The paradox of progress

Walk through a street market in Yangon, a minibus park in Kingston, or a craft village in St. George’s and you’ll see the same choreography—notes changing hands, coins in plastic tubs, a quick mental tally before the bag is tied. In many countries, cash still powers day-to-day life because it is simple, cheap, and trusted. Yet in other places—Oslo, Seoul, parts of Shanghai—bills and coins are edging toward relic status as instant, low-cost digital rails take over. The global map of “where people still use cash” is, in effect, a map of infrastructure, incentives, and institutional trust. And the Caribbean sits right at the hinge between worlds: cash-heavy in daily transactions, but poised for a safe and significant shift if we get the design—and the sequencing—right.

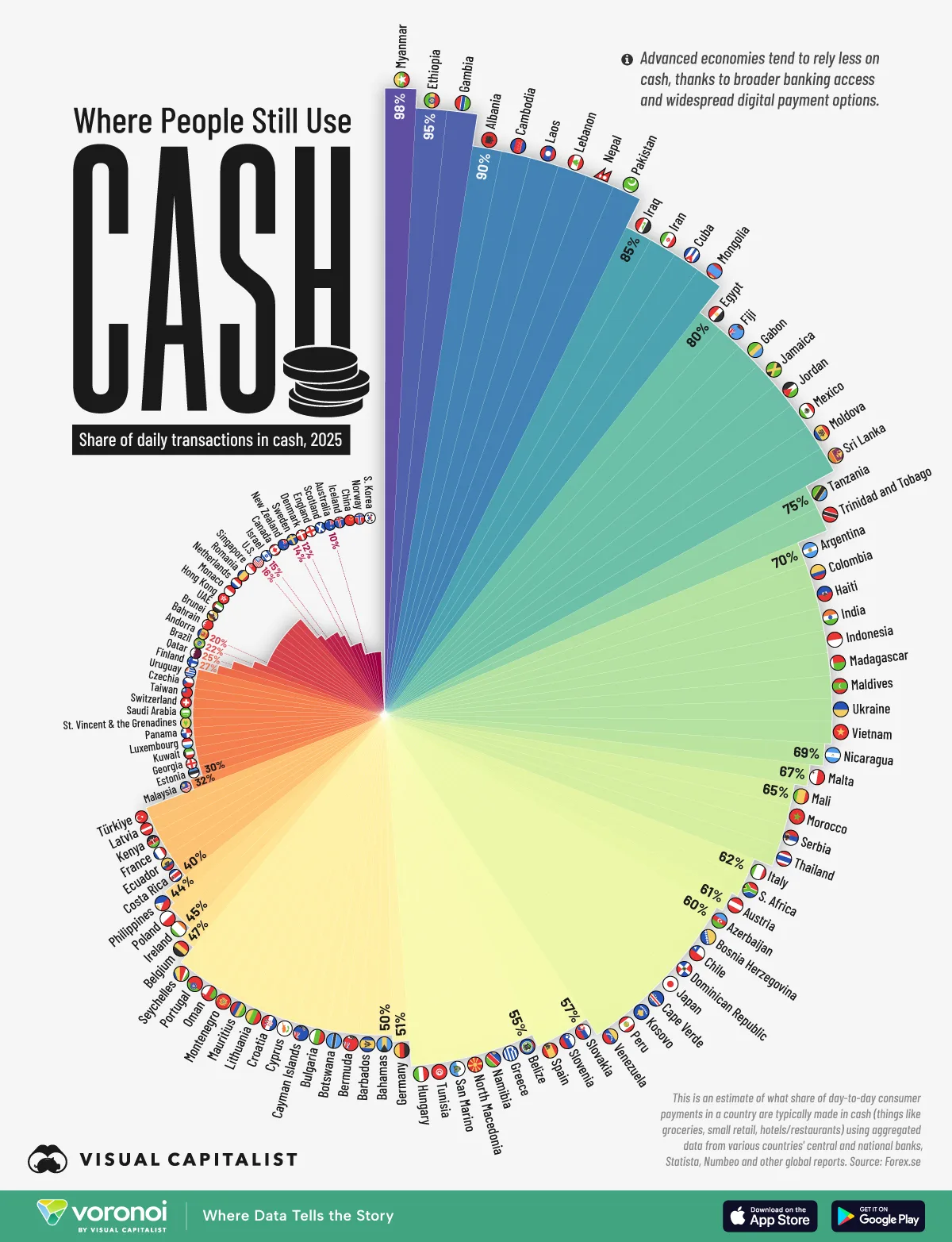

Reading the chart: two worlds on one wheel

The visual you’re seeing ranks 120+ countries by the share of daily consumer transactions completed in cash. At the cash-heavy end, Myanmar leads at roughly 98%, followed by a cluster—Ethiopia and Gambia around 95%, then Albania, Cambodia, Laos, Lebanon, and Nepal at about 90%. The pattern is clear: where the population is more likely to be unbanked, where broadband and smartphones are less pervasive, and where merchant terminals are expensive or impractical, cash remains the operating system.

At the other end are advanced economies with mature digital rails. Norway and South Korea are down near 10% cash share, and the United States sits in the mid-teens. Consumers there rely on ubiquitous connectivity, robust consumer protection, and instant settlement, while merchants enjoy lower shrinkage, faster funds availability, and fewer security risks.

Between these poles are outliers that complicate any simple story. Japan clocks in around 60% cash usage despite its technological prowess; Germany hovers near 51%, a standout among its European peers. Each reflects a blend of privacy preferences, cultural norms, and resilience thinking—a reminder that payment behavior is as social as it is technical.

About the data: The underlying index aggregates sources such as Statista, Numbeo, and national banks, among others, to estimate the share of day-to-day consumer payments done in cash (groceries, small retail, hotels/restaurants). The figures are approximate averages derived from a mix of public and industry reports.

Why cash persists: the “AFT” stack (Access, Friction, Trust)

1) Access: accounts, devices, and data

If you don’t have a bank account—or the documentation to open one—digital is out of reach. Even with an account, limited smartphone ownership, expensive data, and patchy broadband can push people back to cash. This is especially true for rural communities, the self-employed, and informally employed workers. Access gaps are not just about technology; they include identity (can you pass KYC without a utility bill?), geography (how far is the nearest agent or ATM?), and cash-out liquidity (can you convert digital balances back to cash without a long trip and a fee?).

2) Friction: the merchant math

Merchants live by margins. Card acceptance can mean merchant discount rates (MDRs), terminal rental or purchase costs, settlement delays, and chargeback risk. For a street vendor selling low-ticket items, a 2–3% fee plus settlement tomorrow may feel far worse than a few minutes of end-of-day cash counting. If the alternative is free QR with instant settlement and no hardware, digital starts to look better. But where that bundle isn’t available—or isn’t reliably available—cash wins the tie.

3) Trust: privacy, predictability, and resilience

People trust what they can hold, tally, and spend in a blackout. Cash is offline by design. Where outages are common, disaster risk is real, or dispute processes for digital payments are opaque, notes and coins feel safer. Cultural norms and privacy preferences matter, too. In Germany and Japan, high cash usage coexists with world-class infrastructure because citizens like the control and anonymity cash affords.

Why cash recedes: when rails + rules + reasons align

Ubiquitous, affordable connectivity

When most consumers carry a smartphone and data is cheap, wallets and bank apps can ride on top of that layer.

Merchant-first economics

The inflection point arrives when a merchant can accept payments with a printed QR or tap-to-phone, pay close to zero in fees for small tickets, and get funds instantly.

Clear consumer protection

With transparent dispute processes, low error rates, and good UX, consumers gain confidence. Add loyalty, cash-back, or bill discounts, and behavior begins to shift.

Interoperable rails

When wallets, banks, and PSPs can all talk to each other (think UPI in India or PIX in Brazil), the whole market participates. Interoperability is the difference between a collection of walled gardens and a national network effect.

Comparative cases: lessons worth borrowing

India (UPI): public rails, private innovation

India’s Unified Payments Interface (UPI) created an open, instant, 24/7 rail that any licensed participant can plug into—banks, fintechs, super-apps. The result: explosive growth in P2P and P2M transactions with QR as the on-ramp for micro-merchants. Cash is still used widely—given the nation’s scale and diversity—but UPI shows that policy + interoperability + incentives can bend the curve.

Takeaway for small states: You don’t need to saturate a country with card terminals. You need interoperable QR, instant settlement, tiered e-KYC, and low fees for small tickets.

Norway & South Korea: coherent, consumer-safe ecosystems

These countries combine fast rails, broadband ubiquity, strong consumer protection, and merchant-friendly economics. They are examples of cash-lite environments achieved without sacrificing resilience: emergency cash access still exists, but everyday life flows digitally.

Takeaway for small states: The key is the bundle, not any single ingredient. Try to move all levers together—rails, rules, and reasons—rather than piloting one shiny tool at a time.

Japan & Germany: the privacy/resilience outliers

Despite advanced infrastructure, both remain cash-comfortable. Privacy norms, aged demographics, and disaster-planning mindsets all reinforce cash habits.

Takeaway for small states: Don’t frame “cash-lite” as a victory lap. Frame it as choice expansion—digital when it’s better, cash when it’s needed.

Caribbean Spotlight: everyday transactions, real-world frictions

Across the Caribbean, the visualization shows elevated daily cash usage relative to cash-lite economies. Reading directly from the chart:

Jamaica – around 80% of day-to-day transactions in cash

Trinidad & Tobago – roughly 75%

Haiti – about 70%

Dominican Republic – near 60%

Bahamas – approximately 51%

Barbados – approximately 50%

(Additional islands visible on the chart—such as St. Lucia, St. Vincent & the Grenadines, Grenada—also sit in the higher-cash arc.

Field notes from the region

Tourism corridors (hotels, restaurants, attractions) are increasingly card- and wallet-friendly, but tips, street food, market produce, and minibus/taxi fares remain primarily cash.

Micro-merchants face a classic cost trap: card terminals are expensive and risky at low volume; bank settlement is slow; dispute processes are confusing; and smartphone/data costs still pinch.

Remittances—often double-digit % of GDP—arrive through cash pickup or to accounts/wallets that must be cashed out for everyday spend unless merchant acceptance is widespread.

What this means

The Caribbean isn’t “behind”—it’s practical. Households and MSMEs balance certainty (cash today) with convenience (digital where it’s reliable and cheap). A responsible shift requires better economics, clearer protections, and offline-capable resilience.

The merchant decision: a day in the till

Imagine a beach vendor taking 40 payments of US$5 equivalent.

All-cash day

Fees: $0

Risks: theft/shrinkage; no receipt trail; end-of-day bank run; counterfeit detection burden

Liquidity: immediate, but manual and risky

QR + instant settlement day (low or zero MDR for small tickets; no terminal)

Fees: near-zero on small transactions (varies by scheme)

Risks: fewer theft losses; digital trail helps reconcile; chargeback exposure depends on scheme rules

Liquidity: T+0 into wallet/bank, available to restock without traveling

What flips the choice?

Hardware-free acceptance (printed QR / tap-to-phone)

Instant settlement with small-ticket fee caps

Dispute clarity (simple, fast, predictable)

Agent cash-out nearby for those who still need physical float

The inclusion stack: how people actually get on the rail

Digital ID / tiered e-KYC

Let low-risk users open low-limit accounts with minimal documentation.

Expand limits with additional proof over time.

Interoperable QR

Make the same code work across wallets, banks, and PSPs.

Ensure offline-capable acceptance (pre-signed tokens, queued transactions).

Instant, low-cost rails

Guarantee T+0 merchant settlement for small tickets and low MDR bands.

Remittance integration

Route inbound flows directly into wallets/bank apps with bill-pay and merchant pay built in.

Consumer protection and education

Transparent chargeback windows, scam alerts, and a plain-language rights charter.

Merchant and consumer onboarding that fits literacy and language realities.

Resilience by design: hurricanes, blackouts, and fail-gracefully systems

A Caribbean payments strategy has to assume power and connectivity interruptions. The goal is not “digital only,” but cash-resilient digitization:

Offline acceptance modes (QR tokens/NFC/USSD) with risk-managed caps and automatic sync when networks return.

Dual-path connectivity (primary + backup) for larger merchants; battery banks for critical retail.

Agent network liquidity rules for emergency cash-out windows.

Disaster fee caps and clear contingency playbooks published by regulators and PSPs.

Resilience doesn’t reduce digital ambition; it earns it.

Policy and industry playbook: five levers to move 10–20 points off cash—safely

Make QR the default for MSMEs

National spec + interoperability from day one; no proprietary walled gardens.

Tap-to-phone enabled for any NFC-capable Android/iOS device.

Guarantee instant settlement for small tickets

T+0 into merchant accounts/wallets up to a daily cap; settlement certainty is the adoption engine.

Compress fees at the bottom of the pyramid

Micro-MDR tiers (e.g., ≤1% or fixed micro-fee) for transactions under a threshold; promote free P2P.

Scale tiered e-KYC with digital ID

Remove the “no utility bill, no account” trap; let capability grow with risk-based limits.

Incentivize the first 90 days

Bill credits for using digital pay, government-to-person (G2P) and government-to-business (G2B) payments on the same rail, and merchant onboarding bundles (QR kit + signage + training).

Risks & safeguards: build trust as you build rails

Fraud & social engineering: Require in-app name/amount verification, one-tap scam warnings, and cool-off periods for first-time high-value payments.

Chargebacks & disputes: Publish simple SLAs; provide merchant relief for clear-cut cases; use risk-based liability models.

Data privacy: Adopt privacy-by-design defaults; minimize data collected; give users control over history.

Exclusion risk: Keep cash, agents, and assisted service in the loop; design for low literacy and feature phone users.

Vendor lock-in: Prefer open standards and APIs; prevent single-vendor dependence at national scale.

What to watch (12–24 months)

Merchant acceptance density: QR/tap-to-phone per square kilometer and per 1,000 residents.

Instant-settlement adoption: Share of merchant transactions settled T+0.

Wallet-to-merchant (P2M) share: Digital share of small-ticket spend in markets and transit.

Inbound remittance digitization: % of remittances landing in spend-ready wallets/accounts.

Resilience drills: Results of regulator-led outage simulations and offline-mode performance.

Caribbean call-to-action: practical next steps for 2025

Regulators: Publish an interoperable QR standard and a tiered e-KYC policy note; run a public sandbox focused on offline modes and instant settlement.

Banks & PSPs: Roll out tap-to-phone and printable QR kits with signage; compress fees for sub-$10 tickets; offer merchant settlement T+0 by default.

Telcos & Utilities: Co-market data-light wallet bundles; provide bill-pay discounts for digital.

Large retailers & transit: Seed acceptance density; trial request-to-pay links and transit QR to normalize usage.

Tourism boards & hotel groups: Digitize tips, excursions, and craft markets with interoperable QR + agent cash-out options.

Closing thought: choice, not dogma

The future isn’t cashless so much as cash-resilient and confidence-rich. People will keep using cash where it works better—and they should have that option. But with the right rails, rules, and reasons, the Caribbean can unlock the benefits of digital—faster settlement, lower risk, broader inclusion—without sacrificing the reliability that cash provides in tough moments. That’s the transition from notes to nodes: expanding choices, strengthening trust, and letting money move at the speed of real life.

Caribbean Spotlight

Cash in Daily Life (from the chart):

Jamaica ~80% | Trinidad & Tobago ~75% | Haiti ~70% | Dominican Republic ~60% | Bahamas ~51% | Barbados ~50%

Did you know? In many islands, minibus fares, market produce, and tips remain predominantly cash—three high-frequency categories that shape habits more than any single large purchase.

Inclusion lever to pilot next: Interoperable QR + instant settlement for small tickets with tiered e-KYC—no terminal required, print-and-go acceptance.

Resilience note: Prioritize offline-capable acceptance with risk-managed limits for hurricane season; publish outage playbooks so merchants know exactly how to operate.

Work with Dawgen Global

Want a pragmatic roadmap for moving 10–20 points off cash—safely?

Book a 30-minute payments strategy consult.

Request our Merchant Acceptance Calculator and Payments Resilience Checklist for the Caribbean.

What global cash dominance tells us—and the Caribbean’s path to “cash-lite.”

About Dawgen Global

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

✉️ Email: [email protected] 🌐 Visit: Dawgen Global Website

📞 📱 WhatsApp Global Number : +1 555-795-9071

📞 Caribbean Office: +1876-6655926 / 876-9293670/876-9265210 📲 WhatsApp Global: +1 5557959071

📞 USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements