Freeing Cash, Reducing Financing Pressure, and Funding Growth Without Borrowing More

Executive Summary

When leaders think “cost reduction,” they often think expense cuts: headcount, procurement, travel, projects, and overhead. Yet one of the most powerful and underused profit levers sits on the balance sheet: working capital.

Working capital is not just a finance metric. It is the operational footprint of how an organisation buys, makes, sells, and collects. Excess inventory, slow receivables, weak payment discipline, and poorly governed terms are hidden costs—because they increase financing needs, raise interest expense, and compress profitability through cash pressure.

In today’s economic climate—higher interest rates, tighter liquidity, and elevated input costs—working capital improvement becomes a direct cost reduction strategy. Every day you reduce:

-

DSO (days sales outstanding)

-

DIO (days inventory on hand)

-

DPO (days payable outstanding)

can free cash that reduces overdraft utilisation, lowers borrowing costs, strengthens supplier resilience, and funds technology or growth initiatives.

This article explains:

-

how working capital becomes “silent overhead”

-

where the Caribbean reality amplifies cash pressure (imports, FX, logistics, seasonality)

-

practical levers to release cash in receivables, inventory, and payables

-

why many working capital programmes fail (and how to prevent boomerang effects)

-

how to use Dawgen’s V.A.L.U.E.-Chain Cost Advantage Framework™ to deliver validated, sustainable cash release

Why Working Capital Is a Cost Reduction Lever (Not Just Finance “Housekeeping”)

Every business pays a cost for funding working capital:

-

bank overdraft interest

-

loans and revolving facilities

-

supplier financing cost passed through pricing

-

missed early-payment discounts

-

FX exposure and “panic buying” buffers

-

stock obsolescence and emergency freight

-

time spent chasing cash and resolving disputes

When working capital is poor, the business experiences a predictable pattern:

-

cash pressure increases

-

management tightens spending (often indiscriminately)

-

operations begin firefighting

-

service failures rise

-

profitability deteriorates further

Improving working capital breaks this loop. It reduces the need for expensive financing and makes cost reduction less painful because the business gains breathing room.

The simplest truth:

Cash released from working capital is cash you don’t have to borrow.

And borrowing is more expensive today than it has been in years.

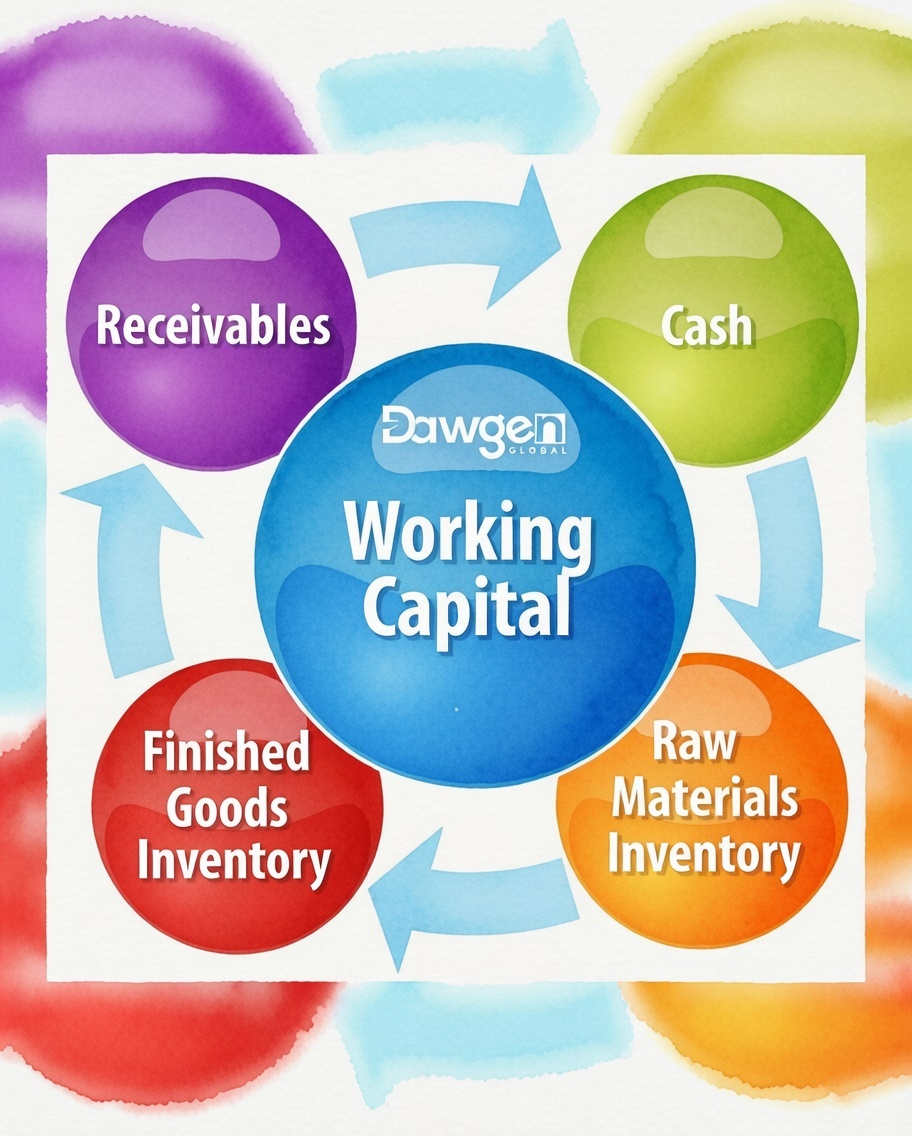

The Working Capital Equation (and What It Really Means Operationally)

Working capital is usually expressed as:

Working Capital = Receivables + Inventory – Payables

The finance definitions are familiar, but the real drivers are operational:

Receivables (DSO)

Driven by:

-

credit policy discipline

-

invoice accuracy

-

disputes and deductions

-

collections cadence

-

customer terms and payment behaviour

-

channel structure and power dynamics

Inventory (DIO)

Driven by:

-

demand forecasting quality

-

SKU complexity and variability

-

lead times and supplier reliability

-

batch size and production scheduling

-

service-level promises

-

poor governance of slow-moving and obsolete stock

Payables (DPO)

Driven by:

-

supplier terms and negotiation

-

procurement discipline

-

invoice processing speed and controls

-

early-payment leakage

-

compliance with payment schedules

-

supplier segmentation and resilience

Working capital is therefore a value chain issue, not a finance-only issue.

The Caribbean Reality: Why Working Capital Pressure Is Often Worse

Many Caribbean organisations face structural factors that intensify working capital drag:

-

high import content and longer replenishment lead times

-

FX constraints and currency volatility

-

multi-island logistics and distribution complexity

-

seasonality (tourism, back-to-school, holidays, agriculture)

-

small market fragmentation and channel power imbalances

-

higher financing costs and tighter liquidity cycles

These conditions often push businesses to hold more inventory “just in case” and tolerate slower collections “to keep customers.” The result: cash trapped everywhere.

The Working Capital Traps That Destroy Profitability

Trap 1: “Sales at all costs” (credit indiscipline)

Revenue is booked, but cash conversion is weak. The business is effectively financing customers.

Trap 2: Inventory as a substitute for capability

Poor forecasting, weak supplier reliability, and unstable operations are “solved” by holding buffer stock.

Trap 3: Uncontrolled terms and exceptions

Different customers get different terms, and those terms drift over time with no governance.

Trap 4: Payables optimisation that breaks suppliers

Extending DPO without segmentation can cause supply disruption, price increases, or loss of service.

Trap 5: Working capital programmes that are “one-off pushes”

Short-term collection drives and stock clearance efforts fade because root causes were never fixed.

Where the Cash Hides: Practical Levers That Work

1) Receivables: Release Cash Without Killing Growth

Receivables improvements are often fastest because they require discipline and process—not major capex.

High-impact receivables levers

a) Fix invoice accuracy and “right-first-time billing”

If invoices are wrong, collections become disputes. Disputes become delays. Delays become cash leakage.

-

standardise pricing and discount approvals

-

reduce manual invoice edits

-

tighten proof-of-delivery documentation

-

resolve recurring dispute root causes

b) Segment customers by payment behaviour, not just revenue

Not all receivables are equal. Create a segmentation such as:

-

reliable payers

-

slow payers but strategic

-

chronic late payers and high-maintenance accounts

Then apply differentiated controls.

c) Collections cadence with ownership

Collections improves when it is run like an operating rhythm:

-

daily/weekly dashboards

-

clearly assigned portfolios

-

escalation rules

-

dispute SLA timers

d) Terms governance (stop “term creep”)

Terms drift quietly. A disciplined business:

-

defines standard terms by segment/channel

-

requires approvals for exceptions

-

monitors effective DSO by customer group

e) Use commercial levers where needed

When customers pay late consistently:

-

link discounts/promotions to payment compliance

-

implement credit holds appropriately

-

restructure pricing and service levels

Quick wins in receivables (0–90 days)

-

“Top 20 overdue” recovery sprint with weekly review

-

dispute clean-up war room

-

eliminate duplicate deductions and double counting

-

tighten credit note governance

-

enforce PO requirements and delivery proof to prevent disputes

2) Inventory: Reduce Cash Traps Without Breaking Service

Inventory is often the largest working capital component and the most politically sensitive. The key is to reduce inventory while protecting customer experience.

The five inventory failure modes (profit destroyers)

You already have the visual for this, and it fits perfectly here:

-

forecast error and planning instability

-

SKU proliferation and slow movers

-

poor replenishment rules and excess safety stock

-

weak discipline on obsolescence and expiry

-

firefighting (expedites, emergency buys, and stockouts)

High-impact inventory levers

a) Segment inventory: “Profit-protecting” vs “Cash-trapping”

Use simple bands:

-

A items: high velocity/high margin (protect service)

-

B items: moderate velocity (optimise)

-

C items: slow movers/low margin (aggressive reduction)

b) Reset safety stock and reorder parameters using reality

Many parameters are “legacy numbers.” Recalibrate based on:

-

actual lead time variability

-

actual demand variability

-

real service level targets by segment

c) Kill or consolidate SKUs that create complexity

Complexity drives inventory. SKU rationalisation is often an inventory strategy disguised as portfolio management.

d) Introduce governance on slow-moving and obsolete stock

A strong discipline includes:

-

monthly SLOB (slow and obsolete) reviews

-

ownership by category

-

triggers for markdowns, returns, disposal, or conversion plans

-

“no new buy” rules for stagnant items

e) Improve forecast + supply reliability rather than buffering

Inventory buffers often exist because:

-

suppliers are unreliable

-

planning is reactive

-

operations are unstable

Fixing these root causes yields sustained cash release.

Quick wins in inventory (0–90 days)

-

freeze new purchases for slow movers

-

run a targeted “SLOB liquidation plan”

-

tighten replenishment to reduce over-ordering

-

stop expediting by introducing an approval rule and root-cause tracking

3) Payables: Extend Terms Without Creating Supply Risk

Payables is a powerful lever, but it must be balanced. A “stretch payables” approach can backfire through:

-

supplier price increases

-

reduced availability

-

quality issues

-

damaged relationships

High-impact payables levers

a) Supplier segmentation

Treat suppliers differently:

-

strategic and critical (protect continuity)

-

leverage suppliers (optimise terms)

-

non-critical suppliers (standardise and consolidate)

b) Terms standardisation and contract discipline

Many organisations have “accidental” terms because contracting is inconsistent.

c) Fix procure-to-pay process speed

If AP is slow, you can’t manage terms intelligently. Process discipline prevents:

-

late fees

-

missed discounts

-

unplanned early payments

d) Prevent early-payment leakage

Early payments happen due to:

-

manual payment runs

-

poor scheduling

-

weak controls

-

supplier pressure without governance

e) Use dynamic discounting strategically

Sometimes paying early creates more value than holding cash—if discounts exceed financing cost. But that should be a deliberate decision, not accidental behaviour.

Quick wins in payables (0–90 days)

-

identify suppliers being paid earlier than terms and correct immediately

-

consolidate payment runs (cadence discipline)

-

renegotiate terms on top spend suppliers where feasible

-

reduce supplier sprawl (fewer vendors = better leverage + lower admin cost)

The Working Capital “Cost Reduction Bridge”

A practical way to position this for management:

-

Cash release (working capital improvement)

-

Reduced financing utilisation (lower overdraft/loan drawdowns)

-

Lower interest expense (direct profit improvement)

-

Improved resilience (less panic buying/expediting)

-

Reinvestment capacity (automation, innovation, growth)

Working capital improvement therefore creates a compounding effect.

Why Working Capital Programmes Fail (and How to Avoid It)

Failure Mode 1: One-time “push” with no root cause fix

Collections temporarily improves, then slides back.

Fix: redesign process + governance, not just messaging.

Failure Mode 2: Inventory reduction that triggers stockouts and service failures

The business panics and over-buys again. Inventory boomerangs.

Fix: segment inventory, protect A-items, and stabilise supply/forecasting.

Failure Mode 3: Payables extension that breaks suppliers

Supply disruption costs more than the cash saved.

Fix: segment suppliers and use balanced terms strategy.

Failure Mode 4: Savings not validated and “net cash” not captured

Paper improvements don’t show up in bank.

Fix: finance validation and disciplined reporting cadence (VCO approach).

How V.A.L.U.E.™ Converts Working Capital Into Sustainable Advantage

V — Validate the Profitability Challenge

Quantify:

-

cash tied up (WC baseline)

-

financing cost and interest burden

-

biggest components by business unit/channel

A — Analyse the Value Chain and Cost-to-Serve

Map where cash gets stuck:

-

slow collections, dispute loops

-

excess buffers, planning failures

-

early payments, weak terms discipline

L — Locate Levers and Build the Opportunity Portfolio

Build an initiative pipeline across:

-

receivables discipline

-

inventory reduction

-

payables optimisation

-

process automation and governance

U — Uplift & Prioritise (Business Case + Roadmap)

Prioritise by:

-

speed to cash release

-

risk to service levels

-

data readiness

-

implementation effort

E — Execute with Governance and Controls

Use the Value Capture discipline:

-

clear workstreams (AR, Inventory, AP/Procurement)

-

weekly cadence

-

issue resolution

-

finance validation to prevent double counting

™ — Transform for Sustainability (Hardwire the Advantage)

Embed:

-

credit terms governance

-

inventory parameter reviews

-

supplier segmentation and contracting discipline

-

dashboards and accountability rhythms

Case Snapshot (Anonymised)

A regional business under financing pressure discovered:

-

DSO inflated due to disputes and invoice errors

-

inventory buffers driven by unreliable lead times and SKU sprawl

-

early payment leakage due to weak AP cadence

Actions taken:

-

dispute war room + invoice accuracy fixes

-

SKU and SLOB discipline + parameter reset

-

supplier segmentation and payment scheduling controls

Result:

-

cash released across AR and inventory

-

reduced overdraft utilisation and interest burden

-

more stable service performance and fewer expedites

Working Capital Is Cost Reduction You Can Bank

In a high-cost, high-interest environment, working capital improvement is one of the most practical ways to protect profitability without cutting capability.

If you can:

-

collect faster (without damaging relationships),

-

hold the right inventory (without stockouts), and

-

pay strategically (without breaking suppliers),

you can fund growth and resilience with your own cash.

Next Step!

Want to unlock trapped cash and reduce financing pressure using a value-protected approach?

Email [email protected] with the subject line “V.A.L.U.E. – Working Capital Cash Release” to request an initial discussion and our data intake checklist.

WhatsApp Global: +1 555 795 9071 | Contact form: https://www.dawgen.global/contact-us/

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

Email: [email protected]

Email: [email protected]  Visit: Dawgen Global Website

Visit: Dawgen Global Website

WhatsApp Global Number : +1 555-795-9071

WhatsApp Global Number : +1 555-795-9071

Caribbean Office: +1876-6655926 / 876-9293670/876-9265210  WhatsApp Global: +1 5557959071

WhatsApp Global: +1 5557959071

USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements