Tax policy is one of the most powerful tools available to governments for shaping economic performance, promoting fairness, and financing essential public services. Among developed economies—particularly those within the Organisation for Economic Co-operation and Development (OECD)—the composition of tax revenue reflects strategic decisions that balance competitiveness, economic efficiency, and social objectives.

In designing an optimal tax mix, policymakers must consider not only how much revenue is raised, but also how it is raised. Different taxes have varying impacts on investment, employment, and consumption patterns.

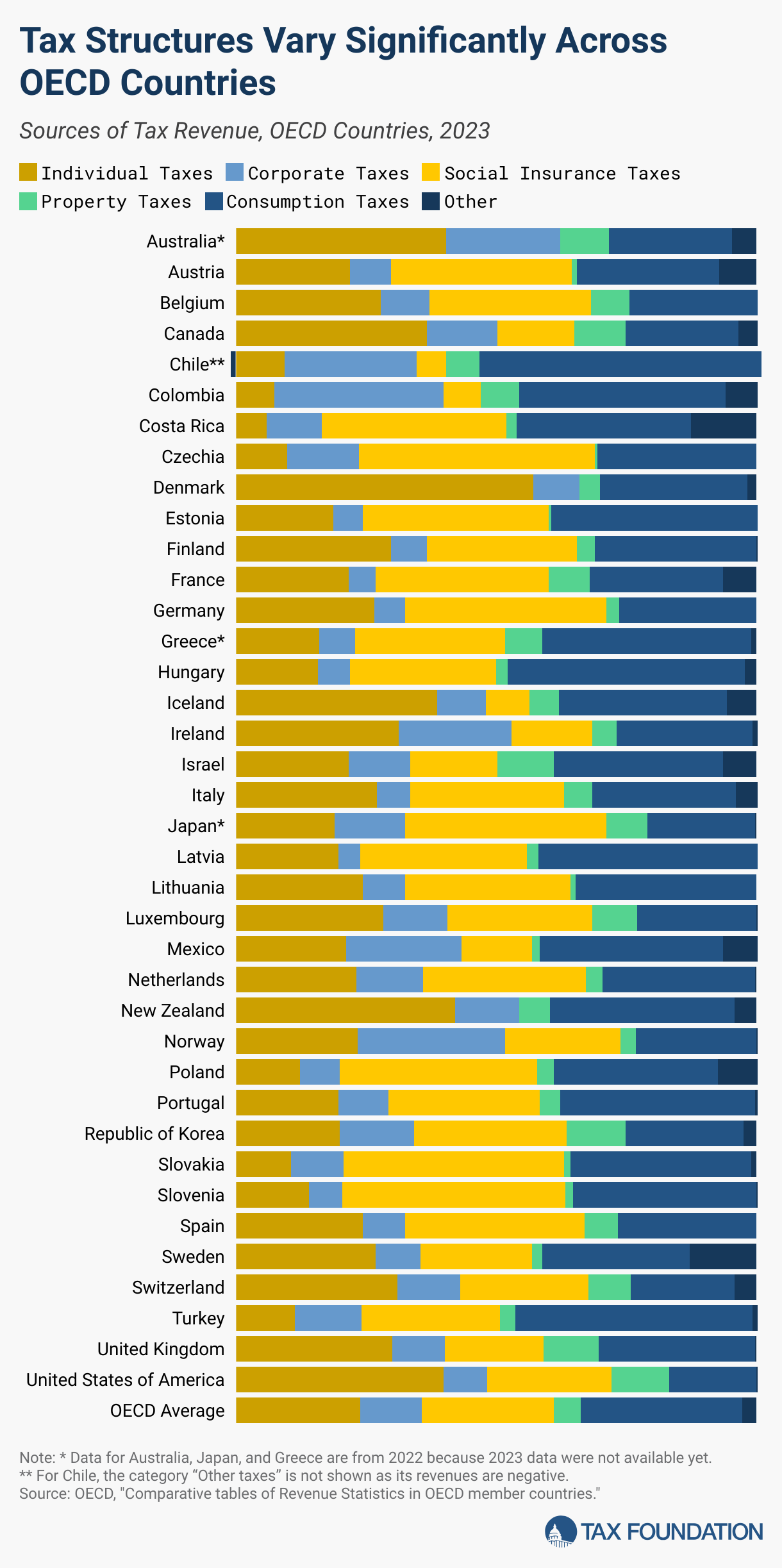

The OECD Tax Mix: A Snapshot

In 2023, the OECD average tax composition was as follows:

-

Consumption Taxes: 31.1%

-

Social Insurance Taxes: 25.5%

-

Individual Income Taxes: 23.7%

-

Corporate Income Taxes: 11.9%

-

Property Taxes: 5.1%

-

Other Taxes: 2.7%

This distribution shows a clear preference for consumption and social insurance taxes over more distortive taxes like high-rate personal income taxes or volatile corporate taxes.

Why the Mix Matters

Economic research and policy experience suggest that taxes on income—both personal and corporate—can have a more negative impact on economic activity than taxes on consumption or property.

-

Income Taxes: Often discourage work effort, entrepreneurship, and investment. High rates can lead to tax avoidance and reduced labor participation.

-

Consumption Taxes: Typically broader-based, more stable, and less distortive to economic decisions.

-

Social Insurance Contributions: Not only fund social security and healthcare systems but also create direct entitlements, making them less politically contentious.

This is why many OECD countries have shifted toward consumption and social insurance taxes over the past three decades.

Long-Term Trends in Revenue Composition

Comparing 1990 with 2023 reveals important shifts:

-

Social Insurance Taxes: Increased by 2.2 percentage points, reflecting a move toward more stable, entitlement-linked revenue sources.

-

Individual Income Taxes: Decreased by 6.2 percentage points, showing a deliberate reduction in reliance on potentially growth-inhibiting taxes.

-

Corporate Income Taxes: Increased from 7.7% to 11.9%, despite global reductions in statutory corporate tax rates. This rise partly reflects the integration of new OECD members—such as Chile, Colombia, and Mexico—where corporate tax revenues exceed 20% of total government revenue.

Case Study: The United States as an Outlier

The United States remains the only OECD country without a value-added tax (VAT). Instead, it relies heavily on state-level sales taxes and selective excise taxes. This choice results in the U.S. raising just 16.8% of total revenue from consumption taxes, well below the OECD average of 31.1%. While this may reflect historical and political factors, it limits the U.S.’s ability to shift away from income-based taxation.

Policy Implications: Designing Efficient and Stable Tax Systems

A well-structured tax system should:

-

Minimize Distortions: Shifting from high-rate income taxes to broader consumption or property taxes can reduce disincentives to work and invest.

-

Promote Stability: Relying on less volatile tax bases—like VAT and social insurance contributions—can improve fiscal predictability.

-

Enhance Competitiveness: Lower corporate tax rates, paired with alternative revenue sources, can attract investment without compromising fiscal health.

-

Ensure Equity: Any shift must balance efficiency with fairness, protecting lower-income households through targeted transfers or exemptions.

Dawgen Global’s Perspective

For Caribbean and emerging market policymakers, the lessons from the OECD experience are both timely and relevant:

-

Diversification of revenue sources is critical to reducing economic vulnerability. Economies overly dependent on a narrow set of taxes—particularly corporate income or trade taxes—are more susceptible to external shocks and global market fluctuations.

-

Heavy reliance on corporate or income taxes can expose economies to significant volatility during downturns, when profits fall and employment contracts.

-

Building strong, broad-based consumption tax systems can provide a stable foundation for long-term fiscal planning, while minimizing distortions to investment and productivity.

As global competition for investment intensifies, the ability to finance government operations without imposing excessive economic distortions will be a decisive factor in sustaining growth. Policymakers who design tax systems that are balanced, efficient, and resilient will be best positioned to attract investors while funding critical infrastructure and social programs.

How Dawgen Global Tax Team Supports Effective Tax Planning

At Dawgen Global, our Tax Advisory Team works at the intersection of policy insight, technical expertise, and strategic foresight. We assist governments, corporations, and policymakers by:

-

Tax Framework Design & Reform – Advising on how to rebalance tax systems to reduce reliance on volatile sources and increase fiscal stability.

-

Revenue Diversification Strategies – Identifying new, broad-based, and less distortionary tax bases to improve economic resilience.

-

Corporate Tax Optimization – Helping businesses legally reduce their tax liabilities while maintaining compliance with local and international regulations.

-

Consumption Tax Advisory – Guiding the implementation or enhancement of VAT, GST, and other consumption-based taxes to maximize revenue with minimal economic drag.

-

Scenario Modelling & Impact Analysis – Using economic and financial models to project the impact of tax policy changes on revenue, investment, and economic growth.

-

Cross-Border & International Tax Solutions – Navigating transfer pricing, treaty benefits, and tax-efficient structuring for companies operating in multiple jurisdictions.

Our approach is holistic—we look at the economic context, sectoral impacts, and long-term growth objectives to ensure that tax systems are not only compliant but also growth-enabling.

Your Next Step: Book a Consultation with Our Experts

Whether you are a policymaker seeking to modernize your country’s tax framework, or a business leader aiming to optimize your corporate tax strategy, Dawgen Global can help you make Smarter and More Effective Decisions.

📲 Book your consultation today via our Global WhatsApp: +1 555-795-9071

Our tax specialists are ready to discuss your unique challenges and provide tailored, actionable solutions that align fiscal sustainability with economic growth.

About Dawgen Global

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

✉️ Email: [email protected] 🌐 Visit: Dawgen Global Website

📞 📱 WhatsApp Global Number : +1 555-795-9071

📞 Caribbean Office: +1876-6655926 / 876-9293670/876-9265210 📲 WhatsApp Global: +1 5557959071

📞 USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements