Airlines are often perceived as big, powerful corporations. But behind the brand names and gleaming aircraft lies a harsh reality: commercial aviation is a low-margin, high-risk business. After paying for fuel, aircraft leases, maintenance, staff, airport charges, and financing costs, what remains per passenger is surprisingly small.

At the same time, governments around the world have steadily increased specific taxes on the use of air transport—fixed charges levied on passengers simply for taking a flight. When we compare what governments take in these specific ticket taxes to what airlines earn in profit, a startling picture emerges: in many cases, taxes per passenger are higher than airline profits per passenger, and total tax revenue far exceeds sector profits.

This article examines that imbalance using recent data from IATA’s in-depth study of specific air travel taxes, and explores what it means for airlines, passengers, and policymakers—especially in regions that depend heavily on air connectivity.

1. A Low-Margin Industry Facing a High Tax Burden

Aviation is capital-intensive and cyclical. Aircraft are expensive, fuel prices are volatile, and demand can collapse suddenly—as seen during COVID-19 or in response to geopolitical shocks. Even in “normal” years, margins are thin.

According to IATA’s assessment for 2024:

-

The global airline industry generated a net profit of about USD 32.4 billion.

-

Spread across all passengers, that equates to around USD 6.8 of net profit per passenger per flight.

At the same time, governments collected:

-

Around USD 60.4 billion in specific taxes on air passenger tickets in 2024 alone.

-

That corresponds to about USD 29.5 in specific ticket taxes per round trip, or USD 12.6 per flight segment on average.

Put simply, governments earned almost twice as much from these specific ticket taxes as airlines earned in net profit. For each passenger, the tax take per flight is almost double the airline’s net earnings.

And this only covers specific ticket taxes—it does not include:

-

Airport charges,

-

Air navigation fees,

-

Fuel excise duties where they exist,

-

VAT or other general consumption taxes on tickets,

-

Corporate income taxes on airline profits.

Those are separate layers. The focus here is on one slice of the fiscal burden: fixed, per-passenger taxes that apply simply because someone flies.

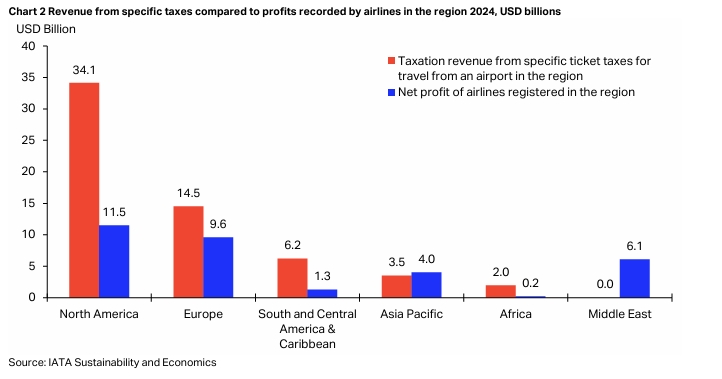

2. Where the Money Goes: Taxes vs Profits by Region

Globally, specific air ticket taxes are distributed unevenly. Some regions rely heavily on them; others barely use them.

IATA’s breakdown of 2024 specific tax revenue shows that:

-

North America collected about USD 34.1 billion, roughly 57% of the global total, even though it accounted for only about 24% of global passengers.

-

Europe collected around USD 14.5 billion, about 24% of global specific tax revenue.

-

South and Central America & the Caribbean collected approximately USD 6.2 billion (about 10% of the total).

-

Asia Pacific collected about USD 3.5 billion, and Africa around USD 2.0 billion.

When these figures are compared with the net profits of airlines registered in each region, IATA’s analysis shows a stark reality:

-

In some regions, revenue from specific air ticket taxes exceeds or closely matches the net profit generated by airlines based there.

-

In others, tax revenue is still a significant fraction of regional airline profits, effectively siphoning away much of the sector’s earnings.

In other words, governments often take more from air travel, through specific ticket taxes alone, than airlines themselves keep in profit—after bearing all the operating and financial risk.

3. Passenger-Level Reality: More Tax Than Profit in Your Ticket

It is one thing to talk about billions at a global or regional level; it is another to consider the numbers at the individual ticket level.

For a typical flight:

-

The airline’s net profit per passenger per segment is roughly USD 6.8.

-

The average specific tax per passenger per segment is about USD 12.6.

That means that, on average, the government’s take from a specific ticket tax is almost twice the profit that the airline earns on that same passenger on that same flight.

On some routes or in some countries, the gap is far larger. Using IATA’s 2024 country figures (excluding VAT, fuel excise and airport taxes):

-

Argentina collected USD 137.8 in specific taxes per departing passenger.

-

Mauritius collected about USD 63.8.

-

The United Kingdom collected an average of USD 36.9, the United States USD 29.3, and Egypt USD 28.3.

-

By contrast, Japan collected only USD 1.8, and China virtually zero (around USD 0.1).

When a single departure tax can exceed USD 100, while global average airline profit is less than USD 7 per flight segment, it becomes clear that in some markets the tax per passenger dwarfs the profit per passenger.

4. How Taxes Shape Route Economics

Airlines do not decide to fly routes on the basis of sentiment; they do it on the basis of expected profitability. When specific ticket taxes are high, they directly influence that calculation.

Here’s how:

-

Higher All-In Price, Lower Demand

Specific ticket taxes are usually fixed amounts, not percentages. This has two important consequences:-

They make up a larger share of the final price on low-fare routes (such as short-haul or leisure markets),

-

They raise the minimum viable ticket price—below a certain level the airline simply cannot sell tickets without losing money.

When the all-in fare rises, some passengers decide not to travel, travel less often, or switch to alternative destinations. That reduces load factors and yields.

-

-

Route Viability and Frequency Decisions

Many routes operate on thin margins, especially outside large trunk markets. When taxes increase:-

Airlines may reduce frequencies, making schedules less attractive.

-

If profitability falls too far, they may withdraw completely, leaving a destination with fewer or no direct connections.

For tourism-dependent or remote regions, this is not a theoretical risk—it can mean fewer visitors, less investment, and higher costs for residents.

-

-

Capacity and Fleet Deployment

Airlines allocate aircraft to markets where the risk-adjusted return is most attractive. High specific taxes in one jurisdiction make lower-tax competitors more appealing for capacity deployment. This can shift growth away from high-tax markets. -

Ancillary Revenue and Yield Management

When taxes eat into margin, airlines may respond by:-

Increasing ancillary fees (baggage, seats, onboard services),

-

Adjusting fare families and price points,

-

Introducing or expanding premium products where margins are higher.

But there is a limit to how much can be passed on before demand erodes.

-

In short, specific ticket taxes change the economic map of aviation. They constrain what routes are viable, how often aircraft can be deployed, and how much connectivity a region enjoys.

5. Systemic Risks: When a “Cash Cow” Becomes a Weak Link

From a finance ministry’s perspective, specific air travel taxes can look like an attractive “cash cow”:

-

Collection is efficient (airlines remit the taxes),

-

A large portion may be paid by non-residents (tourists),

-

The base is visible and relatively easy to monitor.

But treating aviation as a simple revenue source creates a series of systemic risks.

a) Vulnerability to Shocks

Because air travel is cyclical and highly sensitive to economic conditions, these taxes are exposed to shocks:

-

A global recession, pandemic, or geopolitical event can dramatically reduce passenger numbers, collapsing ticket-tax revenue just when governments need money most.

-

High fixed taxes can worsen downturns, because they keep ticket prices elevated even as airlines try to discount to stimulate demand.

b) Eroding Competitiveness

When taxes push air travel costs above competitor destinations or hubs:

-

Airlines may divert capacity to more profitable markets,

-

Tourists and investors may choose alternative locations,

-

Local businesses face higher travel costs for reaching clients, suppliers, and investors.

Over time, this can erode a country’s position in tourism, trade, and investment, shrinking the overall tax base.

c) Weakening Airline Balance Sheets

High specific ticket taxes squeeze airline margins. Weaker balance sheets mean:

-

Less capacity to invest in newer, greener aircraft,

-

Reduced resilience to absorb external shocks,

-

Higher risk of restructuring or outright bankruptcy.

When a major carrier fails or downsizes, the economic costs—lost jobs, lost connectivity, stranded passengers—can far outstrip the revenue once collected through ticket taxes.

6. The Equity Dimension: Who Really Bears the Burden?

Although specific air travel taxes are often perceived as targeting airlines or “wealthy travellers,” the economic incidence is more subtle.

a) Passengers vs Airlines

In competitive markets, airlines can only pass on so much cost before demand drops. In practice:

-

A large portion of specific ticket taxes is borne by passengers, through higher fares and reduced service;

-

A portion is borne by airlines, in the form of reduced margins and fewer profitable opportunities.

Which side bears more depends on factors like competition, elasticity of demand, and available substitutes (including alternative destinations).

b) Low-Income Travellers and Diaspora Communities

Fixed per-passenger taxes are regressive:

-

A USD 30 tax is negligible for a high-income traveller, but significant for a low-income worker or student.

-

Diaspora communities making frequent trips home are particularly affected. Even if headline fares are low, taxes can make travel financially difficult.

In regions where air travel is the only practical mode of international transport, high ticket taxes can become a de facto tax on mobility and opportunity.

c) Business and Public Sector Travellers

Companies and governments also pay more when taxes are high:

-

Business travel budgets must stretch to cover higher ticket costs, potentially limiting market development, trade missions, or professional exchanges.

-

Public sector entities (e.g., health, education, diplomacy) pay more for travel required to deliver their mandates.

Ultimately, these costs are absorbed into prices, public budgets, and service levels—again, affecting citizens and taxpayers.

7. Environmental Claims: Are High Ticket Taxes a Climate Tool?

Some governments justify high or rising air travel taxes by arguing that they help address climate change. The logic is that:

-

Higher ticket prices reduce demand, thus lowering emissions;

-

Revenue can be used to fund environmental programmes.

However, many specific ticket taxes are not directly linked to emissions:

-

They are charged per passenger, not per tonne of CO₂;

-

There is often no automatic connection between tax level and environmental performance (e.g., flying on a newer, more efficient aircraft does not reduce the tax);

-

Revenues are frequently not earmarked for climate or sustainability projects.

At the same time, international frameworks such as CORSIA (for international flights) already aim to address aviation’s climate impact through market-based measures.

If climate policy is the objective, well-designed carbon pricing mechanisms and support for sustainable aviation fuel and efficiency improvements are generally more effective than blunt, flat ticket taxes that primarily function as revenue tools.

8. Towards a More Balanced Framework

None of this implies that aviation should be tax-free. Airlines use public infrastructure, benefit from regulatory frameworks, and operate in societies that need public revenue. The question is how to design aviation taxation in a way that balances:

-

Revenue needs,

-

Economic efficiency,

-

Equity, and

-

Environmental objectives.

Some principles that emerge from the data and experience include:

-

Awareness of the Tax-to-Profit Ratio

Policymakers should pay close attention to how specific ticket taxes compare to airline profits—globally, by region, and on key routes. When taxes systematically exceed profits, the risk of damaging connectivity is high. -

Moderation and Predictability

Sudden, large increases in ticket taxes can destabilise route planning and investment. Moderate, predictable changes—ideally accompanied by impact studies—are less damaging. -

Broad-Based vs Narrow Taxes

From a public finance perspective, broad-based taxes (like VAT or income tax) are typically more efficient and less distortionary than narrow sector-specific taxes. Where possible, governments should lean more on broad bases and use specific ticket taxes sparingly. -

Simplification and Transparency

Consolidating multiple small taxes into a single, clearly labelled charge can reduce compliance costs and increase public understanding. Transparency helps passengers see where their money goes. -

Targeted Relief and Incentives

Well-designed schemes can:-

Provide temporary relief to stimulate recovery after shocks,

-

Support new routes into underserved or strategic markets,

-

Encourage investment in greener aircraft or sustainable fuels.

-

-

Alignment with Aviation and Tourism Strategies

Aviation tax policy should not be developed in isolation. It must align with tourism promotion, trade facilitation, regional integration, and climate strategies. Otherwise, one policy arm can unknowingly undermine another.

9. What It Means for Governments, Airlines and Advisors

The imbalance between air ticket taxes and airline profits has far-reaching implications:

-

Governments risk over-taxing a sector that is critical for tourism, trade, and connectivity, and that already operates on thin margins.

-

Airlines face constrained profitability and reduced resilience, making it harder to invest in fleet renewal and sustainability.

-

Tourism agencies, airports and investors must factor fiscal regimes into their strategy for route development and destination marketing.

For advisory firms and policy analysts, this environment creates a clear agenda:

-

Model how changes in ticket taxes affect demand, airline viability, tax revenue, and wider economic activity;

-

Benchmark countries and regions against global best practice;

-

Support governments in designing data-driven, balanced aviation tax frameworks;

-

Help airlines and tourism stakeholders advocate effectively for reforms that protect both connectivity and fiscal sustainability.

When the Tax Tail Wags the Aviation Dog

The numbers from 2024 tell a simple but powerful story: specific taxes on air passenger tickets now exceed global airline net profits by a wide margin. On a per-passenger basis, the tax take per flight is almost double the profit.

In a sector as vital as aviation—linking people, goods and ideas across continents—this imbalance matters. When taxes outweigh profits, the risk is that the “cash cow” of air travel becomes too weak to pull the economic cart: routes disappear, investment stalls, and opportunities shrink.

A more balanced approach to aviation taxation does not mean abandoning public revenue. It means designing taxes that are proportionate, transparent, and aligned with broader economic and climate goals—so that governments, airlines, and passengers can all share in the value that air connectivity creates.

About Dawgen Global

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

✉️ Email: [email protected] 🌐 Visit: Dawgen Global Website

📞 📱 WhatsApp Global Number : +1 555-795-9071

📞 Caribbean Office: +1876-6655926 / 876-9293670/876-9265210 📲 WhatsApp Global: +1 5557959071

📞 USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements