A Different Kind of CFO Challenge

If you are a Chief Financial Officer in Kingston, Port of Spain, Bridgetown, Nassau, or Georgetown, you understand something that your counterparts in New York, London, and Toronto do not: the rules of working-capital management that are taught in business schools and published in Harvard Business Review are not written for your reality.

They are written for large enterprises operating in deep, liquid capital markets with stable currencies, diversified supplier bases, broad customer portfolios, and multiple layers of institutional credit. They assume that hedging instruments are readily available and affordable, that alternative suppliers can be sourced within weeks, that customer bases span thousands of accounts, and that central-bank policy is broadly predictable. These assumptions define a universe that the Caribbean CFO does not inhabit.

Your universe is different. It is characterised by small, open economies where a single government contract can represent 20 per cent of your revenue. By import dependency where 60 to 80 per cent of your input costs are denominated in a foreign currency that your central bank may or may not be able to defend. By credit markets where three commercial banks control 70 per cent of corporate lending and a single credit-committee decision can reshape your liquidity position overnight. By customer concentration where losing one relationship does not reduce your revenue by 5 per cent – it reduces it by 25 per cent.

This article applies the WC-PULSE Framework™ to the specific realities of Caribbean finance. It is not a localisation exercise – adding a Caribbean flag to a global framework. It is a fundamental recalibration that accounts for the structural characteristics that make working-capital management in the Caribbean harder, more volatile, and more consequential than in larger, deeper markets.

The Caribbean CFO does not have the luxury of working-capital inefficiency. In a small, open economy, the margin between adequate and insufficient can be measured in days, not quarters.

The Five Structural Pressures

Caribbean working-capital management operates under five structural pressures that are either absent or significantly muted in larger economies. Understanding these pressures is the prerequisite for any framework that claims to serve the Caribbean finance leader.

Pressure 1: Currency Fragility

The most pervasive pressure is currency risk. Whether the local currency operates under a managed float, a crawling peg, or a fixed-rate regime, the Caribbean CFO lives with a reality that most global frameworks ignore: the exchange rate can move against you by 5 to 15 per cent in a single quarter, and the hedging instruments available to manage that exposure are either expensive, illiquid, or unavailable in the tenors you need.

For a Jamaican manufacturer importing raw materials in US dollars, a 10 per cent depreciation of the JMD does not merely increase costs – it reshapes the entire working-capital equation. The inventory on the warehouse floor, purchased at the old rate, is suddenly worth more to replace than the revenue it will generate at current prices. The cash collected from yesterday’s sales cannot fund tomorrow’s purchases at the new exchange rate. The gap is funded from working-capital reserves that were sized for a different currency reality, and if those reserves are insufficient, the company is forced into emergency borrowing at rates that reflect the market’s assessment of currency risk – typically 200 to 500 basis points above normal facility pricing.

The WC-PULSE Framework addresses currency fragility through three calibrations. First, the E-Layer’s FX Exposure Ratio is calculated on an unhedged basis with a penalty applied for any exposure above 30 per cent of total working capital – a tighter threshold than the 40 per cent default used for companies in stable-currency jurisdictions. Second, the P-Layer’s scenario engine includes a standing FX-depreciation overlay calibrated to the 95th-percentile historical movement for the relevant currency pair, ensuring that the 13-week forecast always reflects a realistic adverse FX scenario. Third, the Red Zone buffer requirement is increased by a currency-volatility premium that adds 10 to 20 days of coverage above the base calculation, sized according to the proportion of USD-denominated working capital.

Pressure 2: Import Dependency

Caribbean economies are structurally import-dependent. For most CARICOM nations, imports represent 40 to 70 per cent of GDP. At the corporate level, this translates into supply chains that are long, concentrated, and vulnerable to disruption at multiple points: shipping delays, port congestion, customs clearance bottlenecks, and supplier-country disruptions that the Caribbean buyer has no ability to influence.

The working-capital implication is a structurally elevated DIO. Caribbean manufacturers and distributors must carry more inventory than their counterparts in supply-abundant markets, because the lead time to replenish is measured in weeks rather than days and the consequences of a stockout extend beyond lost sales to potential production shutdowns. The challenge is calibrating the right amount of additional inventory buffer – enough to protect against realistic supply disruptions without tying up excessive capital in slow-moving stock.

The S-Layer addresses this through a Caribbean-specific modification: the Ecosystem Resilience Score incorporates a Replenishment Lead-Time Factor that adjusts the scoring based on the actual time required to source alternative supply for each critical input. A component that can be re-sourced from a regional supplier in two weeks receives a different resilience treatment than one that requires a six-week ocean shipment from Asia. This granularity ensures that the PULSE Score reflects the real supply-chain dynamics of the Caribbean rather than applying generic global assumptions.

Pressure 3: Shallow Credit Markets

In most Caribbean jurisdictions, the commercial banking sector is concentrated among three to five institutions. Corporate credit decisions are made by a small number of individuals, and the terms available to any given borrower are influenced as much by relationship dynamics and sectoral appetite as by the borrower’s financial metrics. Revolving credit facilities that are renewable annually on standard terms in New York may require quarterly covenant testing and annual renegotiation in Kingston or Port of Spain.

This concentration has a direct working-capital consequence: the L-Layer’s Liquidity Depth score must be calibrated differently. In a deep capital market, an organisation with one drawn facility and two undrawn committed facilities has three layers of liquidity. In a shallow Caribbean credit market, the undrawn facilities may be less reliable than they appear – because the providing bank may reduce or withdraw commitment at the next renewal if its sectoral exposure limits are reached or if the macroeconomic environment deteriorates.

The PULSE Framework’s Caribbean calibration applies a Facility Reliability Discount to undrawn credit facilities, reducing their contribution to the L-Layer score by 15 to 30 per cent depending on the facility’s contractual strength (committed versus uncommitted), the providing bank’s historical behaviour, and the current credit-market conditions as measured by the E-Layer’s Credit Market Tightness Index.

Pressure 4: Customer Concentration

The small size of Caribbean economies produces customer-concentration levels that would be considered extreme in larger markets. It is not unusual for a Caribbean company’s top three customers to represent 50 to 70 per cent of revenue – and for one of those customers to be a government entity with payment behaviour that is influenced by fiscal cycles, political priorities, and bureaucratic processes rather than commercial norms.

Government receivables deserve special treatment in the Caribbean PULSE configuration. The S-Layer’s Ageing Waterfall Velocity metric is segmented to track government and non-government receivables separately, because the payment dynamics are fundamentally different. Government receivables often exhibit step-function payment patterns – nothing for 60 to 90 days followed by a large lump-sum settlement – that would trigger false alarms in a system designed for the smooth collection curves of private-sector customers. The Caribbean calibration applies a Government Receivables Overlay that adjusts the trigger thresholds and smooths the scoring to account for these patterns while still flagging genuine deterioration when government payment behaviour extends beyond historical norms.

Pressure 5: Natural-Disaster Exposure

The Atlantic hurricane season, which runs from June through November, imposes an annual working-capital planning challenge that has no equivalent in most global frameworks. A direct hurricane hit can shut down operations for days to weeks, destroy physical inventory, disrupt supply chains, delay customer payments, and trigger insurance claims that take months to settle. Even a near-miss can disrupt shipping routes, damage port infrastructure, and cause customers to delay purchases in anticipation of disruption.

The WC-PULSE Framework incorporates hurricane season through a Seasonal Resilience Adjustment that modifies the composite PULSE Score during the June-to-November window. The adjustment operates in two ways: it increases the minimum buffer floor by 15 to 25 days of operating costs, ensuring that the organisation enters hurricane season with additional reserves; and it temporarily increases the weight of the L-Layer in the composite calculation, prioritising liquidity depth during the period of highest vulnerability. These adjustments are automatically activated by the Dashboard on 1 June and deactivated on 30 November, ensuring consistent application without manual intervention.

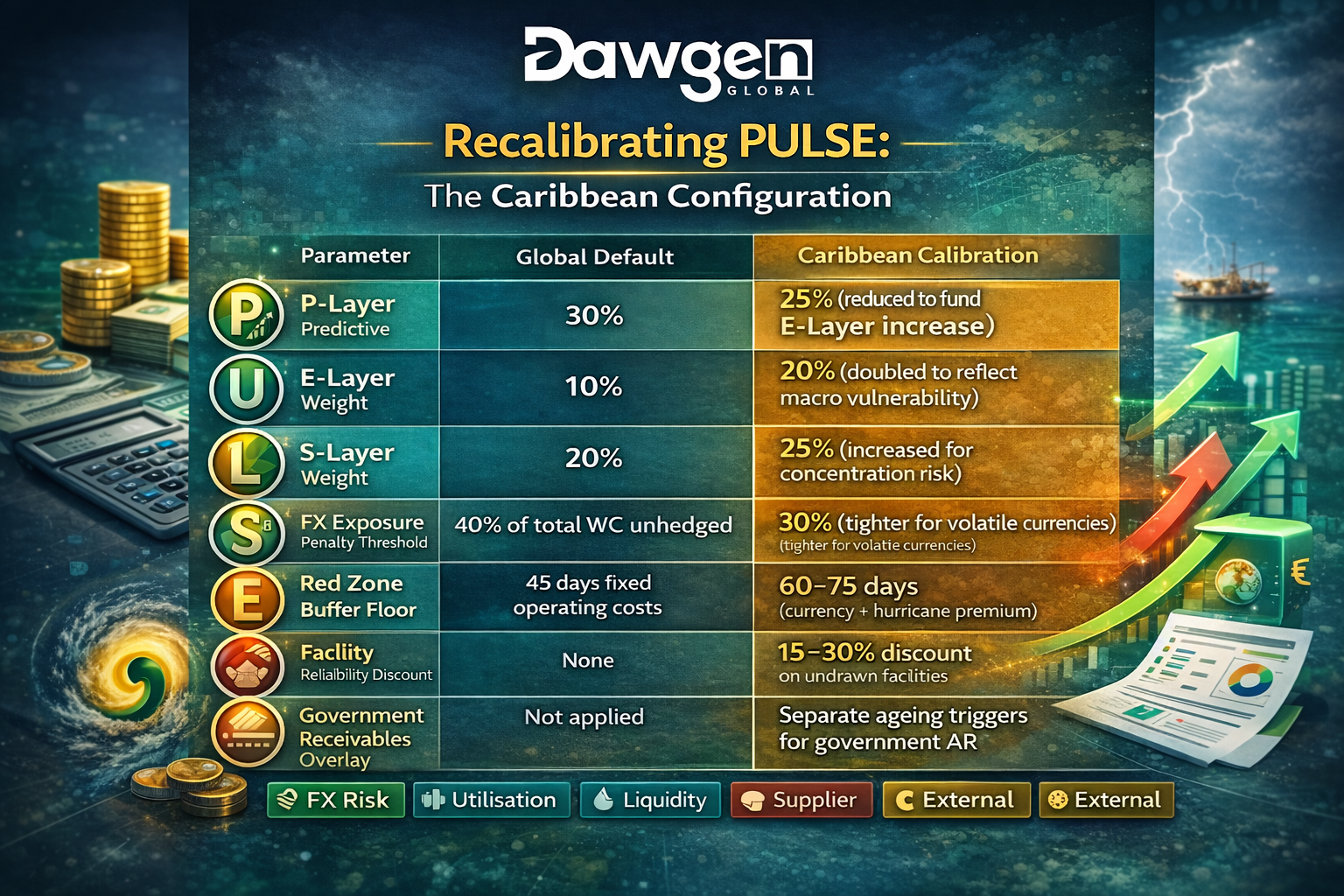

Recalibrating PULSE: The Caribbean Configuration

The five structural pressures produce a Caribbean PULSE configuration that differs materially from the default. The following table summarises the key calibration differences:

| Parameter | Global Default | Caribbean Calibration |

| P-Layer Weight | 30% | 25% (reduced to fund E-Layer increase) |

| E-Layer Weight | 10% | 20% (doubled to reflect macro vulnerability) |

| S-Layer Weight | 20% | 25% (increased for concentration risk) |

| FX Exposure Penalty Threshold | 40% of total WC unhedged | 30% (tighter for volatile currencies) |

| Red Zone Buffer Floor | 45 days fixed operating costs | 60–75 days (currency + hurricane premium) |

| Facility Reliability Discount | None | 15–30% discount on undrawn facilities |

| Government Receivables Overlay | Not applied | Separate ageing triggers for government AR |

| Hurricane Season Adjustment | Not applied | Buffer +15–25 days; L-Layer weight +5% (Jun–Nov) |

These calibrations are not cosmetic. They fundamentally change the zone classification for Caribbean enterprises. A company that scores 52 on the global default configuration – comfortably mid-Amber – may score 44 under the Caribbean configuration because the increased E-Layer and S-Layer weights expose vulnerabilities that the default weights suppress. This is intentional: the Caribbean calibration is designed to be more conservative because the operating environment demands it.

Lessons from Jamaica, Trinidad, and Barbados

Dawgen Global has implemented the Caribbean-calibrated PULSE Framework across multiple jurisdictions. Three brief vignettes illustrate how the regional pressures play out in practice and how the calibrated framework responds.

Jamaica: The FX Cascade

A Kingston-based food manufacturer experienced a 12 per cent JMD depreciation over a four-month period in late 2024. The E-Layer detected the movement within the first month and triggered an Amber Alert when the FX Exposure Ratio exceeded the Caribbean-calibrated 30 per cent threshold. The P-Layer’s standing FX scenario overlay showed that a continuation of the depreciation trend would push the composite PULSE Score below 38 within six weeks. The Working Capital Council authorised three pre-emptive actions: an emergency FX forward contract covering 60 per cent of anticipated USD purchases for the next 90 days, a 5 per cent price increase on the highest-volume product lines to begin recovering the margin compression, and a 30-day deferral of a planned equipment purchase to preserve cash. By the time the depreciation stabilised, the company had absorbed the shock without breaching the Red Zone – a result that would have been impossible without the early-warning system.

Trinidad: The Government Receivables Trap

A Port of Spain professional-services firm derived 40 per cent of its revenue from government contracts. The traditional DSO calculation showed 52 days – within policy. But the S-Layer’s Government Receivables Overlay revealed a different reality: private-sector DSO was 34 days while government DSO was 78 days and trending upward. The overlay’s separate trigger fired an Amber Alert, and the Council initiated a three-pronged response: a formal meeting with the relevant ministry to discuss payment acceleration, a shift in invoicing cadence from monthly to milestone-based to create more frequent payment triggers, and a recalculation of the P-Layer forecast using the government-specific payment distribution rather than the blended average. The government DSO improved to 61 days within three months – still elevated but now visible, tracked, and governed rather than hidden inside an average.

Barbados: The Shallow-Credit Squeeze

A Bridgetown distribution company relied on two revolving credit facilities totalling US$8 million. When one of the providing banks announced a reduction in its Caribbean commercial-lending portfolio, the company received notice that its US$3 million facility would not be renewed at the next annual review. Under the standard PULSE configuration, the company’s L-Layer score would have remained adequate because the remaining US$5 million facility was undrawn. Under the Caribbean calibration, however, the Facility Reliability Discount had already reduced the undrawn facility’s contribution to the L-Layer score by 25 per cent, and the loss of the second facility triggered an immediate zone transition to Red. The advance warning gave the CFO four months – rather than the typical four weeks – to negotiate a replacement facility with an alternative bank, avoiding the panic pricing and unfavourable covenants that typically accompany emergency refinancing.

The Peer Advantage: Why Caribbean CFOs Need Each Other

One of the most striking findings from our Caribbean engagements is the isolation that many CFOs experience. In larger markets, finance leaders have access to extensive peer networks, benchmarking data, industry conferences, and professional communities where working-capital challenges are discussed openly and best practices are shared. In the Caribbean, the small size of the business community, the sensitivity of financial information in concentrated markets, and the limited availability of region-specific benchmarking data create an environment where CFOs often manage working-capital challenges in relative isolation.

This isolation is itself a working-capital risk. A CFO who cannot benchmark their DSO against regional peers may not know that their 55-day performance is 15 days above the sector median. A Treasurer who has never discussed FX-hedging strategies with counterparts in similar jurisdictions may not know that practical, affordable hedging structures exist. A finance director who has never heard how another company solved the government-receivables problem may spend months reinventing a solution that already exists.

Dawgen Global addresses this gap through the Caribbean CFO Working Capital Roundtable – a quarterly, invitation-only peer-learning forum that brings together 15 to 20 senior finance leaders from across the region. The Roundtable operates under Chatham House rules: participants are free to discuss the content of the sessions but may not attribute specific comments or data to individual companies. This structure creates the trust required for genuine knowledge-sharing in a small, interconnected business community.

Each Roundtable session is structured around a specific working-capital theme, anchored by PULSE data and facilitated by a Dawgen Global Senior Advisor. Recent sessions have covered FX-hedging strategies for Caribbean corporates, government-receivables management, hurricane-season cash planning, and supply-chain diversification in import-dependent economies. The sessions produce actionable takeaways, regional benchmarking data, and peer connections that extend beyond the formal event.

YOU DON’T HAVE TO NAVIGATE THIS ALONE.

Dawgen Global is a Caribbean-headquartered, globally connected advisory firm delivering transformation across Strategy, Finance, Operations, Technology, and Governance. With deep roots in Jamaica, Trinidad and Tobago, Barbados, and the wider CARICOM region, we understand the unique operating environment that Caribbean finance leaders navigate every day. Our Working Capital Advisory practice is powered by the proprietary WC-PULSE Framework™, calibrated specifically for the realities of small, open economies.

Join the Caribbean CFO Working Capital Roundtable by requesting invitation @[email protected]

A quarterly, invitation-only peer-learning forum for senior Caribbean finance leaders. Powered by PULSE insights, anchored by regional benchmarking data, and facilitated by Dawgen Global Senior Advisors. Chatham House rules. Actionable takeaways. Peer connections that last.

The WC-PULSE Thought Leadership Series

Articles 1–8: CCC Blind Spots → Buffer vs. Reprice → 13-Week Crystal Ball → Supplier Ecosystem → Governance → Reprice Playbook → E-Layer → 90-Day Case Study

Article 9: “Caribbean CFO Survival Guide: Working Capital in a Small, Open Economy” (You are here)

Coming Next – Article 10: “AI-Powered Cash Forecasting: The P-Layer Technology Stack Revealed” – From machine-learning payment-behaviour models to automated anomaly detection – the technology architecture behind the P-Layer and a pragmatic roadmap for AI adoption in your treasury function.

About Dawgen Global

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

Email: [email protected]

Email: [email protected]  Visit: Dawgen Global Website

Visit: Dawgen Global Website

WhatsApp Global Number : +1 555-795-9071

WhatsApp Global Number : +1 555-795-9071

Caribbean Office: +1876-6655926 / 876-9293670/876-9265210  WhatsApp Global: +1 5557959071

WhatsApp Global: +1 5557959071

USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements