Financial, Tax, Operational & Cyber Red Flags in Distribution and Manufacturing M&A

Most M&A regret does not come from price. It comes from what you didn’t see—or what you saw but didn’t quantify, document, or negotiate properly. In distribution/retail and manufacturing, the risk profile is unique: inventory integrity, margin leakage, supplier concentration, customer credit exposure, production yield variance, ERP controls, and cyber vulnerabilities can quickly turn an “attractive acquisition” into a working-capital trap.

This article introduces the DAWGEN DILIGENCE™ approach—an integrated, multidisciplinary framework that combines financial, tax, operational, and cyber diligence into one coherent view of value and risk. We also provide:

-

a practical red flags checklist tailored to distribution and manufacturing,

-

a clear method to translate findings into deal protections (price adjustments, earn-outs, warranties, indemnities),

-

a 90-day plan for diligence and first-phase integration, and

-

composite cases showing how issues typically surface and how they should be handled.

1) Why traditional due diligence fails in distribution and manufacturing

A common problem: diligence becomes a “financial statements review” and misses the operational mechanics that drive cash and margin.

Typical failure patterns

-

EBITDA looks good but cash conversion is poor because of stock, credit notes, rebates, or overdue AR.

-

Inventory is overstated (phantom stock, slow moving, wrong valuation) and the buyer pays for it.

-

Gross margin is distorted by inconsistent landed cost, rebates not accrued, or uncontrolled discounting.

-

Customer concentration exists but is not stress-tested for contract terms and switching risk.

-

Supplier relationships depend on informal arrangements and can change immediately post-acquisition.

-

Cyber/IT controls are weak (shared logins, no logs, minimal backup resilience) increasing breach risk and operational disruption.

In other words: you can “buy revenue” and still inherit a margin and cash-flow problem.

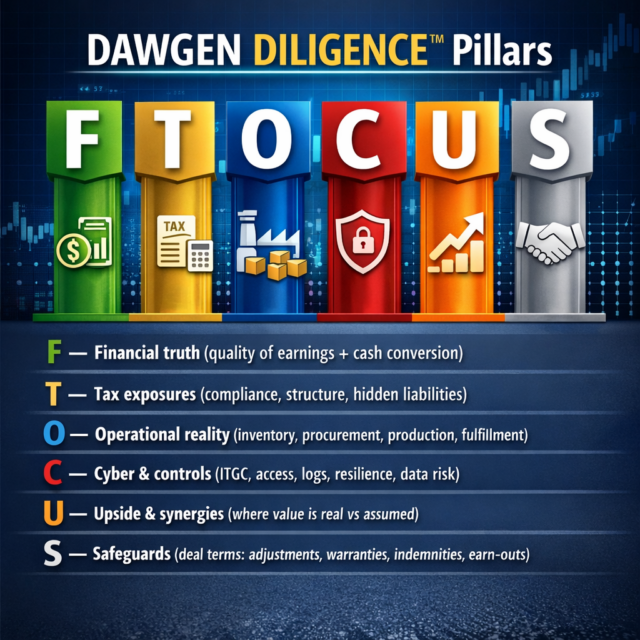

2) Introducing DAWGEN DILIGENCE™

DAWGEN DILIGENCE™ is designed to prevent buyer remorse by converting diligence into:

-

defensible valuation inputs (quality of earnings, cash conversion, normalised working capital), and

-

actionable deal protections (clauses and integration priorities).

DAWGEN DILIGENCE™ pillars

F — Financial truth (quality of earnings + cash conversion)

T — Tax exposures (compliance, structure, hidden liabilities)

O — Operational reality (inventory, procurement, production, fulfilment)

C — Cyber & controls (ITGC, access, logs, resilience, data risk)

U — Upside & synergies (where value is real vs assumed)

S — Safeguards (deal terms: adjustments, warranties, indemnities, earn-outs)

Think of it as FTOCUS™: focus on truth, then lock the deal safely.

3) What buyers should demand: the four truths

Truth #1: EBITDA quality (not just EBITDA size)

In distribution/manufacturing, EBITDA can be inflated by:

-

under-provisioning slow-moving inventory,

-

delaying write-offs,

-

treating supplier rebates inconsistently,

-

“capitalising” costs that should be expensed,

-

weak cut-off and credit note timing.

Dawgen method: build a Quality of Earnings (QoE) bridge:

-

Reported EBITDA

-

Less: one-offs and non-recurring items

-

Less: under-accrued expenses (rebates, provisions, maintenance, bonuses)

-

Add: sustainable adjustments

= Maintainable EBITDA

Truth #2: Working capital normalisation (the hidden price lever)

Many deals are lost or won at the working capital peg. A buyer can overpay if the target’s “normal” working capital is not properly defined.

Distribution red flags

-

AR ageing distorted by disputes and credit notes

-

Inventory levels not aligned to sales reality

-

AP stretched beyond terms (supplier pressure risk)

-

Frequent emergency buying and expedited freight

Manufacturing red flags

-

WIP valuation assumptions

-

Yield and scrap not measured consistently

-

Spare parts and consumables ballooning

-

Procurement terms and supplier dependency

Dawgen method: create a Normalised Working Capital model:

-

seasonality

-

SKU rationalisation potential

-

“true” receivable collectability

-

inventory ageing and valuation adjustments

-

supplier terms stability

Truth #3: Operational controls (where leakage lives)

A deal is fragile if core processes are not evidence-grade.

In distribution:

-

inventory receipts, transfers, returns, adjustments

-

pricing overrides and discounts

-

vendor master changes

-

rebate capture and credit note governance

In manufacturing:

-

production reporting (yield, scrap, downtime)

-

BOM integrity

-

overtime controls

-

maintenance backlog and reliability metrics

Truth #4: Cyber and IT resilience (a deal breaker in 2026)

Cyber diligence is no longer optional. It is tied to:

-

operational continuity

-

insurance eligibility

-

reputational risk

-

regulatory exposure (data privacy)

Minimum questions

-

Are there shared accounts? Is access reviewed?

-

Are logs kept and monitored?

-

Are backups tested?

-

Is there MFA?

-

Are endpoints protected?

-

Is there a history of incidents?

4) Red flags checklist (distribution and manufacturing)

A) Financial red flags

-

Heavy adjustments required to explain gross margin swings

-

Unreconciled inventory to GL or unexplained stock variances

-

Significant “management estimates” without policy discipline

-

Persistent negative operating cash flow despite EBITDA

-

Large related-party balances or “other receivables”

-

Aggressive revenue recognition or cut-off issues

-

Unusual year-end credits or rebates booked late

B) Tax red flags

-

Outstanding tax filings, assessments, or penalties

-

Weak documentation for tax positions and claims

-

Poor VAT/GCT treatment on imports, zero-rated items, or exemptions

-

Transfer pricing issues (if cross-border)

-

PAYE/Payroll compliance gaps

-

Unclear tax treatment of rebates, discounts, and returns

C) Operational red flags (distribution)

-

High adjustments with weak approval discipline

-

Phantom inventory / frequent stockouts despite “availability”

-

Weak cycle counting or counts done only for audit

-

High returns without classification and root cause

-

Vendor changes not independently verified

-

Discounting uncontrolled and not analysed by customer/product

-

Supplier concentration with informal arrangements

D) Operational red flags (manufacturing)

-

No reliable yield/scrap/downtime data (or inconsistent reporting)

-

BOM inaccuracies and uncontrolled substitutions

-

Overtime spikes without approvals and productivity measures

-

Maintenance underfunded leading to downtime risk

-

Quality issues creating rework and warranty exposure

-

Single-source critical inputs without contingency plan

E) Cyber & controls red flags

-

No MFA, shared passwords, weak role segregation

-

Limited logging and no monitoring

-

Backups not tested; ransomware exposure

-

Unsupported systems or unpatched environments

-

Vendor remote access unmanaged

-

No incident response plan or evidence preservation process

5) Translating diligence findings into deal protection

Good diligence is worthless if findings don’t flow into the deal.

The three levers

-

Price adjustment

-

Fix valuation for QoE adjustments, inventory write-downs, bad debts, tax exposures.

-

-

Working capital peg + true-up

-

Define “normal” working capital; adjust purchase price at closing for deviations.

-

-

Warranties, indemnities, and escrow

-

Protect against known risks and unknown unknowns.

-

When to use earn-outs

Use earn-outs when:

-

customer retention is uncertain,

-

margins depend heavily on management behaviour,

-

synergy assumptions are high and unproven.

But ensure earn-outs are not a substitute for fixing obvious issues (inventory and rebates must still be normalised).

6) Composite case study 1 — Distribution/retail (composite)

Situation: A buyer pursued a regional distributor because reported EBITDA and growth looked strong. The seller claimed “inventory is under control” and “customers are loyal.”

What Dawgen DILIGENCE™ uncovered:

-

high level of price overrides and discount leakage

-

supplier rebates inconsistently accrued (EBITDA inflated)

-

inventory ageing understated; write-down policy weak

-

AR ageing masked by credit notes and disputes

-

vendor master changes had weak controls

What changed in the deal:

-

purchase price adjusted for maintainable EBITDA

-

working capital peg tightened with a robust closing true-up

-

escrow introduced for inventory and tax exposures

-

post-close 90-day plan prioritised inventory integrity and discount governance

Lesson: Distribution deals fail when buyers pay for stock and margin that do not exist in reality.

7) Composite case study 2 — Manufacturing (composite)

Situation: A buyer targeted a manufacturer with strong sales and “high margin potential.” Operations claimed efficiency was improving.

What Dawgen DILIGENCE™ uncovered:

-

yield and scrap reporting not reliable; true cost per unit higher

-

overtime approvals inconsistent; labour cost drift

-

maintenance backlog creating downtime and fulfilment risk

-

BOM substitutions not properly controlled or valued

-

cyber posture weak (no MFA, poor backups, limited logging)

What changed in the deal:

-

valuation adjusted for true cost and operational risk

-

capex and maintenance plan incorporated into the investment case

-

integration plan included IT controls uplift and evidence-grade logging

Lesson: Manufacturing deals require operational truth and cyber resilience—not just revenue confidence.

8) A 90-day diligence-to-integration plan (practical execution)

Days 1–30: “Truth sprint” (before signing / before closing)

-

Quality of earnings bridge and working capital normalisation

-

Inventory and landed cost review (including ageing, rebates, adjustments)

-

Top 10 operational controls test (receiving, adjustments, approvals, pricing overrides)

-

Cyber baseline: MFA, backups, privileged access, log retention

-

Deal protections drafted to match findings

Outputs

-

QoE report + maintainable EBITDA

-

Normalised working capital peg recommendation

-

Red flags register with quantified impact

-

Deal protections matrix (what goes into price vs warranty vs escrow)

Days 31–60: Close planning + “Day 1 readiness”

-

confirm roles, access, banking controls, payment run governance

-

create integration control pack (SoD, approvals, audit trails)

-

design weekly dashboards for margin, stock accuracy, AR, and exceptions

-

confirm comms plan for suppliers and key customers

Outputs

-

Day 1 control pack

-

Integration KPI dashboard

-

Evidence map (where proof lives) aligned to forensic readiness

Days 61–90: Value capture and risk closure

-

execute inventory integrity uplift (cycle counts, variance root cause fixes)

-

implement pricing/discount governance

-

tighten collections cadence and credit policy

-

implement minimum cyber controls and monitoring

-

track synergy realisation with discipline (not optimism)

Outputs

-

90-day value capture report

-

Control exceptions reduced + remediation tracker

-

Board-ready integration status pack

9) What Dawgen Global delivers in M&A (multidisciplinary advantage)

Dawgen Global brings a unified approach that many deals lack:

-

financial diligence (QoE, working capital, cash conversion)

-

tax diligence and structuring

-

operational diligence (inventory, procurement, production controls)

-

cyber and controls assurance

-

forensic readiness (evidence-grade incident response, fraud risk)

-

integration governance (board dashboards, remediation tracking)

This is how you protect value and accelerate value capture.

Call to Action

If you are considering buying, selling, or merging a distribution/retail or manufacturing business, don’t rely on generic diligence. Use DAWGEN DILIGENCE™ to quantify risk, protect the deal, and build a 90-day integration plan that actually delivers value.

👉 Start here: https://www.dawgen.global/contact-us/

📧 [email protected]

📞 Caribbean: 876-9293670 | 876-9293870

📞 USA: 855-354-2447

WhatsApp Global: +1 555 795 9071

About Dawgen Global

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

Email: [email protected]

Email: [email protected]  Visit: Dawgen Global Website

Visit: Dawgen Global Website

WhatsApp Global Number : +1 555-795-9071

WhatsApp Global Number : +1 555-795-9071

Caribbean Office: +1876-6655926 / 876-9293670/876-9265210  WhatsApp Global: +1 5557959071

WhatsApp Global: +1 5557959071

USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements