The Audit That Revealed Six Years of Overpayment

The chief financial officer of a Caribbean beverage manufacturer received a call from the company’s external tax advisor on a Thursday afternoon in September. The advisor had been engaged to assist with a routine tax audit by the revenue authority — an audit the company had expected to result in a modest additional assessment, given the complexity of its operations across manufacturing, distribution, and export. What the advisor found was not what anyone had anticipated.

The company had been overpaying corporate income tax for approximately six years. The overpayment was not the result of a single error. It was the cumulative consequence of multiple missed opportunities, each individually modest but collectively devastating: approved tax incentives for manufacturing that had never been claimed because the finance team was unaware they existed; capital allowances on qualifying plant and equipment that had been calculated at rates below those permitted by the legislation; export incentives that the company was entitled to but had never applied for because the application process was perceived as too complex; and employment tax credits for a workforce training programme that met the statutory criteria but had never been formally documented for tax purposes.

The total overpayment was estimated at approximately US$1.4 million. Six years of tax that the company was never required to pay. Six years of cash flow that could have funded equipment upgrades, market expansion, or the working capital that the CFO had been managing on increasingly tight margins.

The revenue authority’s audit, meanwhile, also identified deficiencies. The company’s transfer pricing documentation for intercompany sales to its distribution subsidiary in a neighbouring territory was incomplete. Its treatment of certain marketing expenses as deductible had been inconsistent with the revenue authority’s published guidance. And its GCT returns contained classification errors that, while not indicative of fraud, demonstrated a lack of systematic compliance processes.

The net result was paradoxical: a company that had been overpaying its income tax for six years was simultaneously exposed to penalties for compliance failures in other areas. It was both overly generous to the revenue authority and inadequately governed in its tax affairs. The CFO’s summary to the board was blunt: “We have been paying too much tax and managing too much risk, simultaneously, because we have never had a tax strategy.”

This fictional scenario, while not attributable to any specific Caribbean manufacturer, reflects a pattern that Dawgen Global encounters with troubling regularity across the region. Caribbean enterprises that are operationally sophisticated, commercially successful, and financially disciplined are managing their tax affairs with a level of informality and passivity that costs them money, creates compliance risk, and leaves value on the table that their competitors may be capturing.

The State of Caribbean Tax Management

Tax is the single largest recurring cash outflow for most Caribbean enterprises. Corporate income tax, general consumption tax or value added tax, payroll taxes, social security contributions, customs duties, stamp duties, property taxes, and sector-specific levies collectively represent a compliance burden and a financial impact that exceeds any other category of business expenditure. Yet for the majority of Caribbean enterprises, tax management is treated as a compliance function rather than a strategic discipline.

The typical pattern is familiar: tax returns are prepared and filed by the finance team or an external accountant, often under time pressure, with the primary objective of meeting filing deadlines rather than optimising the company’s tax position. Tax planning — the systematic analysis of how business decisions, corporate structures, and transaction arrangements affect the company’s tax obligations — is either absent or episodic. Tax incentives are claimed only when someone happens to know they exist. Transfer pricing is documented, if at all, as an afterthought when the revenue authority asks for it. And the board receives no regular reporting on the company’s tax position, tax risks, or tax strategy.

This passive approach to tax management creates a dual vulnerability. On one side, companies overpay tax by failing to claim incentives, allowances, and reliefs to which they are legally entitled. On the other side, they accumulate compliance risk by failing to maintain the documentation, processes, and governance structures that revenue authorities increasingly expect. The tax gap in Caribbean enterprises is not a gap between what companies pay and what they owe — it is the gap between how companies manage tax and how they should manage it.

Five Dimensions of the Caribbean Tax Gap

Unclaimed Incentives and Reliefs: Caribbean governments offer a substantial array of tax incentives designed to promote investment, employment, export activity, and sectoral development. Jamaica’s fiscal incentive regime includes incentives under the Income Tax Act, the Customs Act, the Jamaica Special Economic Zone Authority framework, and sector-specific legislation for tourism, agriculture, manufacturing, and creative industries. Trinidad and Tobago offers incentives through the Corporation Tax Act, the Fiscal Incentives Act, and sector-specific provisions for energy, manufacturing, and technology. Barbados maintains incentives for international business, small business, and renewable energy. Across the Eastern Caribbean, investment incentive legislation provides concessions on corporate tax, customs duties, and stamp duties for qualifying enterprises. The challenge is that many Caribbean enterprises — particularly mid-market companies without dedicated tax departments — are unaware of the incentives available to them, uncertain about eligibility criteria, or deterred by application processes that they perceive as bureaucratic and time-consuming. The result is that incentives designed to reduce the cost of doing business and promote economic development go unclaimed by the very enterprises they were designed to benefit.

Transfer Pricing Exposure: The global transfer pricing landscape has undergone a fundamental transformation driven by the OECD’s Base Erosion and Profit Shifting initiative. Caribbean revenue authorities — including Jamaica’s Tax Administration Jamaica, Trinidad and Tobago’s Board of Inland Revenue, and the Barbados Revenue Authority — are building transfer pricing audit capability, adopting transfer pricing legislation, and participating in the automatic exchange of information frameworks that enable them to identify intercompany transactions that may not reflect arm’s-length pricing. Caribbean enterprises that operate across multiple territories — a common structure given the region’s small national markets — face transfer pricing risk that many have not adequately assessed or documented. The intercompany management fees, royalties, service charges, and goods transfers that facilitate multi-territory operations must be priced and documented in accordance with transfer pricing principles that are becoming progressively more rigorous. Enterprises that lack transfer pricing documentation face the risk of revenue authority adjustments, double taxation, penalties, and the reputational consequences of being perceived as engaged in profit shifting.

Indirect Tax Complexity: Jamaica’s General Consumption Tax, Trinidad and Tobago’s Value Added Tax, Barbados’s Value Added Tax, and the indirect tax regimes across the Eastern Caribbean and wider region create a compliance landscape of considerable complexity. Classification of goods and services, determination of taxable and exempt supplies, input tax credit recovery, timing of supply rules, and cross-border supply provisions all require technical expertise that many Caribbean enterprises lack. The digitisation of commerce — e-commerce, digital services, and platform-based business models — is adding new layers of indirect tax complexity as Caribbean revenue authorities adapt their frameworks to capture tax on digital supplies. Enterprises that sell goods or services across Caribbean jurisdictions face indirect tax obligations in multiple territories, each with its own registration thresholds, filing requirements, and compliance procedures.

Payroll Tax and Employment Cost Governance: Payroll-related taxes and social contributions represent a significant portion of Caribbean enterprises’ total tax burden. Jamaica’s employers must navigate PAYE income tax, National Insurance Scheme contributions, National Housing Trust contributions, Education Tax, and HEART Trust/NTA contributions. Trinidad and Tobago’s employers must manage PAYE, National Insurance, and Health Surcharge. Similar multi-layered payroll obligations exist across the region. The complexity of these obligations — each with its own rates, thresholds, filing frequencies, and penalty regimes — creates compliance risk that materialises with particular severity during statutory audits. Misapplication of tax thresholds, incorrect classification of employees versus contractors, failure to account for benefits in kind, and errors in remittance timing can result in assessments, penalties, and interest that significantly exceed the underlying tax at stake.

No Tax Governance Framework: Perhaps the most fundamental dimension of the Caribbean tax gap is the absence of a governance framework for tax. In well-governed organisations, tax strategy is approved by the board, tax risk is monitored and reported, tax planning is integrated with business decision-making, and tax compliance is subject to the same internal controls and quality assurance that apply to financial reporting. In the majority of Caribbean enterprises, none of these governance elements exist. Tax is managed operationally by the finance team, with no board oversight, no documented strategy, no risk framework, and no quality assurance beyond the external accountant’s review at year-end. This governance vacuum means that tax decisions are made without strategic context, tax risks accumulate without visibility, and tax opportunities are missed without accountability.

The Cost of the Caribbean Tax Gap

The cost of the Caribbean tax gap is both financial and strategic. Financially, the combination of unclaimed incentives, suboptimal structures, and compliance penalties represents a direct erosion of enterprise value. The fictional beverage manufacturer that overpaid US$1.4 million in corporate income tax over six years was not the victim of aggressive tax enforcement — it was the victim of its own passivity. That US$1.4 million, had it been retained and reinvested, would have compounded in business value over those six years.

Strategically, the tax gap undermines competitiveness. Caribbean enterprises compete for capital, partnerships, and talent in markets where tax efficiency is a factor in investment decisions. A company with an effective tax rate significantly above the minimum achievable rate is at a disadvantage relative to competitors who manage their tax affairs strategically. International investors, joint venture partners, and acquirers evaluate the tax efficiency of target companies as part of their due diligence. A company that cannot demonstrate strategic tax management signals governance immaturity to sophisticated counterparties.

The reputational dimension is increasingly significant. As global attention focuses on corporate tax practices — driven by BEPS, country-by-country reporting, and public disclosure requirements — Caribbean enterprises face scrutiny from both directions. Aggressive tax avoidance risks reputational damage and regulatory attention. But passive tax management that results in overpayment and missed incentives signals to shareholders and stakeholders that the company is not being managed in their best interests. The appropriate position is strategic tax management: fully compliant, fully optimised, fully governed.

Dawgen Global’s Tax Strategy and Compliance Programme

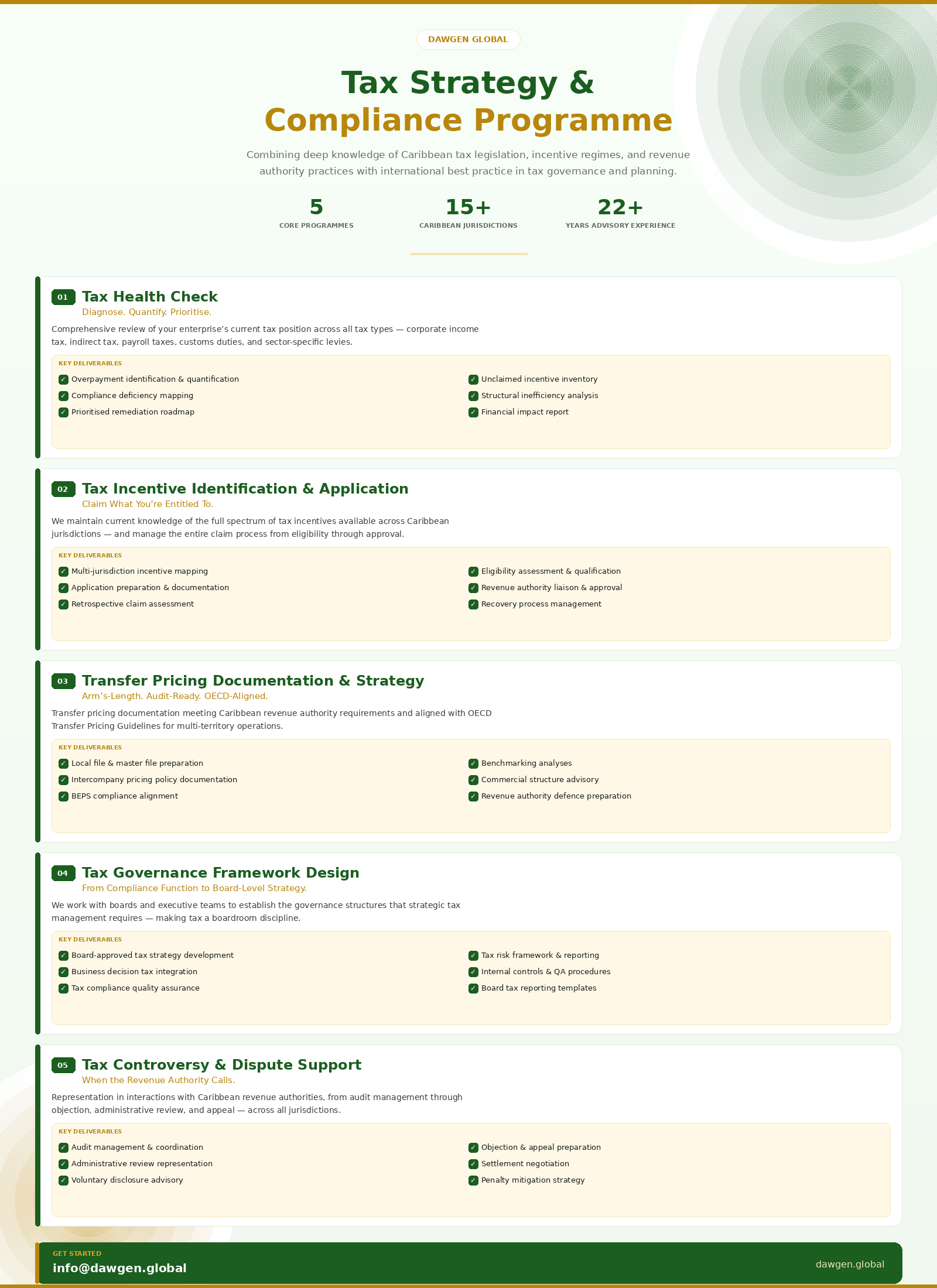

Dawgen Global has developed a Tax Strategy and Compliance Programme specifically designed for Caribbean enterprises, combining deep knowledge of Caribbean tax legislation, incentive regimes, and revenue authority practices with international best practice in tax governance and planning.

Tax Health Check: Dawgen Global conducts comprehensive reviews of the enterprise’s current tax position across all tax types — corporate income tax, indirect tax, payroll taxes, customs duties, and sector-specific levies — identifying overpayments, unclaimed incentives, compliance deficiencies, and structural inefficiencies. The Tax Health Check produces a prioritised report quantifying the financial impact of identified issues and providing a clear roadmap for remediation and optimisation.

Tax Incentive Identification and Application: Dawgen Global maintains current knowledge of the full spectrum of tax incentives available across Caribbean jurisdictions. We identify the incentives for which each client qualifies, prepare the required applications and supporting documentation, and manage the approval process with the relevant revenue authority or incentive agency. For enterprises that have failed to claim incentives in prior periods, Dawgen Global assesses the availability of retrospective claims and manages the recovery process.

Transfer Pricing Documentation and Strategy: Dawgen Global prepares transfer pricing documentation that meets the requirements of Caribbean revenue authorities and aligns with OECD Transfer Pricing Guidelines. This includes preparing local files and master files, conducting benchmarking analyses, documenting intercompany pricing policies, and advising on transfer pricing structures that achieve commercial objectives while maintaining arm’s-length compliance.

Tax Governance Framework Design: Dawgen Global works with boards and executive teams to establish the governance structures that strategic tax management requires. This includes developing board-approved tax strategies, establishing tax risk frameworks and reporting, integrating tax planning into business decision-making processes, and building the internal controls and quality assurance procedures that ensure tax compliance quality.

Tax Controversy and Dispute Support: Dawgen Global represents clients in interactions with Caribbean revenue authorities, from audit management through objection, administrative review, and appeal. Our tax controversy team combines technical tax expertise with deep understanding of revenue authority procedures, audit methodologies, and settlement practices across Caribbean jurisdictions.

From Compliance Cost to Strategic Asset

The fictional beverage manufacturer that overpaid US$1.4 million while simultaneously accumulating compliance risk did not have a tax problem. It had a governance problem. The finance team was competent at preparing and filing returns. What the company lacked was the strategic framework that would have ensured incentives were identified and claimed, structures were optimised, documentation was maintained, and the board understood the company’s tax position and the risks and opportunities it presented.

Caribbean enterprises that transform their approach to tax — from passive compliance to strategic management — unlock value that goes directly to the bottom line. Every legitimately claimed incentive is cash retained. Every structural optimisation is margin improved. Every compliance deficiency remediated is a penalty avoided and a regulatory relationship strengthened. Tax is not merely a cost of doing business. Managed strategically, it is a source of competitive advantage.

The journey from compliance to strategy begins with a single step: an honest assessment of the current tax position. What incentives are available and unclaimed? What structural inefficiencies exist? What compliance risks are accumulating? What is the board’s visibility into the company’s tax affairs? The answers to these questions define the gap. Closing that gap is the work of strategic tax leadership.

Start With a Tax Health Check

Dawgen Global invites Caribbean CFOs, boards, and business owners to take the first step toward strategic tax management. Our Tax Health Check provides a comprehensive, confidential assessment of your enterprise’s tax position across all tax types, identifying overpayments, unclaimed incentives, compliance risks, and optimisation opportunities with a quantified financial impact analysis.

Request a proposal for Dawgen Global’s Tax Health Check and Strategic Tax Review. Email [email protected] or visit www.dawgen.global to begin the conversation.

DAWGEN GLOBAL | Big Firm Capabilities. Caribbean Understanding.

Request a proposal for Dawgen Global’s Tax Health Check and Strategic Tax Review.

Email: [email protected]

Web: www.dawgen.global

About Dawgen Global

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

Email: [email protected]

Email: [email protected]  Visit: Dawgen Global Website

Visit: Dawgen Global Website

WhatsApp Global Number : +1 555-795-9071

WhatsApp Global Number : +1 555-795-9071

Caribbean Office: +1876-6655926 / 876-9293670/876-9265210  WhatsApp Global: +1 5557959071

WhatsApp Global: +1 5557959071

USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements