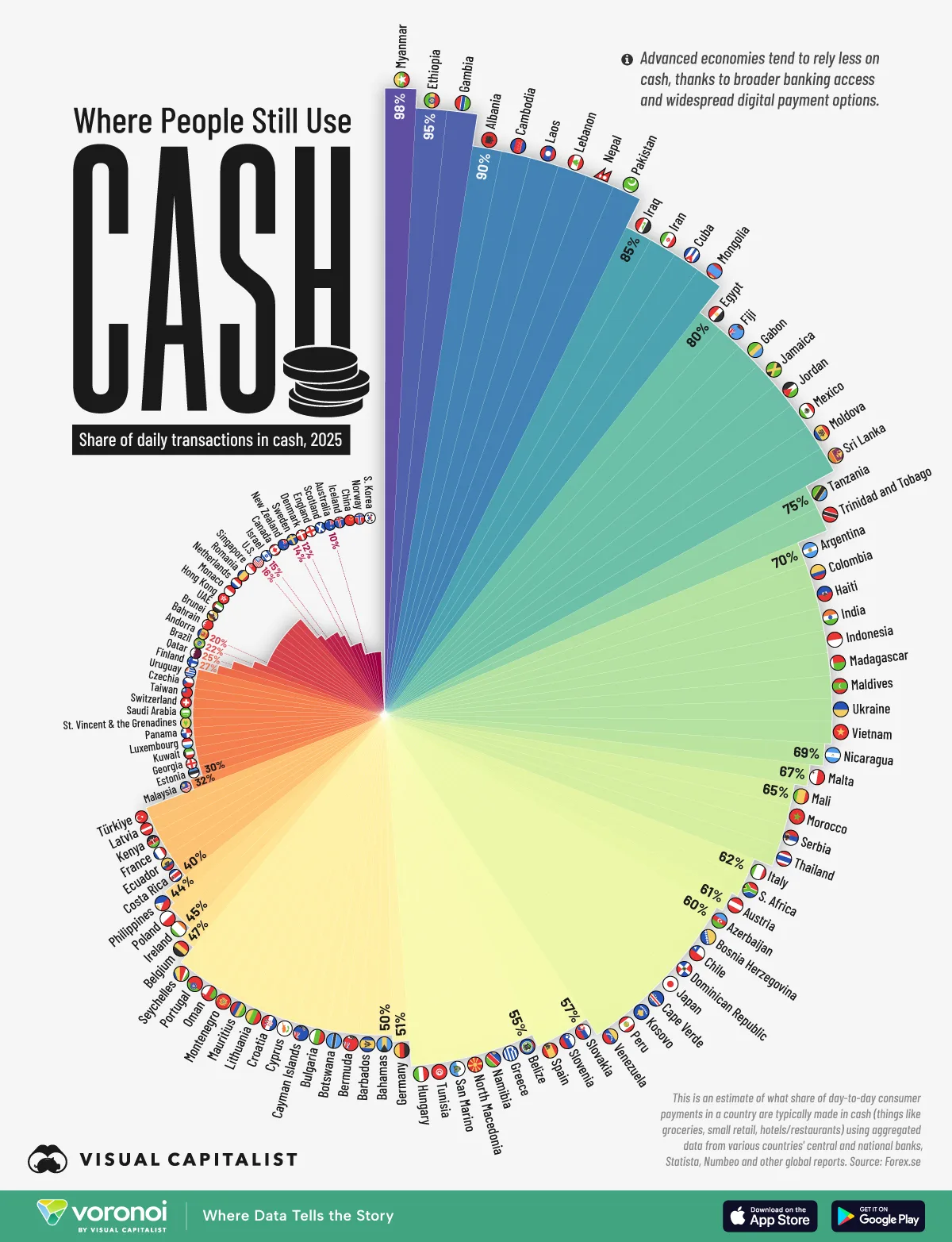

Across the region, the cash share of daily transactions is high (e.g., Jamaica ~80%, Trinidad & Tobago ~75%, Haiti ~70%, Dominican Republic ~60%, Bahamas ~51%, Barbados ~50%, with several OECS islands also in the higher-cash arc). Merchant conversations reveal consistent themes:

-

Terminal cost anxiety for very small volumes and seasonal businesses.

-

Settlement delays that force a next-day restock run or supplier credit.

-

Dispute uncertainty—no one knows “who pays” when something goes wrong.

-

Connectivity gaps during storms, blackouts, or big event days.

Translation: To move the needle, solutions must be hardware-light, instant, interoperable, and offline-capable, with rules that are understood in one read.

9) A practical merchant playbook (micro to small)

Phase 1: Start (Week 1–2)

-

Printed QR kit with signage; tap-to-phone enabled if merchant has NFC smartphone.

-

Instant settlement up to a daily cap; fees ≤ 0.5–0.8% for transactions under US$10.

-

One-page protection card summarizing dispute rules and hotline.

Phase 2: Prove value (Month 1–2)

-

Auto-reconciliation reports sent nightly (PDF + CSV); WhatsApp summary option.

-

Loyalty hooks: small bill credits or cash-back on wallet spends.

-

“Request-to-pay” links for delivery and preorders (no card-on-file needed).

Phase 3: Optimize (Quarter 2–3)

-

Switch to dynamic QR for top 20 items or pre-tax totals.

-

Offer POS-lite app features: inventory counts, daily targets, staff user roles.

-

Micro-working-capital advances repaid via single-digit % of digital sales (transparent, capped).

10) Design patterns that increase acceptance density fast

-

Interoperable national QR

-

One spec all wallets/banks must honor; no “QR islands.”

-

Certification program for consistency and UX quality.

-

-

Fee bands that reward small tickets

-

Examples: free ≤US$2; US$2–$10 at ≤0.5%; caps thereafter.

-

Publish the grid; let merchants compute savings.

-

-

T+0 settlement as the default for micros

-

Display “Funds in your account within minutes” in the onboarding.

-

-

Tap-to-phone as a first-class citizen

-

Great for taxis, delivery, service pros, and pop-ups.

-

-

Offline modes with sensible caps

-

Pre-signed tokens / deferred authorization; auto-sync when online.

-

Communicate caps clearly (e.g., “Offline limit: $20 per payment, $60/day”).

-

-

Dispute transparency

-

Plain-language summary; short videos; in-app banner that says “You are protected.”

-

11) The numbers that matter (merchant-side KPIs)

-

Acceptance density: # of QR/tap-to-phone points per 1,000 residents and per km².

-

T+0 share: % of merchant transactions settled instantly.

-

Micro-ticket share: % of transactions ≤US$10 processed digitally (beachheads for habit change).

-

Dispute rate: # disputes / 1,000 transactions, and average resolution days.

-

Reconciliation accuracy: mismatch rate between app totals and bank statements.

-

Churn: merchants inactive for 30 days—trigger outreach.

12) Risk, resilience, and reputation: what to get right

-

SIM-swap & social engineering: In-app name display, payment verification screens, cooling-off limits for new payees.

-

Vendor lock-in: Open APIs and standards; portability of transaction history.

-

Privacy: Minimize personally identifiable data; clear consent for analytics and marketing.

-

Disaster playbooks:

-

Power: battery banks and low-power modes.

-

Network: USSD/QR fallback and queued transactions.

-

Cash: agent liquidity and emergency cash-out windows.

-

-

Human support: A real hotline with short wait times beats a perfect FAQ.

Your reputation rides on the first bad day—design for it now.

13) Policy levers that unlock the merchant switch

-

Publish an interoperable QR standard and certification process; prohibit non-interoperable closed loops for retail payments at national scale.

-

Tiered e-KYC so micro-merchants onboard with minimal documents and grow limits with usage.

-

Cap MDR for small tickets and encourage flat micro-fees; set transparency rules for FX in tourism corridors.

-

Mandate T+0 for small merchants up to a daily ceiling, with settlement guarantees backed by scheme providers.

-

Consumer protection charter: simple dispute windows, liability clarity, and relief for obvious fraud patterns.

-

Public procurement & G2P on the same rails to normalize acceptance and fund ecosystem scale.

14) Merchant stories: where the math already works

-

Market food stall: printed QR taped to a cooler; instant settlement; end-of-day report via WhatsApp. Cash share drops from 100% to 30–40% in 60 days.

-

Taxi/minibus: tap-to-phone for commuters + QR for tourists; fewer cash management headaches; better end-of-shift reconciliation; higher tips.

-

Craft vendor: dynamic QR with itemized totals; dispute protection under low-ticket rules; ability to accept preorders during festivals.

Common thread: no terminal, instant money, clear protection.

15) Caribbean Spotlight

Data cues from the regional arc of the map

-

Daily transactions in cash remain elevated in Jamaica (~80%), Trinidad & Tobago (~75%), Haiti (~70%), Dominican Republic (~60%), Bahamas (~51%), Barbados (~50%), with several OECS islands also clustered in higher-cash ranges.

-

High-frequency spend categories—minibus/taxi fares, street food, fresh markets, and tips—anchor habits.

What flips the region’s merchant math

-

Interoperable QR kits for every registered MSME—free to start.

-

Tap-to-phone for transport, delivery, and pop-ups.

-

Instant settlement (T+0) up to daily caps; micro-MDR bands for ≤US$10 transactions.

-

Dispute clarity summarized in a one-page “Merchant Rights” card.

-

Offline acceptance for storm season and big events.

Quick wins

-

Digitize tips and excursions in tourism corridors with QR; bundle signage and staff scripts.

-

Integrate remittance-to-merchant flows (spend directly, not cash-out first).

-

Offer utility bill credits for wallet spends to create habit loops.

16) Closing: cheaper, faster, safer—or it doesn’t stick

Merchants won’t move because digital is fashionable. They’ll move when today’s takings are worth more, sooner, with less risk than cash in the drawer. That means hardware-light acceptance, instant settlement, micro-fee economics, clear protections, and offline resilience. Get those five right and the Caribbean’s daily commerce shifts—naturally and permanently—from notes to nodes.

Work with Dawgen Global

Ready to quantify the merchant math in your market and move 10–20 points off cash without risking trust?

-

Book a 30-minute payments strategy consult.

-

Request our Merchant Acceptance Calculator and Payments Resilience Checklist tailored to Caribbean MSMEs.

Contact: 🔗 https://dawgen.global/ | 📧 [email protected] | 📞 USA: 855-354-2447

About Dawgen Global

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

✉️ Email: [email protected] 🌐 Visit: Dawgen Global Website

📞 📱 WhatsApp Global Number : +1 555-795-9071

📞 Caribbean Office: +1876-6655926 / 876-9293670/876-9265210 📲 WhatsApp Global: +1 5557959071

📞 USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements