Notes to Nodes: The Great Payment Transition

The difference a rail makes

Many countries don’t reduce cash usage by persuading people; they do it by lowering the cost of switching. That’s what national, interoperable, instant-payment rails do. When the rulebook (policy) and the track (infrastructure) are aligned, paying digitally becomes the default—cheap for small merchants, safe for consumers, and simple for everyone. India’s UPI, Brazil’s PIX, Thailand’s PromptPay, Malaysia’s DuitNow, and Singapore’s PayNow prove that a well-governed rail can shift millions of daily transactions off cash without expensive hardware or complex onboarding. For the Caribbean—where small island economies juggle tourism, remittances, and MSMEs—the policy-plus-rail approach offers a path to move 10–20 points off cash safely, fast.

1) What a “national rail” really is (and isn’t)

A national instant-payment rail is a shared utility with four critical properties:

-

Interoperability by default

Banks, licensed wallets, and PSPs can all send and receive payments to each other—same QR, same addressing (phone number, alias, or account), same rules. -

Instant clearing and settlement

Payments land in seconds, with finality. For micro and small merchants, this is the cash-equivalent guarantee. -

Open access with proportionate guardrails

Participation is open to regulated actors (banks, e-money issuers, PSPs) with risk-based requirements. Gatekeeping is about safety, not favoritism. -

Transparent scheme rules and consumer protection

Clear dispute timelines, fraud liability allocations, and fee disclosures—published and enforced.

It’s not another app or brand. The rail is the invisible layer that powers many apps—bank apps, wallets, super-apps, and sector apps (transit, utilities). Think roads, not cars.

2) Why rails move behavior: the three R’s

-

Reach: Interoperability collapses fragmentation. If every shop window accepts the same QR, consumers don’t guess which app works where.

-

Reliability: Instant settlement + uptime SLAs make digital feel like cash, not like a “maybe.”

-

Rate (pricing): Micro-fee bands (or zero-fee for small tickets) make digital cheaper than cash handling for merchants—and cheaper than cards.

When those three combine, network effects kick in: people prefer digital because it’s easier and merchants prefer it because it’s safer and faster.

3) Global blueprints: what worked—and why

India: UPI (public rail, private innovation)

-

Design: Open APIs, interoperable QR, aliasing via phone numbers/virtual IDs, 24/7 instant payments, wide PSP ecosystem.

-

Levers that mattered: Zero/near-zero fees for P2P and small P2M; government payments (G2P) on-rail; QR ubiquity for micro-merchants; strong identity backbone for e-KYC.

-

Takeaway for small states: You don’t need millions of terminals; you need one national QR spec, tiered e-KYC, and instant settlement.

Brazil: PIX (central bank-run instant rail)

-

Design: Mandatory participation for major banks, interoperable addressing (“PIX keys”), 24/7 instant transfers, low/no fees.

-

Levers that mattered: Compulsory adoption created universal reach quickly; standard UX patterns (QR, key directory) reduced friction; merchants got speed + cost certainty.

-

Takeaway: A decisive, central-bank-led launch can compress adoption timelines from years to months.

Thailand: PromptPay; Malaysia: DuitNow; Singapore: PayNow

-

Design: Alias addressing (phone/ID), interoperable QR; cross-border QR pilots among ASEAN neighbors.

-

Levers that mattered: Simple identifiers, QR in hawker centers/markets, and regional interoperability that matches travel patterns.

-

Takeaway: Start with domestic interoperability; then extend to trusted cross-border corridors that matter (tourism, workers).

4) Caribbean Spotlight: the case for a CARICOM-grade rail

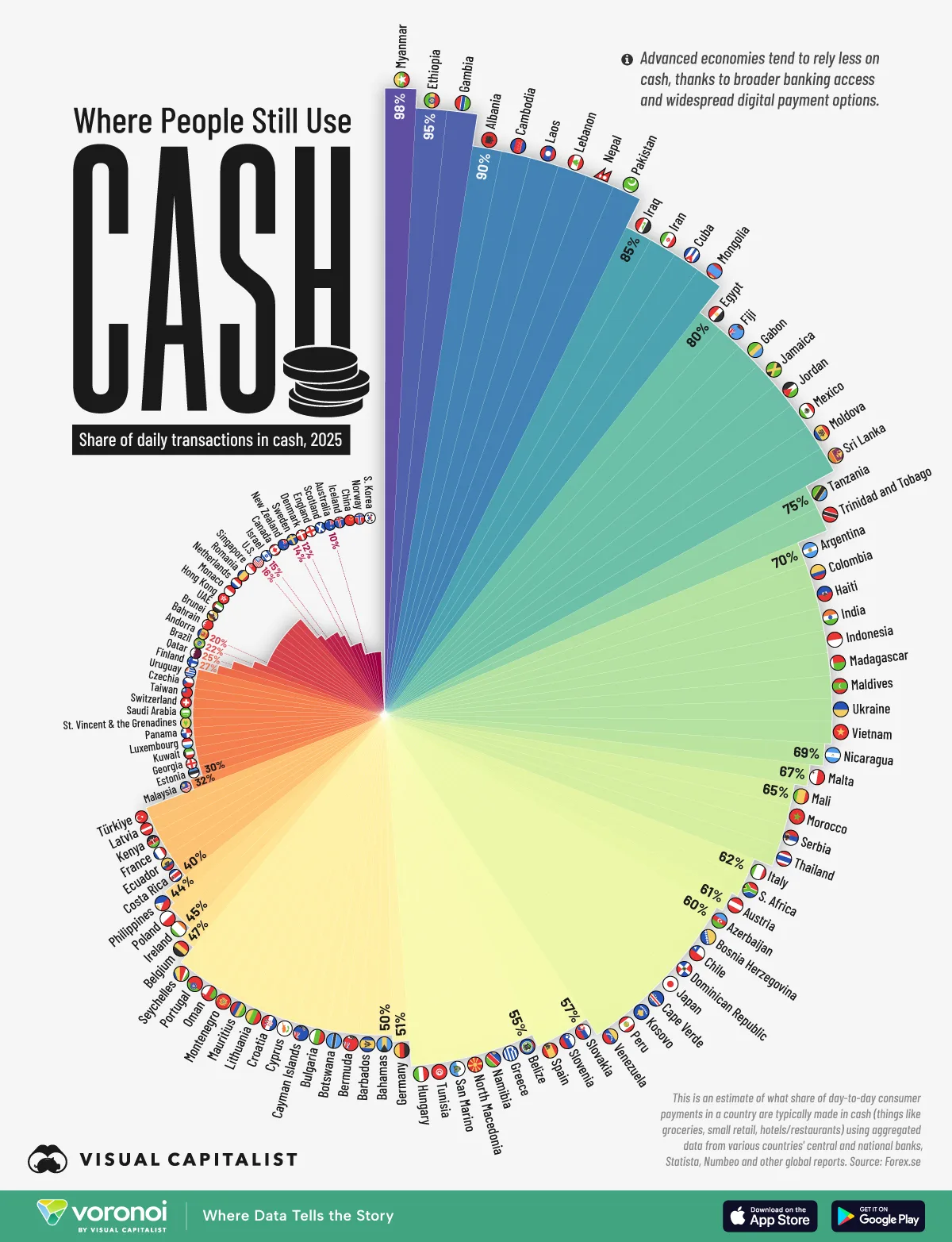

From the cash-usage visualization, daily transactions in several Caribbean markets remain high in cash—e.g., Jamaica (~80%), Trinidad & Tobago (~75%), Haiti (~70%), Dominican Republic (~60%), Bahamas (~51%), Barbados (~50%), with multiple OECS islands also on the higher-cash arc. That pattern is rational in hurricane-prone, tourism-heavy, remittance-rich economies. A rail must therefore be:

-

Interoperable across banks and wallets from day one

-

Merchant-first on pricing (micro-MDR bands; instant settlement)

-

Offline-capable with clear caps and reconciliation

-

Cross-border aware for tourism and remittances (FX clarity, limits, and dispute rules)

What a Caribbean rail should prioritize:

-

National QR standard adopted across issuers/PSPs, with printed static QR as the baseline and dynamic QR for higher-volume merchants.

-

Alias addressing (phone/email or national ID where appropriate) so paying anyone is type-and-go.

-

Instant settlement (T+0) for micros up to daily caps (e.g., US$500–1,000).

-

Tiered e-KYC to onboard MSMEs and consumers quickly; limits increase with usage and verification.

-

Resilience: offline tokens, USSD fallbacks, and liquidity buffers so the rail works through outages.

5) The merchant math on rails: why fees and funds timing flip behavior

Fee architecture (example bands)

-

≤ US$2: free

-

US$2–$10: ≤ 0.5% (or a small fixed micro-fee)

-

US$10–$50: ≤ 0.8–1.0%

-

> US$50: market-priced within caps

Settlement guarantees

-

Instant for eligible transactions up to the daily micro cap

-

Provisional T+0 during declared outages; auto-net on recovery

Dispute model (plain-language)

-

Under $25 with device verification and merchant-present QR: merchant protected barring evidence of fraud

-

Resolution windows: 7/3/10 (7 days to dispute, 3 days merchant response, 10 days decision)

This is the bundle that beats cash and makes small merchants comfortable.

6) Governance: how to keep rails fair, fast, and trusted

-

Operator: Central bank, designated payments council, or neutral utility with public oversight

-

Rulebook: Published scheme rules, change-control calendar, public consultation for major updates

-

Participant tiers: Banks, e-money issuers, PSPs—each with proportionate capital/tech/risk obligations

-

Certification: QR conformance, security tests, offline-mode compliance

-

Transparency: Uptime dashboard, dispute metrics, fee tables, and post-incident reports

Good governance is the difference between a rail that scales and a rail people avoid.

7) Inclusion by design: onboarding that meets people where they are

Tiered e-KYC lets users enter with what they have and grow capability:

-

Tier 0: Name + phone; tiny limits; P2P and micro-purchases only

-

Tier 1: Add date of birth and selfie/OTP; higher limits; P2M allowed

-

Tier 2: Add ID verification/address; full limits; merchant accounts, payroll, and remittance reception

Assisted onboarding (agents, bank correspondents) is essential for rural areas and older users; training and scripts should be standardized across providers.

8) Tourism & remittances: build the real corridors first

Tourism corridor design

-

Pricing clarity: Local currency as primary; optional FX display; no hidden conversion fees

-

Acceptance density: QR/tap-to-phone kits for hotels, taxis, craft markets, tours; pre-event packets for festivals/cruise days

-

Dispute fast lanes: Sub-$25 disputes resolved within 48 hours during peak seasons

Remittance corridor design

-

Direct-to-rail credits: Inbound remittances land into wallet/bank on the same rail used at merchants

-

Spend, not cash-out: Bill-pay and merchant discounts encourage local spending; agent cash-out remains available to avoid user backlash

-

FX transparency: Clear spread and fees; no surprises at checkout

9) Resilience patterns baked into the rail

-

Offline tokens (QR/NFC) with caps and timeboxes; USSD menus for feature phones

-

Liquidity buffers to fund provisional settlement during outages

-

Status comms agreements with telcos/utilities; wallet data zero-rating during emergencies

-

Annual drills (tabletop + live failover) with metrics published as a Resilience Scorecard

If resilience isn’t designed upfront, merchants will default to cash the first time the wind picks up.

10) Implementation roadmap (first 18 months)

Quarter 0–1: Charter & standards

-

Form the scheme operator; publish National QR spec and Tiered e-KYC guidelines

-

Draft fee bands and instant settlement policy (caps + outage provisions)

Quarter 2–3: Pilot & seed density

-

Pilots in 2–3 urban markets + 1 tourism hub; onboard utilities and transit for bill-pay and fares

-

Distribute printed QR kits; enable tap-to-phone; certify first PSPs/wallets

Quarter 4–5: Scale & resilience

-

Expand to fresh markets, taxis/minibuses, beach vendors; run offline drills

-

Launch G2P and G2B on-rail; publish consumer charter and dispute SLAs

Quarter 6: Cross-border corridor (limited)

-

Enable a trusted partner corridor (e.g., a major visitor source market) with FX clarity and dispute reciprocity

-

Release the first Resilience Scorecard and KPI dashboard

11) KPIs that prove the curve is bending

-

Acceptance density: # of active QR/tap-to-phone points per km² and per 1,000 residents

-

T+0 share: % of merchant transactions settled instantly (and % provisional during outages)

-

Micro-ticket digitization: % of ≤ US$10 transactions processed on-rail

-

Remittance spend-through: % of inbound remittances spent digitally within 7 days

-

Dispute metrics: Disputes per 1,000 txns; median time to resolution

-

Resilience metrics: Offline completion rate; median sync time; liquidity buffer utilization

Publish monthly. Momentum is a trust asset.

12) Risks & how to neutralize them

-

Fraud/social engineering: In-app name confirmation, risk-based step-up auth, education nudges, and “cool-off” rules for new payees

-

Data privacy: Minimize data; clear consent flows; anonymize analytics; independent audits

-

Vendor lock-in: Open APIs, portable aliases, and interoperable QR keep the ecosystem contestable

-

Digital exclusion: Agents and assisted service channels; feature-phone support (USSD/SMS)

-

Regulatory fragmentation: Single national rulebook; cross-agency coordination with telcos, utilities, consumer protection bodies

13) Caribbean Spotlight: practical levers for island economies

-

Use the map’s cash shares to prioritize rollout (e.g., Jamaica ~80%, T&T ~75%, Haiti ~70%, DR ~60%, Bahamas ~51%, Barbados ~50%).

-

Start where “lines form”: transit, fresh markets, festivals, craft villages, and school/utility bill-pay.

-

Make the merchant math obvious: show posters with “Fees ≤0.5% for ≤US$10” and “Funds in minutes.”

-

Turn remittances into everyday spend: direct credits + merchant/utility incentives.

-

Design for storms: offline caps printed next to every QR; hotline and WhatsApp support on the same card.

14) CBDCs, stablecoins, and the rail

If a CBDC or compliant stablecoin is launched, treat it as one currency option on the same rail—same QR, same dispute rules, same offline caps. Don’t splinter acceptance. Interoperability is the moat.

15) Closing: policy + rails = confidence

Cash doesn’t persist because people love paper; it persists because it works—cheaply, reliably, privately. To shift behavior, digital must work better on those same terms. That’s what a well-governed, interoperable, instant rail delivers: lower costs for small merchants, cash-equivalent settlement, clear protection, and resilience when the lights flicker. Build the rail, publish the rules, seed acceptance where people actually buy and sell—and the Caribbean’s everyday economy will move, naturally, from notes to nodes.

Work with Dawgen Global

Design the rail, write the rulebook, and sequence adoption for your island or region.

-

Book a 30-minute payments strategy consult.

-

Request our National QR & Instant Rail Playbook and Resilience Scorecard Template.

Contact: 🔗 https://dawgen.global/ | 📧 [email protected] | 📞 USA: 855-354-2447

About Dawgen Global

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

✉️ Email: [email protected] 🌐 Visit: Dawgen Global Website

📞 📱 WhatsApp Global Number : +1 555-795-9071

📞 Caribbean Office: +1876-6655926 / 876-9293670/876-9265210 📲 WhatsApp Global: +1 5557959071

📞 USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements