The Loneliest Job in Governance

The Chief Audit Executive occupies one of the most unusual positions in any organisation. They must be close enough to management to understand the business deeply, yet independent enough to challenge management fearlessly. They must be trusted by the Board as an objective voice, yet respected by operational leaders as a collaborative partner. They must deliver difficult messages without making enemies, advocate for investment without appearing self-serving, and maintain absolute integrity while navigating the most politically complex terrain in the organisation.

It is, by almost any measure, the loneliest job in governance. And yet it is also one of the most consequential. The CAE who masters this role – who learns to lead strategically rather than merely manage technically – transforms not just the Internal Audit function but the governance culture of the entire organisation. The CAE who does not master it remains a competent administrator producing reports that land on desks but never change decisions.

In the previous five articles of this series, we explored the IAVANTAGE™ Framework’s architecture: the maturity model, the seven pillars, the business case, and the technology roadmap. In this article, we turn to the human element that makes everything else possible: the leadership of the Chief Audit Executive.

| “Every dimension of the IAVANTAGE™ Framework depends ultimately on one person’s ability to lead: the CAE. Technology, methodology, and structure are necessary but not sufficient. Without a CAE who can build trust, communicate vision, and navigate complexity, even the best framework remains paper.” — Dawgen Global |

The Three Pillars of CAE Strategic Leadership

Based on our work with Chief Audit Executives across the Caribbean, Latin America, and international markets, Dawgen Global has identified three foundational pillars that distinguish transformational CAEs from competent administrators. These are not technical audit competencies – they are leadership capabilities that determine whether a CAE can convert the IAVANTAGE™ Framework from aspiration into reality.

LEADERSHIP PILLAR 1: INFLUENCE |

The ability to shape decisions, secure resources, and drive change without positional authority

The CAE has remarkably little formal power. Unlike the CFO who controls budgets or the COO who controls operations, the CAE controls nothing except the quality and relevance of their own team’s work. Everything the CAE achieves beyond completing the audit plan – every strategic conversation, every transformation initiative, every additional resource – depends on influence.

Influence for a CAE is built through five mechanisms. The first is credibility through consistent quality. Every audit report, every presentation, every interaction either builds or erodes the CAE’s credibility. The CAE who delivers consistently high-quality, relevant, and actionable work creates a reservoir of credibility that can be drawn upon when advocating for change.

The second mechanism is strategic relevance. The CAE who understands the business – not just its controls but its strategy, its competitive pressures, its growth ambitions, and its vulnerabilities – earns a fundamentally different kind of respect. Strategic relevance means the CAE can contribute to conversations about market entry, digital transformation, or organisational restructuring in ways that go beyond “have you considered the risks?” to “here is how I think we can manage the risks while achieving the strategic objective.”

The third is relational investment. Influence is built one relationship at a time. The CAE must invest deliberately in understanding what each key stakeholder needs, values, and worries about. The Audit Committee Chair has different concerns from the CEO. The CFO has different priorities from the CRO. The CAE who takes the time to understand these differences – and who tailors their communication accordingly – builds a network of allies who support the function because they have experienced its value.

The fourth mechanism is the courage to speak truth. Influence is not the same as popularity. The CAE who avoids difficult conversations, who softens findings to avoid confrontation, or who tells the Board what it wants to hear rather than what it needs to hear is not building influence – they are building irrelevance. True influence comes from being known as someone who will always tell the truth, even when the truth is uncomfortable.

The fifth is visibility and presence. The CAE must be visible to the organisation’s leaders – not just during audit engagements but throughout the year. Attending leadership meetings, participating in strategic forums, contributing to industry events, and being available for informal conversations all create the presence that sustains influence.

LEADERSHIP PILLAR 2: INDEPENDENCE |

Maintaining objectivity while building relationships – the essential paradox of the CAE role

Independence is the defining characteristic of Internal Audit’s value proposition. Without independence, the function is merely an extension of management – and the Board has no basis for relying on its assessments. Yet independence is also the most misunderstood concept in the profession. Too many CAEs interpret independence as distance, formality, or even antagonism. This is a fundamental error.

True independence is not about avoiding relationships with management. It is about maintaining objectivity within those relationships. A CAE can have an excellent, collaborative, mutually respectful relationship with the CEO and still deliver a finding that the CEO disagrees with. The key is not separation but integrity – the demonstrated willingness to call things as they are, regardless of the relational consequences.

The structural foundations of independence are well-established in professional standards: functional reporting to the Audit Committee, private access to the Board without management present, Board approval of the audit plan and budget, and dual reporting for administrative matters. These structures are necessary but not sufficient. The CAE can have every structural safeguard in place and still compromise independence through self-censorship, finding avoidance, or scope limitation driven by fear of management reaction.

The practical test of independence is simple: In the past twelve months, has the CAE delivered a finding or opinion that management strongly disagreed with? If the answer is no, either the organisation has no significant control weaknesses – which is improbable – or the CAE is not exercising genuine independence.

| “Independence is not a structural arrangement. It is a daily practice. It is the choice, made repeatedly, to say what needs to be said even when the audience does not want to hear it. The CAE who makes this choice consistently earns something no organisational chart can provide: the Board’s unqualified trust.” — Dawgen Global |

LEADERSHIP PILLAR 3: IMPACT |

Delivering measurable results that change organisational outcomes and justify continued investment

Influence secures the seat at the table. Independence ensures the voice is trusted. Impact ensures the function remains there. Without demonstrable impact, even the most influential and independent CAE will eventually face the question: “What exactly are we getting for this investment?”

Impact-oriented CAEs think differently about every aspect of the audit function’s work. They do not measure success by audit completion rates or finding counts. They measure success by outcomes: risks that were prevented, costs that were saved, decisions that were improved, confidence that was strengthened. They ask, after every engagement, “What changed because of our work?” If the answer is “nothing”, then the engagement did not deliver its potential value.

Delivering impact requires three disciplines. First, outcome-oriented planning: every engagement should have a defined expected outcome – not just “complete the audit of Process X” but “provide assurance on the effectiveness of controls in Process X and identify at least two actionable improvement opportunities.” Second, follow-through rigour: findings that are issued but never implemented have zero impact. The CAE must build robust follow-up mechanisms and escalation protocols. Third, value communication: as explored in Article 4, the CAE must systematically measure, record, and communicate the tangible value that Internal Audit delivers.

The IAVANTAGE™ CAE Competency Model

Building on these three leadership pillars, Dawgen Global has developed a comprehensive competency model for the strategic CAE. This model defines seven competency domains that together represent the complete profile of a transformational Internal Audit leader.

| COMPETENCY | LEADERSHIP PILLAR | WHAT THIS LOOKS LIKE IN PRACTICE |

| Strategic Thinking | Influence + Impact | Connects audit work to business strategy. Anticipates how organisational changes will affect the risk landscape. Contributes to strategic conversations with insight rather than just caution. |

| Executive Communication | Influence | Presents complex risk information with clarity and impact. Adapts messaging for different audiences. Uses data visualisation and storytelling to make audit insights memorable. |

| Stakeholder Management | Influence | Builds productive relationships with all key stakeholders. Understands priorities and concerns. Manages expectations proactively. Resolves conflicts constructively. |

| Ethical Courage | Independence | Delivers difficult messages with clarity and conviction. Resists pressure to modify findings or limit scope. Escalates concerns through appropriate channels without hesitation. |

| Change Leadership | Impact | Develops and executes the transformation roadmap. Builds team capability. Manages resistance. Maintains momentum through organisational challenges. |

| Technical Excellence | Impact | Maintains deep expertise in audit methodology, risk assessment, and governance. Stays current on emerging technologies and regulatory developments. Sets quality standards. |

| Talent Development | Influence + Impact | Recruits, develops, and retains high-calibre professionals. Creates career pathways. Builds a team culture of excellence, innovation, and continuous learning. |

The Five Conversations Every CAE Must Master

Strategic leadership for a CAE is ultimately expressed through conversations. The ability to have the right conversation, with the right person, at the right time, in the right way is the skill that separates transformational CAEs from the rest.

- The Board Conversation: “What Should Keep You Awake?”

The CAE’s most important audience is the Audit Committee. The Board conversation should be strategic, forward-looking, and candid. The most effective CAEs use their private sessions with the Audit Committee Chair to share perspectives on the organisation’s risk culture, the quality of management’s risk management, and the emerging threats that are not yet on the formal risk register.

- The CEO Conversation: “How Can I Help You Succeed?”

The relationship with the CEO is often the most delicate. The most effective approach is to position Internal Audit as a resource that helps the CEO achieve their objectives – by identifying risks that could derail strategic initiatives, providing assurance that major programmes are on track, and offering advisory perspectives that strengthen decision-making. The CAE who begins every CEO interaction by asking “What are you most concerned about right now?” creates a dynamic where audit relevance is built into the relationship.

- The CFO Conversation: “This Is Our Return on Your Investment”

As explored in Article 4, the CFO conversation is fundamentally about value. The CAE must be prepared to articulate the return on the organisation’s audit investment in financial terms. This is not a once-per-year budget discussion – it is an ongoing dialogue where the CAE regularly demonstrates tangible contributions. The Value Register is the essential tool for this conversation.

- The Management Conversation: “Let’s Solve This Together”

Operational managers are the CAE’s most frequent stakeholders and often the most resistant audience. Changing adversarial perceptions requires consistent, authentic collaboration. The most effective CAEs approach management conversations with genuine curiosity about the business, practical and proportionate recommendations, timely communication, and a willingness to listen as much as they speak. When management starts coming to Internal Audit voluntarily – seeking advice before problems occur rather than defending themselves after findings are issued – the relationship has been transformed.

- The Team Conversation: “This Is Where We’re Going and Why It Matters”

The CAE’s internal conversation with the audit team is often the most neglected. Yet the team’s alignment, motivation, and capability directly determine the function’s impact. Transformational CAEs invest significant time in communicating vision, explaining strategy, celebrating achievements, developing talent, and building a culture of professional pride. The team that understands why they are transforming – not just what they are doing differently – is the team that sustains momentum through the inevitable challenges of change.

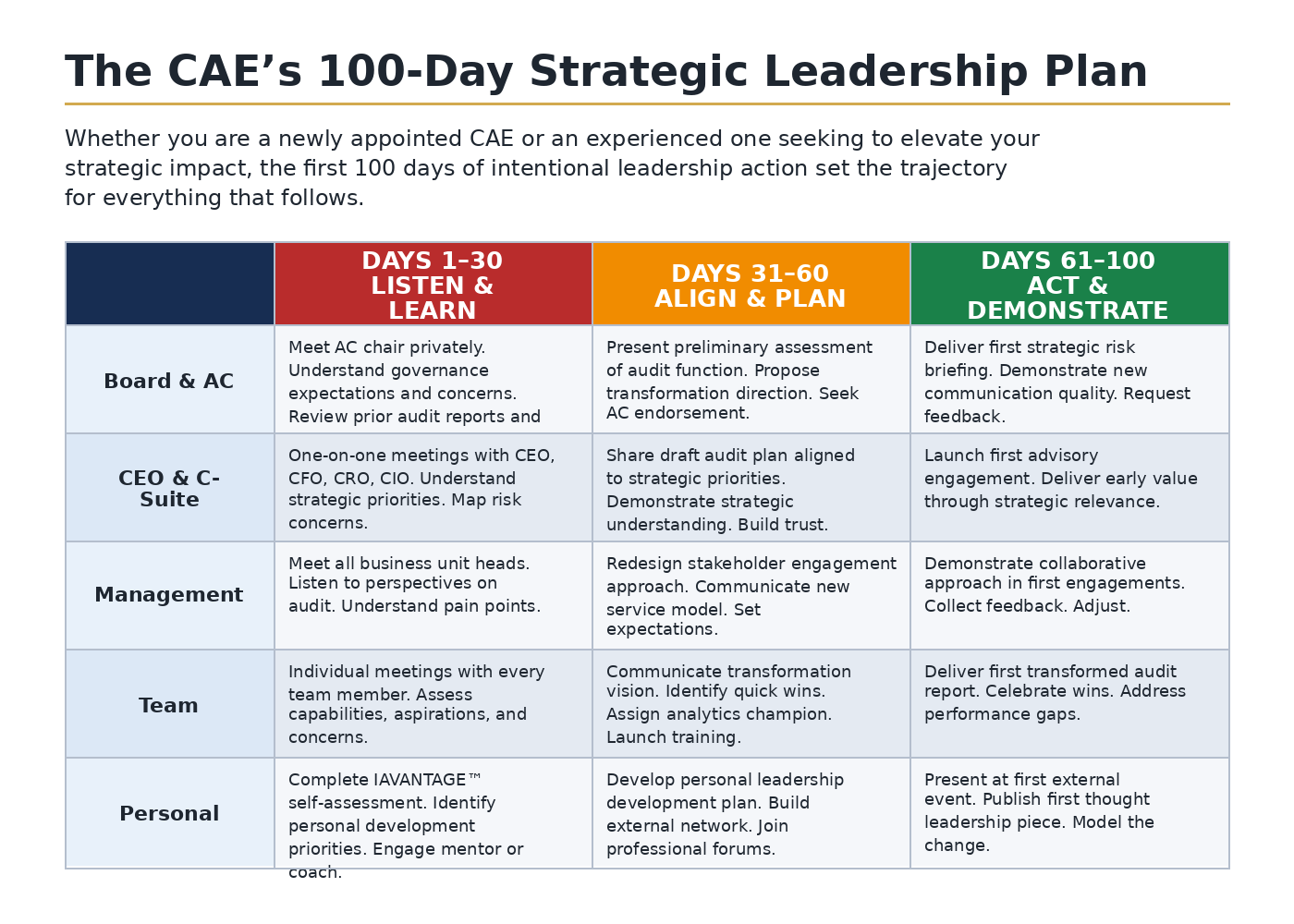

The CAE’s 100-Day Strategic Leadership Plan

Whether you are a newly appointed CAE or an experienced one seeking to elevate your strategic impact, the first 100 days of intentional leadership action set the trajectory for everything that follows.

| DAYS 1–30 LISTEN & LEARN | DAYS 31–60 ALIGN & PLAN | DAYS 61–100 ACT & DEMONSTRATE | |

| Board & AC | Meet AC Chair privately. Understand governance expectations and concerns. Review prior audit reports and AC minutes. | Present preliminary assessment of audit function. Propose transformation direction. Seek AC endorsement. | Deliver first strategic risk briefing. Demonstrate new communication quality. Request feedback. |

| CEO & C-Suite | One-on-one meetings with CEO, CFO, CRO, CIO. Understand strategic priorities. Map risk concerns. | Share draft audit plan aligned to strategic priorities. Demonstrate strategic understanding. Build trust. | Launch first advisory engagement. Deliver early value through strategic relevance. |

| Management | Meet all business unit heads. Listen to perspectives on audit. Understand pain points. | Redesign stakeholder engagement approach. Communicate new service model. Set expectations. | Demonstrate collaborative approach in first engagements. Collect feedback. Adjust. |

| Team | Individual meetings with every team member. Assess capabilities, aspirations, and concerns. | Communicate transformation vision. Identify quick wins. Assign analytics champion. Launch training. | Deliver first transformed audit report. Celebrate wins. Address performance gaps. |

| Personal | Complete IAVANTAGE™ self-assessment. Identify personal development priorities. Engage mentor or coach. | Develop personal leadership development plan. Build external network. Join professional forums. | Present at first external event. Publish first thought leadership piece. Model the change. |

The Independence Stress Test: Eight Questions Every CAE Should Answer

The following questions are designed as a practical self-assessment of your independence posture. Answer each honestly. If you answer “no” to three or more, your independence may be compromised in ways that undermine your function’s credibility and value.

- Have you delivered a finding in the past 12 months that the CEO or a senior executive strongly disagreed with – and maintained it?

- Do you have unrestricted private access to the Audit Committee Chair, and have you used it at least quarterly?

- Is your annual performance assessment conducted or approved by the Audit Committee, not solely by management?

- Have you declined a management request to limit audit scope or modify a finding in the past year?

- Can you add or remove engagements from the audit plan without management veto?

- Is your audit budget approved by the Board or Audit Committee, not solely by management?

- Have you reported an impairment to your independence or objectivity to the Audit Committee when it occurred?

- Would your team members honestly tell you they feel free to report findings without fear of management retaliation?

If this self-assessment reveals gaps, the response should not be defensive. It should be constructive. Every independence gap is a conversation waiting to happen with your Audit Committee Chair – and most Audit Committee Chairs, when informed of structural independence weaknesses, will support the CAE in addressing them.

Invest in Your Leadership

Strategic leadership is not an innate talent – it is a developed capability. The most effective CAEs are those who invest deliberately in their own development, seek feedback, engage mentors and coaches, and continuously refine their approach.

YOUR NEXT STEPJoin the IAVANTAGE™ CAE Leadership Roundtable Dawgen Global is a multidisciplinary professional services firm delivering audit, assurance, risk advisory, tax, and business consulting services across the Caribbean, Latin America, and emerging markets. Our Audit & Assurance Services practice is recognized for its deep industry expertise, innovative methodologies, and commitment to helping organizations transform governance from a compliance obligation into a competitive advantage. Dawgen Global hosts a quarterly, invitation-only roundtable for Chief Audit Executives across the Caribbean and Latin America. Participants share challenges, benchmark practices, and develop their strategic leadership capabilities in a confidential, peer-supported environment. Each session is facilitated by a Dawgen Global Partner and includes a focused leadership development module. ↓ REQUEST YOUR INVITATION ↓ Email: info@@dawgen.global | Call: +1 (876) 926-5210 |

| CATCHING UP ON THE SERIES?

Articles 1–5 cover the Expectation Gap, Maturity Model, Seven Pillars, Business Case, and Technology Roadmap. Read all articles: www.dawgen.global |

Coming Next in the IAVANTAGE™ Series

Article 7: “Risk-Based Auditing Reimagined: From Static Plans to Dynamic Intelligence” – A comprehensive rethinking of how Internal Audit approaches risk assessment, audit planning, and resource allocation in a volatile world. With practical methodologies for building dynamic, intelligence-driven audit plans.

About Dawgen Global

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

Email: [email protected]

Email: [email protected]  Visit: Dawgen Global Website

Visit: Dawgen Global Website

WhatsApp Global Number : +1 555-795-9071

WhatsApp Global Number : +1 555-795-9071

Caribbean Office: +1876-6655926 / 876-9293670/876-9265210  WhatsApp Global: +1 5557959071

WhatsApp Global: +1 5557959071

USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements